Introduction

Restaurants face a genuinely unusual combination of risks. Kitchen fires, customer slip-and-falls, foodborne illness claims, and employee injuries can all happen in the same week — sometimes the same day. According to NFPA research on eating and drinking establishment fires, US restaurants average 7,410 structure fires per year, causing $165 million in direct property damage annually. And that's just fire exposure.

What makes budgeting for restaurant insurance difficult is that there's no standard price. A ghost kitchen operator and a high-volume bar might both call themselves "restaurants," but their insurance programs look nothing alike. Premiums vary based on:

- What you serve (food only vs. alcohol)

- Where you operate and your state's requirements

- How many employees you have

- Your claims history and physical space

Here's what you need to know to budget accurately, avoid coverage gaps, and stop overpaying.

Key Takeaways

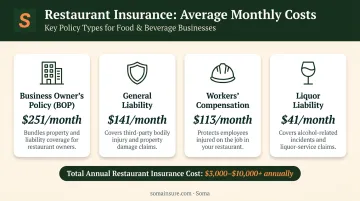

- A full restaurant insurance program typically costs $3,000–$10,000+ per year, depending on size, service model, and risk profile

- A Business Owner's Policy (BOP) is the most cost-effective starting point for most restaurants

- Alcohol service raises both liquor liability and general liability premiums, making it one of the biggest cost drivers

- Workers' compensation is legally required in most states once you have employees

- Working with an independent broker to compare multiple carriers consistently produces better pricing than going direct

How Much Does Restaurant Insurance Cost?

Restaurant insurance has no fixed price — underwriters assess dozens of variables before setting a premium, and two operations of the same size can receive very different quotes.

The two most common budgeting mistakes: pricing only one or two policies in isolation, and forgetting add-on endorsements like food spoilage or equipment breakdown that can significantly affect total annual cost.

Here's a practical breakdown by operation type, based on available industry benchmarks:

Small / Low-Risk Restaurants

Who this covers: Food trucks, small cafés, counter-service spots, ghost kitchens, and solo operators

What's typically included: A basic BOP (general liability + commercial property). May not require liquor liability if alcohol isn't served, and workers' comp may not apply if it's owner-operated with minimal staff. Some carriers advertise coverage from $25/month, but real-world programs with proper property and liability limits run higher.

Estimated annual range: $1,500–$4,000 for a basic program

Mid-Range / Full-Service Restaurants

Who this covers: Casual dining, family-style restaurants, mid-size bars, and operations with 5–20 employees

What's typically included: Everything in Tier 2, plus:

- Commercial auto (for delivery or catering vehicles)

- Umbrella coverage for higher liability limits

- Employment practices liability

Venues with heavy alcohol sales or prior claims — especially in litigious states — typically hit the upper end of that range.

Estimated annual range: $8,000–$15,000+ depending on complexity

Types of Restaurant Insurance Coverage and Their Costs

Restaurant insurance is a bundle of coverages — each protecting against a different category of risk. Understanding per-policy costs lets you build the right program without overpaying.

Business Owner's Policy (BOP)

A BOP bundles general liability and commercial property into one policy — typically cheaper than buying them separately. Most restaurants should start here before adding specialized coverage.

- Average cost: $251/month ($3,010/year) for restaurant businesses, per Insureon's 2024 data

- What it covers: Customer injuries on premises, property damage, business interruption, and damage to your building and equipment

- Best for: Nearly every restaurant type as a foundation

General Liability Insurance

General liability covers the most common restaurant claims: customer slip-and-falls, property damage caused by your staff, and foodborne illness claims. One important limitation — it does not cover alcohol-related incidents.

- Average cost: $141/month for restaurant businesses

- Note: If you serve alcohol, you need a separate liquor liability policy regardless of your general liability coverage

Workers' Compensation Insurance

Workers' comp covers employee medical costs and lost wages from on-the-job injuries. It's legally required in most states once you have employees, though thresholds vary by state.

- Average cost: $113/month for restaurant businesses

- How it's priced: Calculated as a rate per $100 of payroll — more employees means a higher premium

- State rules vary: California requires coverage from the first employee; Florida requires it at four or more employees for non-construction employers; Virginia at three or more; Texas largely leaves it optional for private employers

Liquor Liability Insurance

Dram shop laws in 43 states can hold restaurants legally liable for damages caused by customers who were served alcohol on your premises. Without this coverage, a single lawsuit can easily exceed your annual revenue.

- Average cost: $41/month for restaurant businesses

- Who needs it: Any establishment with a liquor license — restaurants and bars alike

- Key factor: The higher the ratio of alcohol sales to total sales, the higher the premium

Additional Coverages to Consider

| Coverage | Avg. Monthly Cost | Who Needs It |

|---|---|---|

| Cyber liability | ~$129/month (food & beverage average) | Any restaurant with POS systems or online ordering |

| Commercial auto | ~$170/month (food & beverage average) | Restaurants with owned delivery vehicles |

| Food spoilage endorsement | Varies; added to BOP or property policy | Any restaurant with significant perishable inventory |

| Equipment breakdown | Varies; added to BOP or property policy | Full-service kitchens with commercial cooking equipment |

The last two items in the table — food spoilage and equipment breakdown — are endorsements added to an existing BOP or commercial property policy, not standalone products. Brokers with access to hospitality-focused carriers like Markel, Nationwide, and Liberty Mutual can typically include food spoilage as a named component — worth confirming when you compare quotes.

Key Factors That Affect Your Restaurant Insurance Premium

Two restaurants of similar size can have very different premiums. Underwriters assess operational risk — not just square footage or annual revenue.

Restaurant Type and Service Model

Your concept and service model directly shape your risk profile:

- Takeout-only and fast casual operations typically receive the most favorable rates — limited seating means lower slip-and-fall exposure

- Full-service restaurants with table service, alcohol, and larger kitchens carry higher liability and property exposure

- Fine dining with a high-value wine program increases both property values and alcohol-related liability

- Live entertainment adds another layer of risk that affects general liability pricing

Alcohol Service

Serving alcohol is one of the biggest premium drivers — it triggers liquor liability coverage and can increase general liability premiums.

The ratio of alcohol sales to total revenue matters. A restaurant where a glass of wine occasionally accompanies dinner is underwritten differently than a bar where alcohol generates the majority of revenue. The Hartford explicitly identifies the percentage of sales from alcohol and annual liquor volume as key factors in liquor liability pricing.

Number of Employees and Payroll

Workers' compensation is calculated per $100 of payroll, so a restaurant with 20 employees pays significantly more than one with three. More employees also increase exposure for general liability claims and employment practices liability, both of which factor into overall program cost.

Location

Geography affects premiums in several ways:

- Urban markets like New York or Chicago typically carry higher rates due to litigation frequency

- Flood zones and hurricane-prone areas (Florida, the Carolinas, Texas, Georgia) affect commercial property premiums

- State-specific workers' comp systems vary significantly in how rates are calculated and what thresholds apply

Claims History

A clean claims history is one of the most effective tools for controlling premiums long-term. Even one significant kitchen fire or slip-and-fall claim can raise your rates at renewal.

Documented safety practices signal lower risk to underwriters and can qualify your operation for better pricing:

- Fire suppression system maintenance and inspection records

- Employee safety training logs

- Slip-resistant flooring and hazard mitigation

- Formal incident reporting protocols

How to Lower Your Restaurant Insurance Costs

Bundle Policies Into a BOP

Purchasing a BOP typically costs less than buying general liability and commercial property separately. Adding endorsements like food spoilage to an existing BOP is typically cheaper than pricing those coverages as standalone policies. Ask your broker what can be bundled before pricing individual lines.

Implement Documented Risk Management Practices

Insurers price risk. Demonstrating that you actively manage it can result in lower premiums or more favorable underwriting consideration. Practical steps that insurers respond to include:

- Scheduling regular fire suppression system inspections

- Documenting employee safety training and incident protocols

- Installing security cameras and alarm systems

- Maintaining written records of kitchen cleaning and equipment maintenance

Compare Quotes Across Multiple Carriers

Rates for identical coverage can vary substantially between insurers. Some carriers specialize in hospitality and price restaurant risks more competitively than general commercial carriers. Working with an independent broker who has access to multiple markets — rather than a single carrier's direct sales channel — is the most reliable way to avoid overpaying.

Soma's risk management team works with restaurant clients to analyze operational exposures and compare options across hundreds of carrier partners — finding coverage that's competitively priced without gaps that show up only at claim time.

What Most Restaurant Owners Get Wrong About Insurance Costs

Restaurant owners commonly make three mistakes that lead to underinsurance or unexpected out-of-pocket costs:

Chasing the lowest premium. The cheapest quote often comes with lower coverage limits, higher deductibles, or missing endorsements. A restaurant that saves $500/year but lacks food spoilage coverage could face a five-figure loss from a single power outage. The right policy balances affordability with limits that match your actual exposure.

Starting with bare-minimum coverage. New owners often open with basic general liability and plan to "add coverage later." The first year is typically the highest-risk period: staff is still training, processes aren't established, and cash flow is tight. A proper BOP plus workers' comp from day one closes gaps before early-stage claims can expose them.

Skipping annual policy reviews. Insurance needs shift as a restaurant grows. Adding a location, launching delivery, hiring more staff, or obtaining a liquor license all change your risk profile. Policies that made sense at opening can carry outdated limits or miss new exposures entirely — leaving you underinsured when it matters most.

Frequently Asked Questions

How much does restaurant insurance cost?

A full restaurant insurance program typically runs $3,000–$10,000+ per year. Small, low-risk operations like food trucks or solo-operated cafés pay toward the lower end; full-service restaurants and bars with multiple employees pay more. Getting a custom quote is the only way to know your actual cost.

What insurance does a small restaurant need?

At minimum: a Business Owner's Policy (general liability + commercial property), workers' compensation if you have any employees, and liquor liability if you serve alcohol. Even a solo operator with no staff should carry general liability — it's often required by landlords before signing a commercial lease.

Is insurance cheaper for an LLC?

Forming an LLC does not directly reduce insurance premiums. Underwriters price based on operational risk — restaurant type, employees, alcohol service, location, and claims history — not legal structure. An LLC provides personal liability protection, but it complements rather than replaces commercial coverage.

What is the most important type of insurance for a restaurant?

General liability is the foundational coverage no restaurant should operate without. It covers the most frequent and costly claims — customer injuries, property damage caused by staff, and foodborne illness claims. It's also commonly required by commercial landlords as a condition of signing a lease.

Does restaurant insurance cover food spoilage?

Standard general liability and property policies typically do not include food spoilage — it requires a specific endorsement added to a commercial property or BOP policy, covering losses from power outages, refrigeration failure, or contamination events. Any restaurant with significant perishable inventory should carry it.

How can I lower my restaurant insurance premium?

The most effective approaches:

- Bundle coverages into a BOP rather than buying separate policies

- Document safety practices — carriers reward operations that demonstrate lower claim likelihood

- Compare quotes from multiple carriers through an independent broker with access to hospitality-specialist markets