Introduction

A single client claim alleging bad advice or a missed deliverable can cost more than most small businesses carry in reserve. That's the risk professional liability insurance is built to cover.

Unlike general liability—which covers bodily injury and property damage—professional liability protects against claims of negligence, errors, or omissions in the services you deliver. It addresses financial harm your advice or work may cause a client, not physical harm.

Choosing the right type of professional liability policy matters more than most business owners realize. The wrong trigger type or coverage form can leave you financially exposed—even while you're paying premiums. A 2025 Hiscox study found that 77% of U.S. small businesses are underinsured, with only 42% carrying professional liability insurance—and 83% unable to correctly describe what their policy actually covers.

This guide breaks down the main policy types, what each covers, and how to select the one that fits your profession and risk profile.

Key Takeaways

- Professional liability insurance protects your business when a client claims your advice or work caused financial harm

- Claims-made and occurrence policies respond to claims differently — and the distinction affects whether you're covered years after a project ends

- Coverage varies by profession: E&O for consultants, medical malpractice for healthcare, D&O for executives, and Tech E&O for technology providers

- Retroactive dates and policy wording differences can create gaps — even when you've never missed a premium

- Factor in tail coverage costs and your profession's claims history before choosing a policy structure

What Is Professional Liability Insurance?

Professional liability insurance covers financial losses a client suffers due to your mistake, oversight, or failure to deliver services as promised. It also pays for your legal defense if a claim is filed. Unlike general liability insurance, which covers bodily injury and property damage, professional liability focuses on economic harm and is not included in standard business owner's policies (BOPs).

Who Needs It

Any individual or business that provides expertise, advice, or services for a fee typically needs professional liability insurance. This includes:

- Consultants and advisors

- Healthcare professionals

- Financial planners and accountants

- Technology service providers

- Architects and engineers

- Real estate agents

- Attorneys

In some states and industries, professional liability insurance is legally required. For example, physicians must carry medical malpractice coverage in most states, and attorneys must maintain errors and omissions (E&O) insurance to practice law.

How It Differs from General Liability

These two coverages protect against fundamentally different risks:

| Coverage Type | What It Covers | Example |

|---|---|---|

| General Liability | Third-party bodily injury and property damage | A client slips and falls in your office |

| Professional Liability | Financial harm from professional errors or omissions | An accountant files an incorrect return, costing a client thousands in penalties |

If you provide professional services, you likely need both — one does not substitute for the other.

Why Professional Liability Insurance Matters

Operating without professional liability coverage exposes your business to catastrophic financial risk. A single negligence claim can result in attorney fees, court costs, and settlement payments that far exceed what most small businesses can absorb.

The numbers tell a stark story. The average of the top 50 medical malpractice verdicts jumped from $32 million in 2022 to $56 million in 2024, driven by "nuclear verdicts" that far exceed typical settlement amounts. Private company Directors & Officers claims now average $4.3 million, with median settlements at $3.1 million.

What Goes Wrong Without Coverage

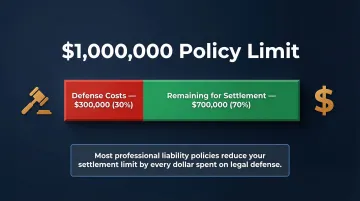

Even when you win a claim, defense costs alone can financially ruin a business. Most professional liability policies feature "defense within limits," meaning attorney fees reduce the amount available for settlements. In complex claims, legal costs routinely consume 25% to 33% of a $1 million policy before negotiations even begin.

Financial loss is only part of the damage. Litigation leaves a reputational mark that outlasts the case itself:

- Clients may question your competence, even after a favorable outcome

- Referral sources hesitate when your name appears in court records

- Competitors can use public filings against you during the sales process

Types of Professional Liability Insurance Policies

Professional liability insurance is not one uniform product. It varies both by how the policy responds to claims (the trigger type) and by the profession it is designed for (the coverage form). Understanding both dimensions is essential to selecting the right protection.

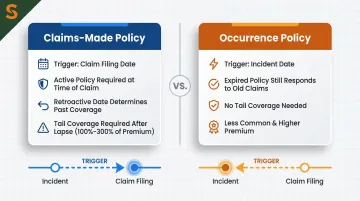

Claims-Made Policy

A claims-made policy covers claims reported to the insurer during the active policy period, regardless of when the underlying incident occurred—as long as it happened after the retroactive (prior acts) date. The retroactive date is the earliest point from which wrongful acts are eligible for coverage; services performed before that date are excluded even if the claim is filed during an active policy period.

Unlike occurrence policies, the policy in force when the claim is filed—not when the incident happened—responds to it. A lapse in coverage can therefore expose you to unprotected claims.

Best Suited For:

- Active practitioners who maintain continuous coverage

- Professionals in fields where claims surface months or years after service delivery (accountants, consultants, architects)

- Businesses that can commit to long-term carrier relationships

Key Strengths and Limitations:

Claims-made policies are the most affordable and most widely available option. However, if the policy lapses at retirement or career change, tail coverage (extended reporting period) must be purchased separately to maintain protection for past work.

Tail coverage key facts:

- Cost: 100%–300% of your expiring annual premium, paid as a one-time lump sum

- Election window: Most carriers require election within 30–60 days after cancellation

Occurrence Policy

An occurrence policy covers any incident that takes place during the policy period, regardless of when the claim is filed—even years after the policy expires. The trigger is the date the incident occurred, not the date the claim is reported. That distinction matters: an expired occurrence policy can still respond to a claim filed long after cancellation.

Best Suited For:

- Professionals who anticipate coverage gaps (retirement, career change, insurer switching)

- Professions where claims may emerge long after work is completed (engineers, architects on long-term construction projects)

- Businesses that want permanent protection without ongoing premiums

Key Strengths and Limitations:

Occurrence policies provide lasting protection without the need for tail coverage. Once you've paid the premium for a policy year, you're covered for incidents from that year permanently.

The trade-off: occurrence-based professional liability policies are rare and more expensive when available. Most carriers don't offer them for professional lines, which is why claims-made remains the industry standard.

Specialty Professional Liability Policies by Profession

Beyond the trigger type, professional liability insurance is shaped by the profession it covers. These specialty forms carry tailored definitions of what counts as a "professional service" and what constitutes a covered error.

Errors & Omissions (E&O) Insurance

E&O is the broadest and most common form of professional liability coverage. It applies to consultants, real estate agents, financial advisors, insurance professionals, and IT consultants—covering claims that services were performed incorrectly, incompletely, or not at all.

Typical annual premiums for $1 million coverage:

- Management consultants: $626

- IT consultants: $788

- Real estate agents: $753

Medical Malpractice Insurance

Covers healthcare professionals (physicians, dentists, nurses, therapists) against claims of clinical negligence or failure to meet the standard of care. Typically structured on a claims-made basis with higher limits given the severity of potential damages.

The average medical malpractice settlement in 2025 was approximately $463,000, though diagnostic errors average $499,000 and surgical procedure allegations average $350,000.

Directors & Officers (D&O) Liability Insurance

Protects executives and board members against claims that their management decisions caused financial harm to shareholders, employees, or regulators. Both for-profit corporations and nonprofits with active boards carry meaningful D&O exposure.

Typical annual premiums: $5,000 to $10,000 for private companies, depending on revenue size and complexity.

Technology E&O Insurance

Covers tech companies, SaaS providers, and IT consultants against claims that their software, systems, or technology services caused client financial losses. Often bundled with cyber liability coverage because 35.5% of data breaches originate from third-party vendors.

Choosing the right specialty form starts with accurately defining your services—what you do determines which coverage form applies and how broadly it will protect you.

What Professional Liability Insurance Covers—and What It Doesn't

What's Covered

A standard professional liability policy typically covers:

- Legal defense costs: Attorney fees, court costs, and expert witness fees—often the largest expense in a claim

- Settlements and judgments: Payments to claimants when a covered claim resolves, whether through negotiation or court order

- Negligence claims: Allegations that your work fell below the professional standard of care

- Errors and omissions: Mistakes, oversights, or gaps in the services or deliverables you provided

- Misrepresentation: False or misleading statements made in the course of delivering professional services

- Missed deadlines: Failure to complete work on time when the delay causes documented financial harm to a client

The Shrinking Limits Issue

Knowing what's covered is only half the picture—you also need to understand how much of that coverage you can actually access. In most professional liability policies (unlike general liability), defense costs come out of the same limit as indemnity payments, meaning legal fees reduce the amount available for settlements.

If you have a $1 million policy and spend $300,000 on defense costs, only $700,000 remains for settlement or judgment. This "defense within limits" structure makes limit selection critical.

Common Exclusions

Professional liability policies do not cover:

- Bodily injury and property damage: These fall under general liability, not professional liability

- Intentional or fraudulent acts: Coverage applies to mistakes, not deliberate misconduct

- Criminal acts: No professional liability policy responds to criminal proceedings

- Employee discrimination claims: These require Employment Practices Liability Insurance (EPLI)

- Prior known incidents: Claims you were aware of before the policy's effective date are excluded

- Cyber incidents and data breaches: Excluded by default unless you add a specific cyber endorsement

The Policy Wording Risk

Seemingly similar phrases carry different legal interpretations. A 2025 7th Circuit Court ruling analyzed a policy defining wrongful acts as "negligent act, error, or omission." The court ruled that "negligent" modifies all three terms—meaning intentional breaches of contract were not covered.

Before binding coverage, have an experienced broker or attorney walk through the policy's definitions section word by word—that's where most coverage gaps hide.

How to Choose the Right Professional Liability Policy

The right policy type depends on your profession's risk profile, how your claims are likely to surface over time, and whether continuous coverage can be maintained—not on what's cheapest or most familiar.

Key Factors to Evaluate

1. Coverage trigger — Claims-made dominates most professional fields. Verify your retroactive date covers all past work, especially when switching carriers.

2. Policy limits — Match limits to your typical contract sizes and client revenue exposure. Registered Investment Advisors experienced a 213% increase in paid E&O claims in 2023, with suitability claims surging 500%. Industry-specific claim patterns matter more than most buyers expect.

3. Deductible structure — Higher deductibles reduce premiums but increase out-of-pocket costs when claims arise.

4. Tail coverage availability — If retiring or closing your practice, confirm whether tail coverage is available and at what cost (typically 100%–300% of annual premium).

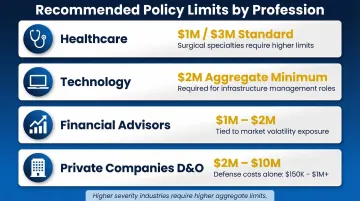

Profession-Specific Considerations

Some industries face higher claim frequency or severity and need higher aggregate limits:

- Healthcare: Standard limits are $1M/$3M, though surgical specialties often purchase higher limits

- Technology: Minimum $2M aggregate recommended if managing client infrastructure

- Financial Advisors: $1M to $2M given the correlation between market downturns and claim spikes

- Private Companies (D&O): $2M to $10M, as defense costs alone can consume $150,000 to $1M+

Coverage Gaps to Close

When switching insurers: Confirm the new policy's retroactive date covers past work. A lapsed retroactive date creates a permanent gap where past decisions become uninsured.

For tech businesses: Verify whether cyber liability is included or must be added separately. Many carriers now bundle Tech E&O with cyber coverage to prevent disputes about whether a loss stemmed from a "professional error" or a "network security failure."

For complex or hard-to-insure professions: Carrier requirements vary significantly across specialties, and some risks get declined by standard markets entirely. A brokerage like Soma — with access to hundreds of carriers including Chubb, Markel, and Liberty Mutual — can place coverage for these businesses through a single application rather than requiring quotes from multiple brokers.

Common Mistakes to Avoid When Selecting a Policy

Even a well-priced policy can leave you exposed if you make the wrong call at purchase time. These are the most costly mistakes professionals make when selecting coverage.

- Let claims-made coverage lapse without buying tail coverage. All past work loses protection the moment the policy ends. Most carriers require tail coverage to be purchased within 30 to 60 days of cancellation — missing that window closes the door permanently.

- Set limits based on standard defaults alone. A $1M/$1M structure may look clean on paper, but it may not reflect your actual contract sizes, client revenue exposure, or the reality that defense costs eat into your available coverage during litigation.

- Skip the fine print on policy wording. Two policies at similar price points can offer very different protection. Before signing, compare how each policy defines covered acts and what the exclusions actually say — not just the premium.

Conclusion

Professional liability insurance isn't a single product. The right policy hinges on matching the trigger type (claims-made vs. occurrence) to your exposure and selecting the specialty form built for your profession.

Three decisions determine whether your coverage holds up when a claim arrives:

- Trigger type: Claims-made policies require active coverage at the time of the claim; occurrence policies cover incidents when they happen, regardless of when reported

- Specialty form: E&O, D&O, EPLI, and medical malpractice each cover distinct exposures — using a general form for a specialty risk leaves gaps

- Exclusions and limits: Understanding what's carved out is as important as knowing what's included

With claim severity rising across professional sectors, this isn't a box to check at renewal. If you're unsure which policy structure fits your business, Soma's team can match you with the right carrier and form — without the back-and-forth.

Frequently Asked Questions

What is a professional liability policy?

A professional liability policy is specialized insurance coverage protecting professionals against claims of negligence, errors, or omissions in the services they provide. It covers legal defense costs, settlements, and judgments arising from alleged professional mistakes.

What are the different types of professional liability policies?

The two main trigger types are claims-made (covers claims reported during the active policy period) and occurrence (covers incidents that occur during the policy period). Profession-specific forms include E&O for consultants, medical malpractice for healthcare, D&O for executives, and Tech E&O for technology providers — with claims-made being the most prevalent.

What is covered under a professional liability policy?

Professional liability policies cover attorney fees, court costs, expert witness fees, settlements, and judgments from errors, omissions, negligence, misrepresentation, and missed deadlines. Note that defense costs typically reduce the policy limit — meaning legal fees erode what's left for settlements.

What does professional liability insurance not cover?

Professional liability insurance excludes bodily injury, property damage, intentional acts, employment discrimination, known prior incidents, and cyber events unless endorsed. These exposures require separate policies — general liability, EPLI, or cyber insurance.

What are common professional liability claims?

Common claims include an accountant filing an incorrect tax return, a consultant's flawed advice causing business losses, or an architect's design error triggering construction cost overruns. Software developers also face claims when a delivered product doesn't meet contracted specifications.

How much does a $1,000,000 liability insurance policy cost?

Costs vary by profession, claims history, geography, and number of employees. Annual premiums for $1 million in coverage vary widely by profession:

- Notary services: ~$234/year

- Management consultants: ~$626/year

- IT consultants: ~$788/year

- Architects and engineers: ~$1,311/year

- Financial advisors: $1,612–$2,610/year