Introduction

Imagine this: A software development firm delivers a custom inventory management system to a retail client. Three weeks post-launch, an overlooked bug crashes the client's entire point-of-sale network during the holiday shopping rush. The outage lasts three days. Lost revenue: $180,000. The client sues for damages, breach of contract, and recovery costs—and the developer's business faces financial ruin.

Tech E&O insurance exists precisely for scenarios like this. Yet many tech businesses remain dangerously underprotected—often assuming cyber insurance covers professional failures (it doesn't) or that general liability will respond (it won't).

This guide breaks down what Tech E&O insurance actually covers, who needs it, how it differs from cyber insurance, and how to get the right policy for your business.

Key Takeaways

- Tech E&O protects technology businesses from client lawsuits arising from software bugs, missed deadlines, defective products, or service failures

- Covers legal defense, settlements, damages, and breach of contract — cyberattacks and ransomware require separate cyber insurance

- Essential for SaaS companies, IT consultants, software developers, MSPs—plus non-tech firms offering technology services

- Bundling Tech E&O with cyber insurance typically runs $67/month — and closes the gaps a standalone policy leaves open

- Premiums vary by revenue, data exposure, claims history, and policy limits

What Is Technology Errors & Omissions Insurance?

Technology Errors & Omissions insurance is a specialized professional liability policy designed for companies that develop, sell, distribute, or provide technology products and services. It responds when a client claims your technology product or service failed to perform as promised, caused financial harm, or didn't deliver contractual results.

How Tech E&O Differs from Standard Professional Liability

While general professional liability (E&O) covers any professional giving advice or services—accountants, consultants, real estate agents—Tech E&O is purpose-built for technology exposures. According to the International Risk Management Institute (IRMI), Tech E&O uniquely covers both liability exposures (third-party financial losses) and property loss exposures (data loss, system failures, network security breaches).

That dual structure is what separates Tech E&O from standard E&O forms, which typically exclude technology-specific risks like software product failures or network security incidents.

Two Ways Insurers Define Coverage Scope

Insurers structure Tech E&O policies using two primary approaches:

| Approach | How It Works | Best For |

|---|---|---|

| Policy Definitions | Broadly defines "technology products/services" using expansive language; new offerings covered automatically | Startups that frequently launch products or pivot services |

| Enumerated Services | Explicitly lists covered products and services in the policy declarations; unlisted offerings may not be covered | Established firms with a stable, well-defined service portfolio |

Most policies use hybrid approaches. If you launch a new software module not listed in your declarations, a claim related to that module could be denied. Work with a broker to ensure your policy language keeps pace with your actual offerings.

Hidden Tech E&O Exposures for Non-Tech Businesses

You don't need to be a software company to face Tech E&O liability. Any business that delivers technology as part of its service — even incidentally — carries exposure:

- A hospital providing IT infrastructure to local clinics

- An engineering firm selling access to a proprietary BIM application

- A retailer processing transactions through a custom e-commerce platform

- A financial services firm offering clients a proprietary portfolio management app

In each case, a system failure or software error that causes a client financial harm can trigger a Tech E&O claim — regardless of whether "tech company" appears anywhere in the business description.

Claims-Made Coverage and Why Continuous Coverage Matters

Tech E&O policies are written on claims-made forms. This means:

- The claim must be both made and reported during the active policy period

- Coverage only applies to errors occurring on or after the policy's retroactive date

- If you cancel or let your policy lapse, you lose protection for past work unless you purchase extended reporting period (tail) coverage

Maintaining continuous coverage is critical. Gaps create permanent blind spots for work performed during those periods.

What Does Tech E&O Insurance Cover — and What Doesn't It Cover?

Tech E&O fills the gap left by Commercial General Liability policies, which only respond to bodily injury or physical property damage—not pure economic loss caused by a software glitch or service failure.

Core Coverages Tech E&O Provides

Tech E&O responds to:

- Errors or mistakes that cause a client financial loss

- Omissions or negligent acts in delivering services

- Failure to deliver on contractual terms or meet a deadline

- Breach of contract or warranty

- Legal defense fees and attorney costs

- Court-ordered settlements or judgments

- Accidental copyright infringement or misrepresentation

The Four Standard Insuring Agreements

Most Tech E&O policies bundle four major liability coverages:

| Coverage Type | What It Protects |

|---|---|

| Technology Services Liability | Negligent acts, errors, or omissions in IT services, consulting, data processing, or software integration |

| Technology Products Liability | Failure of software, hardware, or SaaS products to perform their intended function |

| Media Content Liability | Copyright infringement, trademark violations, plagiarism, or defamation from media material |

| Network Security Liability | Failure to prevent unauthorized access, malicious code transmission, or denial-of-service attacks affecting third parties |

Some policies also include crisis management expense and business interruption coverage triggered by covered events.

These coverages become concrete when you see how claims actually play out. Here are two examples drawn from real Tech E&O cases.

Real-World Tech E&O Claim Scenarios

Scenario 1: Retail System Fails Post-Launch, $2M Settlement Follows

An IT company spent years developing a retail operations system. Post-launch, the software lacked required functionality and failed to track inventory or issue invoices. The client sought $5M in damages; the claim settled for $2M, plus $200,000 in defense costs.

Scenario 2: IT Consultant Misses Open Port, Law Firm Sues for $3M

A law firm hired an IT consultant to install network-attached storage. The consultant failed to connect a VPN to close an open port, leading to a third-party data breach. The law firm sued for $3M in lost income; the claim settled for $800,000, plus $100,000 in defense costs.

What Tech E&O Does NOT Cover

Standard exclusions include:

- Intentional wrongdoing or deliberate negligence (policies cover mistakes, not willful or fraudulent acts)

- Criminal charges or illegal activities, including intentional cybercrime

- Bodily injury or personal injury (those fall under general liability)

- Employment-related claims like discrimination, harassment, or wrongful termination (covered under EPLI)

- Patent and trade secret infringement — copyright is often covered, but patent claims are typically excluded

- Unmet guarantees or warranties, such as promised ROI or cost savings, unless the failure stems from a provable negligent act

Tech E&O Complements, Not Replaces, General Liability

A comprehensive protection strategy requires both Tech E&O and general liability insurance. Each policy fills gaps the other leaves open. Together, they ensure a mistake on a job site and a coding error in your software both have a policy responding — so a single uncovered claim doesn't become an existential cost.

Who Needs Tech E&O Insurance?

Primary Audience: Technology Product and Service Providers

Businesses that design, develop, or deliver technology products or services:

- Software developers and SaaS companies

- IT consultants and managed service providers (MSPs)

- Web and app developers

- Cybersecurity firms

- Data storage and cloud hosting companies

- E-commerce platforms

- Electronics manufacturers

- Telecommunications providers

According to NEXT Insurance data, 73% of small tech businesses carry professional liability coverage, indicating widespread recognition of this exposure.

Non-Tech Firms with Technology Exposures

Any organization whose clients rely on its technology systems faces potential Tech E&O exposure:

- Healthcare systems running telehealth platforms or patient triage apps

- Engineering firms using BIM software or drone-based data collection

- Financial services firms operating proprietary trading platforms or client portals

- Manufacturers embedding software in physical products like IoT devices or smart equipment

Practical Triggers That Make Tech E&O Essential

Certain situations signal that coverage has moved from optional to necessary:

- Client contracts requiring proof of E&O coverage before work begins

- Scaling a remote workforce where quality control is harder to enforce

- Entering a new industry vertical or client segment with higher stakes

- Launching new products or services that broaden your technology scope

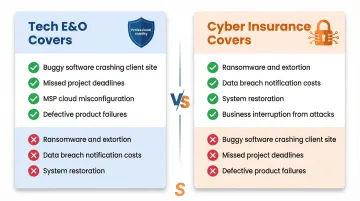

Tech E&O vs. Cyber Insurance: Understanding the Difference

Many technology businesses assume cyber insurance covers all technology-related failures. It doesn't. The two policies protect against fundamentally different risks.

The Fundamental Distinction

- Tech E&O Insurance covers third-party liability claims when your technology product or service fails — client lawsuits for professional negligence, defective software, or missed deadlines.

- Cyber Insurance covers first-party losses from cyberattacks (ransom payments, system restoration, business interruption) plus third-party liability for data privacy violations.

The "Professional Services" Exclusion in Cyber Policies

Standalone cyber policies explicitly exclude professional mistakes. For example:

- Beazley's Breach Response policy lists "professional services" under "What is not insured"

- Hiscox's cyber policy excludes claims "made by any individual or entity to whom or which you have provided professional advice or services"

If a client sues because your buggy software crashed their system, cyber insurance won't respond.

Scenario Mapping: Tech E&O vs. Cyber

| Claim Scenario | Tech E&O Covers? | Standalone Cyber Covers? |

|----------------|------------------|--------------------------|

| Buggy software release crashes client's e-commerce site, causing lost sales | Yes (Professional Negligence) | No (Professional Services Exclusion) |

| Missed project deadline causes client financial harm | Yes (Breach of Contract) | No |

| Hacker locks your own servers and demands ransom | No | Yes (First-Party Cyber Extortion) |

| MSP misconfigures client's cloud database, leading to data breach | Yes (Tech Services Liability) | No (Professional Services Exclusion) |

The Strategic Advantage of Bundled Policies

Technology errors (like a misconfigured firewall) frequently trigger cyber events (like a data breach), so claims often straddle both coverages. A bundled "Tech E&O + Cyber" policy from a single carrier:

- Eliminates coverage disputes between two insurers over whether a claim was "cyber" or "professional"

- Yields premium savings of 10-20% compared to buying separately

- Ensures no gaps between professional failures and data breaches

If your product's failure causes a client to lose money, cyber insurance will not respond to that claim. Tech E&O is the policy that closes that gap.

How Much Does Tech E&O Insurance Cost?

Tech E&O pricing depends on business size, services offered, data exposure, and coverage limits. Recent market data provides clear benchmarks for small tech businesses.

Current Premium Benchmarks for Small Tech Firms

Bundled Tech E&O + Cyber Coverage: Small IT businesses pay an average of $67 per month ($807 annually) for bundled Tech E&O and cyber coverage, with 56% selecting $1M per-occurrence / $1M aggregate limits.

Standalone E&O Coverage: For standalone professional liability across all small businesses, the average is $88 per month. For small IT consultants with $150,000 annual revenue, a $500,000 limit with $5,000 deductible averages $42.92 per month ($515 annually).

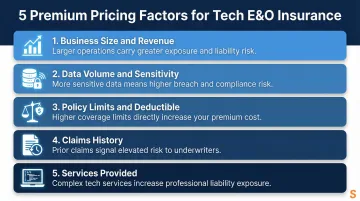

Key Factors That Influence Premium Pricing

- Business size and revenue — Higher revenue signals larger contracts and greater potential claim severity.

- Data volume and sensitivity — Handling healthcare or financial records increases premiums noticeably.

- Policy limits and deductible — Most small businesses choose $1M/$1M limits; higher deductibles lower your premium but raise out-of-pocket costs at claim time.

- Claims history — Prior E&O claims signal elevated risk to underwriters and push premiums up immediately.

- Services provided — Financial software and healthcare IT carry higher premiums than general tech consulting.

Practical Tips for Keeping Costs Down

- Bundle Tech E&O with cyber in a single policy — often 10-20% cheaper than buying separately

- Pay annual premiums upfront rather than monthly to reduce total cost

- Keep coverage continuous — gaps require expensive retroactive coverage to fill

- Implement MFA, endpoint detection and response (EDR), and air-gapped backups — strong cybersecurity practices lower claims risk and improve your insurability

Work with a Multi-Carrier Broker

The tips above only go so far if you're only getting one quote. A broker with access to multiple carriers can compare pricing across the market and match your specific risk profile to the right policy. Soma works with carriers including Chubb, Markel, Liberty Mutual, Kinsale, and Nationwide, so tech businesses can weigh real options rather than defaulting to whatever's available first.

How to Get Tech E&O Coverage

What to Prepare Before Applying

Gather the following information before requesting quotes:

- Description of your technology services and products

- Annual revenue and number of employees

- Any existing contracts with clients that require coverage

- Prior claims history (if any)

- Specific services or products you provide (for enumerated policies)

Some insurers define scope broadly through policy language; others list specific services. Knowing exactly what your business does helps match the right policy structure.

Get Coverage Through Soma

Soma is a specialized brokerage for tech businesses seeking E&O coverage. Quotes run through hundreds of carrier partners, including Chubb, Hiscox, Kinsale, and Liberty Mutual, with a focus on complex and hard-to-insure businesses.

Tech companies with non-standard risks get coverage placed fast. Soma binds same-day startup packages and adjusts limits as your headcount, revenue, and data footprint grow — no new application required.

Working with Soma gives you:

- Same-day quotes for startup and early-stage tech businesses

- Coverage that adjusts as you scale, without restarting the process

- Access to carriers that specialize in tech professional liability

- One application compared across multiple carriers simultaneously

Submit one application to see your options side by side and choose the policy that fits your risk profile and budget.

Frequently Asked Questions

What does technology errors & omissions insurance cover?

Tech E&O covers legal defense costs, settlements, and damages arising from client claims of errors, omissions, missed deadlines, breach of contract, and defective technology products or services.

What does E&O not cover?

Tech E&O generally excludes intentional wrongdoing, criminal acts, bodily or personal injury, illegal activities, and employee-related claims like discrimination. Those risks fall under other policies such as general liability or EPLI.

Who needs technology E&O insurance?

Dedicated tech firms — software developers, IT consultants, SaaS companies, and MSPs — need Tech E&O coverage. So do non-tech businesses that deliver technology services or products to clients.

What is the difference between tech E&O and professional E&O?

Standard professional E&O covers any professional providing advice or services. Tech E&O is built specifically for technology businesses and adds coverage for product failures, network security incidents, and media content liability that generic professional liability policies don't address.

How much does tech E&O insurance cost?

Costs vary based on business size, services offered, data exposure, and coverage limits. Small IT businesses typically pay $67 per month for bundled Tech E&O and cyber coverage, with most selecting $1M/$1M limits.

Is tech E&O the same as cyber insurance?

No. Tech E&O addresses third-party claims from clients alleging professional failure. Cyber insurance covers the policyholder's own costs from a cyberattack and data breach liability. Many businesses benefit from carrying both, ideally bundled together.