Introduction

A commercial development in Phoenix is 60% complete when a fire breaks out in the electrical system. Damage totals $400,000, and the project grinds to a halt for three months. Without builders risk insurance, the property owner faces the full cost of repairs, extended loan interest, and lost rental income — with no policy to absorb the loss.

That's what builders risk insurance is designed to cover. It's a specialized property policy protecting buildings and materials during construction against perils like fire, theft, vandalism, and weather damage. This guide breaks down who needs it, what's excluded, and what it typically costs.

Key Takeaways

- Builders risk covers structures, on-site materials, and equipment in transit during construction

- All-risks basis: everything is covered unless the policy explicitly excludes it

- Standard exclusions include flood, earthquake, faulty workmanship, and employee theft

- Property owners, general contractors, or both can hold the policy — coverage ends at project completion or occupancy

- Premiums typically range from 1–4% of total construction value

What Is Builders Risk Insurance?

Builders risk insurance is a specialized property insurance policy that covers buildings and structures while they are under construction. Also called "course of construction insurance" or "Contractor's All Risk (CAR) insurance," it differs from standard commercial property insurance in one key way: it's written on an inland marine form, which allows coverage to follow the project across locations and construction phases.

Standard property policies don't cover in-progress work — a building under construction isn't a completed structure, so homeowners and commercial property policies typically exclude it. The exposure is real: fires and explosions account for 27% of construction insurance claims by value, and water damage drives over 30% of construction claims, totaling approximately $16 billion annually.

Without dedicated coverage, those losses fall entirely on the project owner or contractor.

How the policy is structured:

- Covers all perils except those specifically excluded (all-risks basis)

- Limits are set to the project's estimated completed value — not its current construction stage

- Follows property in transit and at temporary locations under the inland marine classification

- Terms are written to match the construction timeline, not a fixed annual period

When Does Builders Risk Coverage Begin and End?

Coverage typically starts when the construction contract is signed or materials are first delivered to the job site. However, the exact trigger date must be confirmed with the insurer. Gaps between contract signing and construction start can leave the project exposed, especially if materials are delivered early or site work begins before the policy takes effect.

Builders risk policies terminate when the first of these occurs:

- Policy expiration or cancellation

- The building is accepted by the purchaser

- The insured's interest in the property ceases

- The insured abandons construction with no intention to complete it

- 90 days after construction is complete, or 60 days after any building is occupied in whole or in part

When any of these triggers occurs, coverage ends — sometimes before the project feels "done." At that point, the owner should transition immediately to a permanent commercial property policy. For projects with phased move-ins, a "Permission to Occupy" endorsement maintains protection through final completion.

What Does Builders Risk Insurance Cover?

Builders risk policies cover physical damage to structures under construction, building materials, supplies, scaffolding, temporary structures, and construction forms. Coverage follows the material even before it's installed—meaning lumber staged on-site is protected before it becomes part of the framing.

Covered property at the construction site includes:

- The structure itself (foundations, framing, installed fixtures)

- Building materials and supplies on-site

- Scaffolding and temporary structures

- Construction forms and equipment used to service the building

Covered Property Locations

Builders risk coverage extends beyond the physical job site. Materials in transit to the project and supplies stored at temporary off-site locations are also typically covered under a standard policy, which reduces coverage gaps for contractors who stage materials across multiple locations.

However, transit and off-site storage coverage often come with sublimits—commonly $5,000 to $25,000, or 5% of total completed value. For projects with significant material staging needs, these sublimits should be reviewed and increased if necessary.

Covered Perils

Most policies cover on an open-perils (all-risk) basis, meaning everything is covered unless specifically excluded. Commonly covered causes of loss include:

- Fire, lightning, and explosion

- Windstorm and hail

- Theft and vandalism

- Smoke damage

- Aircraft or vehicle impact

- Riot or civil commotion

- Accidental water damage

Soft Costs Coverage

If property damage causes a construction delay, a builders risk policy can be extended to cover additional expenses not directly tied to physical repair. These "soft costs" include:

- Lost rental income

- Additional loan interest

- Real estate taxes

- Lost sales

- Extended general overhead

- Architect, engineer, and consultant fees

Soft cost endorsements typically include a waiting period (time-based deductible) before coverage triggers. Limits can be applied separately to each cost type or on a blanket basis. For a $1 million project delayed by three months, soft costs can easily exceed $50,000—worth adding for any income-producing property.

Optional Coverage Extensions

Beyond soft costs, several endorsements expand what a standard policy covers. None of these are automatic—each must be explicitly added:

- Debris removal and disposal — clears damaged materials from the site after a covered loss

- Pollutant cleanup — addresses environmental contamination tied to a covered event

- Scaffolding — extends protection to temporary structures not included by default

- Architect and engineering fees — covers redesign costs when reconstruction requires new plans

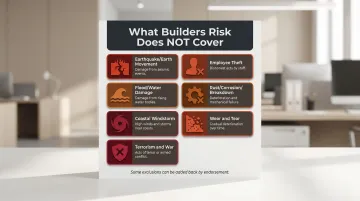

What Builders Risk Insurance Does NOT Cover

Because builders risk is written on an all-risks basis, understanding exclusions is critical. The policy covers everything not excluded, so gaps often surprise policyholders at claim time.

Standard Exclusions

Most builders risk policies exclude:

- Earthquake and earth movement: Landslide, mine subsidence, earth sinking or shifting

- Flood and water damage: Surface water, storm surge, mudslide, sewer backup

- Wind in coastal/hurricane zones: Named windstorm coverage often excluded in high-risk areas

- Acts of terrorism and war: Catastrophic events with extreme loss potential

- Employee theft: Dishonest or criminal acts by employees or subcontractors

- Rust, corrosion, and mechanical breakdown: Gradual deterioration or equipment failure

- Ordinary wear and tear: Normal aging, decay, and latent defects

The Faulty Workmanship Exclusion

Builders risk policies exclude the cost to repair or redo defective work itself. However, the resulting damage to other property caused by faulty workmanship is typically covered under the "ensuing loss" provision.

Example: If a contractor installs a pipe incorrectly and it bursts, the policy will not pay to replace the defective pipe. But it will cover the resulting water damage to the surrounding structure, framing, and drywall.

Getting this distinction wrong at claim time can mean the difference between a covered loss and an out-of-pocket repair bill.

Exclusions That Can Be Added Back by Endorsement

You can add back several standard exclusions by purchasing specific endorsements:

| Catastrophe Peril | Typical Deductible Structure |

|---|---|

| Earthquake | 2-20% of the value of the property (not the loss amount); minimum 10% in high-risk states |

| Flood | Separate, higher deductible; aggregate limit for all flood losses during the policy year |

| Windstorm/Hail | 1%, 2%, or 5% of the value of the covered property at the time of loss |

These endorsements often come with sublimits and higher deductibles. Coverage availability depends on the project's geographic location and proximity to flood zones or fault lines.

Critical reminder: Builders risk is not standardized. Most insurers write proprietary forms, meaning covered perils and exclusions can vary significantly between carriers. Compare policy forms side-by-side — not just the price — before committing to a carrier.

Who Needs Builders Risk Insurance?

Anyone with a financial interest in the construction project should be covered under a builders risk policy:

- Property owner: Holds the insurable interest in the land and structure

- General contractor: Manages the project and often has contractual obligations to carry coverage

- Subcontractors of all tiers: May be named insureds to eliminate disputes over property ownership during construction

- Lenders/mortgagees: Typically named as loss payees to protect their financial interest

- Architects (in some cases): When they have a financial stake in the project

A single policy covering all parties is the practical standard — it simplifies the claims process and removes disputes over who owns damaged property when something goes wrong mid-project.

Is Builders Risk Insurance Legally Required?

Builders risk insurance isn't universally required by law, but it's routinely required by:

- Lenders as a loan condition: Fannie Mae requires builders risk insurance equaling at least 100% of the completed value for new construction or significant renovation

- Local building codes: Some municipalities mandate coverage before issuing permits

- Contractual requirements: The American Institute of Architects (AIA) Document A101-2017 requires the owner to purchase builders risk "all-risks" completed value coverage, though this obligation can be shifted to the contractor

Do You Need Builders Risk Insurance for Renovations?

Yes, builders risk insurance applies to both new construction and renovation/remodeling projects. For renovations on an existing building, the owner's existing commercial property or homeowners policy may already provide some coverage for the work in progress — though policies vary widely.

For large-scale or structural renovations, a dedicated builders risk policy is strongly recommended. The ISO CP 11 13 (Builders Risk Renovations) endorsement is designed specifically for this scenario. It covers:

- Renovation value only: Machinery, fixtures, and materials added during the project

- Not the existing structure: The original building is excluded from this endorsement

- Separate policy required: The existing structure must stay insured under a standalone commercial property policy

How Much Does Builders Risk Insurance Cost?

Builders risk insurance typically costs 1-4% of total construction value annually. For a $500,000 project, expect premiums between $5,000 and $20,000. For a $1 million project, premiums generally range from $10,000 to $40,000.

Key Factors That Affect Your Premium

- Construction value sets the base premium — coverage must equal the anticipated completed value, not current progress

- Building materials matter: wood-frame structures cost more to insure than steel or masonry due to higher fire risk

- Project type shapes risk profile — residential vs. commercial and new construction vs. renovation are rated differently

- Location drives surcharges — coastal projects pay more for wind coverage; California adds wildfire and seismic exposure

- Timeline affects cost — longer construction periods mean longer exposure, which increases premiums

- Deductible level creates a tradeoff — higher deductibles lower premiums but raise out-of-pocket costs at claim time

- Endorsements add up — soft cost coverage and ordinance upgrades can increase base premiums by 10-25%

Setting Appropriate Coverage Limits

The coverage limit should equal the total anticipated completed value of the project, not the value at the current construction stage. Underinsuring triggers a co-insurance penalty: if your policy limit falls below the actual completed value, the insurer pays only a proportional share of any loss.

Example — Co-Insurance Penalty in Action: A project's completed value is $200,000, but the owner insured it for $100,000. That's 50% of the actual value — so the insurer covers only 50% of any loss. An $80,000 fire claim pays out just $40,000, minus the deductible.

How to Get the Right Builders Risk Policy

Working with a specialist broker matters for builders risk. Because most insurers write their own proprietary forms, coverage terms can differ dramatically between carriers. An experienced broker who specializes in construction insurance can compare policy language — not just price — and catch coverage gaps before a loss occurs.

Soma works with carriers including Chubb, Liberty Mutual, and Kinsale to place builders risk coverage for construction businesses of all sizes. The focus is on satisfying lender, owner, and contract requirements while building programs that fit your full project pipeline — not just a single job.

Pre-Purchase Checklist

Before binding coverage, review these critical elements:

- Named insureds: Confirm the policy lists the owner, general contractor, and subcontractors of every tier. Avoid "As Their Interests May Appear" (ATIMA) language — it can limit coverage and open the door to subrogation.

- Waiver of subrogation: Verify a blanket waiver is included so the insurer cannot pursue a negligent subcontractor after paying a claim.

- Catastrophe perils: Check that flood, earthquake, and named windstorm are covered. Confirm sublimits are adequate and that percentage deductibles apply to the loss amount — not total project value.

- Transit & off-site coverage: Ensure sublimits for property in transit and temporary off-site storage match the project's supply chain exposure.

- Soft costs: Confirm adequate limits for delay-related expenses and verify the time-deductible is reasonable for the project timeline.

- Escalation clause: Look for an "escalation" or "limits margin" provision that automatically adjusts for change orders and material cost fluctuations.

Timing Is Critical

Builders risk coverage should be secured before ground is broken or materials are ordered. Gaps in coverage at the start of a project are one of the most common and costly mistakes. Retroactive coverage is generally not available after a loss has occurred.

Frequently Asked Questions

What does a builder's risk insurance cover?

Builders risk insurance covers physical damage to structures under construction, on-site materials and equipment, supplies in transit, and can be extended to cover soft costs like delayed rental income. It typically operates on an all-risks basis.

What is not covered by a builder's risk policy?

Common exclusions include earthquake, flood, employee theft, faulty workmanship (the repair cost itself), war, terrorism, and mechanical breakdown. You can add some back by endorsement.

Do I need builders risk insurance?

Any party with a financial interest in a construction project—owner, contractor, or lender—should carry builders risk insurance. Lenders and construction contracts often require it as a condition.

Do you need builders risk insurance for renovations?

Yes, renovations can be covered under a builders risk policy. Check first whether your existing property policy covers the work—for large-scale or structural renovations, a dedicated builders risk policy is the safer choice.

Who typically pays for builders risk insurance?

Either the property owner or the general contractor can purchase the policy. The property owner is generally the better choice since they hold the insurable interest in the land and structure.

Who should be named insured on builders risk?

Name all parties with a financial interest on a single policy—property owner, general contractor, subcontractors, and lenders. One shared policy eliminates ownership disputes during construction and speeds up claims handling.