Introduction

Construction ranks among the riskiest industries for liability and property losses. In 2024, the Bureau of Labor Statistics recorded 1,032 fatal work injuries among construction and extraction workers, with a fatal injury rate of 9.2 deaths per 100,000 full-time equivalent workers. Beyond fatalities, the Liberty Mutual Workplace Safety Index reports that construction loses nearly $11.4 billion annually to serious, nonfatal workplace injuries.

Insurance requirements come from two distinct sources: state and federal law, and project contracts. Confusing these two tiers can cost contractors bids, projects, or their entire business. Legal mandates set the baseline floor, but contractual requirements from clients often exceed those minimums — and failing to carry the right coverage disqualifies contractors before they even submit a proposal.

Understanding both tiers — and what each demands — is how contractors protect their licenses, win bids, and stay on the job.

Key Takeaways

- Workers' compensation and commercial auto insurance are legally required in virtually every state

- General liability, builders risk, and inland marine are contractually required by project owners — not law, but non-negotiable for winning contracts

- Most commercial contracts require at least $1 million per occurrence / $2 million aggregate in general liability; government projects often set higher thresholds

- GCs must require subcontractors to carry their own coverage and verify it with certificates of insurance

- Premiums differ significantly by trade, payroll size, and claims history — get quotes specific to your work type

Legally Required vs. Contractually Required: Understanding the Two Tiers of Construction Insurance

The First Tier: Legally Mandated Coverage

Two types of insurance are required by law for construction businesses:

Workers' Compensation is legally mandated in nearly every U.S. state for businesses with employees, though thresholds vary significantly by jurisdiction. Key examples:

- Florida: Requires coverage for construction businesses with one or more employees — non-construction businesses don't trigger the requirement until four or more

- California: Certain contractor classifications — concrete, HVAC, asbestos, roofing, and tree service — must carry coverage even with zero employees

- Texas: Makes workers' comp optional for private employers, but requires it for construction companies on government contracts

Commercial Auto Insurance is required by federal law and all states for vehicles used in business operations. Personal auto policies universally exclude business-use claims — a serious coverage gap for contractors who assume their personal policy carries over to work vehicles.

Contractors operating across state lines must verify requirements in each state — there is no universal employee-count threshold that applies everywhere.

The Second Tier: Contractually Mandated Coverage

State law doesn't require general liability or builders risk insurance for most contractors, but major clients — municipalities, universities, large developers — almost universally require these policies before awarding contracts. A contractor without the right coverage gets disqualified before the bid is even reviewed.

Common contractually required policies include:

- Commercial General Liability (CGL) — covering third-party bodily injury and property damage

- Builders Risk — protecting the structure under construction

- Inland Marine — covering tools, equipment, and materials in transit

- Umbrella/Excess Liability — extending limits beyond primary policies

Certificates of Insurance and Additional Insured Endorsements

Contractors prove coverage to clients through Certificates of Insurance (COIs) — standardized forms showing policy types, limits, and effective dates. Two things to know about how they actually work:

- The ACORD 25 Certificate explicitly states it "DOES NOT CONSTITUTE A CONTRACT" and that limits shown may not reflect actual policy amounts

- Adding a project owner as an "additional insured" extends the contractor's liability coverage to protect the owner from claims arising from the contractor's work — this requires a specific endorsement to the CGL policy and is nearly universal in commercial construction contracts

Recommended-But-Not-Required Coverage

Professional liability (errors and omissions) and umbrella/excess liability policies are often left out of contracts but can protect against the most financially devastating claims — especially on design-build projects where the contractor owns both design and construction risk.

Essential Commercial Insurance Policies Every Construction Business Needs

Commercial General Liability (CGL) Insurance

CGL is the most universally required policy in construction contracts. It covers third-party bodily injury, property damage, and advertising injury arising from business operations. Critically, it does NOT cover the contractor's own employees (that's workers' comp) or faulty workmanship resulting in financial loss (that's professional liability).

Construction contractors pay some of the highest CGL rates of any profession due to job-site risk. Policies are structured with:

- Per-occurrence limit: maximum the insurer pays for a single event

- General aggregate limit: maximum the insurer pays for all claims during the policy period

The most common contract baseline is $1 million per occurrence / $2 million aggregate. The AIA Document A101-2017 Exhibit A explicitly requires contractors to specify limits for each occurrence, the general aggregate, and the products-completed operations hazard.

Workers' Compensation Insurance

Workers' comp is legally required in nearly all U.S. states for businesses with employees. The exact employee count threshold varies by state, with construction businesses often subject to stricter requirements than other industries.

Coverage includes:

- Medical expenses for employees injured on the job

- Lost wages during recovery

- Rehabilitation costs

- Protection for employers from most employee lawsuits related to workplace injuries

Construction has one of the highest workplace injury rates of any industry. The BLS reports a Total Recordable Incident Rate (TRIR) of 2.2 cases per 100 FTE workers for the construction sector. That risk profile pushes construction premiums well above what most other industries pay — often 2x to 3x comparable rates.

Builders Risk (Course of Construction) Insurance

Builders risk insurance covers the structure being built — including materials, fixtures, and temporary structures like scaffolding — against damage from fire, theft, vandalism, and windstorm. It is typically required in project contracts and purchased by either the project owner or the general contractor, depending on contract terms.

Key coverage details:

- Standard policies do NOT cover floods or earthquakes unless specifically endorsed

- Policies are project-specific and terminate at project completion or when the structure is occupied

- Coverage limits should reflect the full completed value of the project

Water damage accounts for over 30% of all builders risk claims, making it the leading cause of losses. That exposure drives up deductibles market-wide and is worth addressing explicitly in your policy endorsements.

Under standard AIA A201-2017 and A101-2017 contracts, the project owner is generally required to purchase the builder's risk policy unless the parties explicitly agree otherwise.

Commercial Auto Insurance

Commercial auto insurance is legally required for all business-owned vehicles in every state. Personal auto policies typically exclude business-use accidents, leaving contractors exposed if they assume their personal coverage applies.

For construction businesses, this covers:

- Trucks, dump trucks, flatbeds, cement mixers, and other job-site vehicles

- Liability for bodily injury and property damage caused by company vehicles

- Physical damage to company vehicles

- Medical payments and uninsured motorist protection

Contractors should also carry Hired and Non-Owned Auto (HNOA) insurance to protect against liability when employees use personal vehicles for work errands or job site travel.

Umbrella / Excess Liability Insurance

Umbrella or excess liability policies extend the limits of underlying policies — typically CGL, commercial auto, and employers' liability — when a claim exceeds those limits. While not usually legally required, many large project contracts require umbrella coverage to boost total liability limits to $5 million or more.

Key differences:

- Excess policies follow form, meaning they adopt the exact provisions and exclusions of the underlying primary policy

- Umbrella policies may offer broader coverage, including drop-down coverage for exposures not included in the primary policy, subject to a self-insured retention

In multi-party construction disputes, damages routinely climb past primary policy limits — making umbrella coverage less of an option and more of a contract reality for any significant project.

Minimum Coverage Limits: What Construction Contracts Typically Require

Coverage limits are not standardized across the industry — they vary by project type, project owner, state, and contract value. However, the most common baseline appearing in commercial construction contracts is:

- $1 million per occurrence / $2 million aggregate for CGL

- $1 million combined single limit for commercial auto liability

Understanding Liability Limit Structures

A per-occurrence limit is the maximum your insurer pays for all damages from a single event. The aggregate limit is the total maximum paid across all claims during the policy period.

Example: A contractor with a $1M/$2M policy faces a $3M claim. The insurer pays $1M (the per-occurrence limit), and the contractor is personally liable for the remaining $2M — even though the aggregate limit is $2M, because the per-occurrence limit caps the payout for this single event.

An umbrella policy layers on top of primary limits. If the contractor above carried a $5M umbrella, it would pay the additional $2M after the primary CGL limit was exhausted. That's precisely why government and institutional projects require umbrella coverage from the outset — primary CGL limits alone rarely satisfy their procurement thresholds.

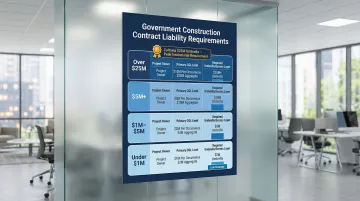

Government and Institutional Project Requirements

Government contracts and large institutional projects — hospitals and public infrastructure, for example — typically require $5M to $10M in total liability coverage. Expect contract exhibits to mandate specific endorsements, including completed operations coverage and broad form property damage.

Example government contract requirements:

| Project Owner | Project Value | Primary CGL | Umbrella/Excess |

|---|---|---|---|

| UNLV | Up to $1M | $1M/$2M | None |

| UNLV | $1M - $5M | $1M/$2M | $5M |

| UNLV | Over $5M | $1M/$2M | $10M |

| Caltrans | Over $25M | $2M/$4M | $25M |

Contractors bidding on public works must factor the cost of high umbrella and excess liability layers into their project estimates, as primary CGL limits alone will not satisfy procurement requirements.

Review Every Contract's Insurance Exhibit

Contractors should review every contract's insurance exhibit before bidding — rather than assuming standard limits apply. Undercoverage discovered mid-project can result in contract termination or direct out-of-pocket liability. Each project owner sets their own requirements, and the difference between what you carry and what a contract demands can cost you the bid — or more.

Subcontractor Insurance Requirements: What General Contractors Need to Know

General contractors are typically required — both by their own contracts and by sound risk management — to ensure every subcontractor on a project carries their own insurance. This usually includes at minimum:

- Commercial General Liability

- Workers' Compensation

- Commercial Auto

Specialty subcontractors (electricians, structural engineers) may also be required to carry professional liability.

The Mechanism: COIs and Additional Insured Endorsements

GCs typically require subs to provide a Certificate of Insurance before work begins, naming the GC and project owner as additional insureds. However, COIs alone don't prove coverage — GCs must collect physical copies of the actual policy endorsements.

Critical endorsements to require:

| Endorsement | ISO Form | Coverage Scope |

|---|---|---|

| Ongoing Operations | CG 20 10 | Liability while work is in progress |

| Completed Operations | CG 20 37 | Claims arising after work is complete |

| Primary & Noncontributory | CG 20 01 | Ensures sub's policy pays first |

The CG 20 10 endorsement only covers ongoing operations — coverage ends when the subcontractor's work is complete. The CG 20 37 endorsement is essential for long-tail construction defect claims and must be maintained through the state's statute of repose.

The 1099 Independent Contractor Question

1099 independent contractors aren't employees — but GCs routinely require them to carry their own coverage. The reason: most GC policies exclude work performed by uninsured subs, leaving a gap that falls directly on the GC.

State agencies compound this exposure by reclassifying uninsured 1099 workers as employees. Two examples illustrate how strict these standards are:

- New York's Construction Industry Fair Play Act presumes any worker providing services to a contractor is an employee unless a 12-point test is met — including holding a separate FEIN and maintaining their own liability and workers' comp coverage.

- California Labor Code Section 2750.5 creates a similar rebuttable presumption that uninsured workers are employees.

If an uninsured 1099 sub is injured on the job, the GC's workers' compensation policy absorbs the claim — and retroactive premiums follow.

Best Practice: Insurance Tracking Systems

Failing to verify subcontractor insurance exposes the GC to claims that roll up to their own policy — increasing premiums and potential liability. GCs should use a dedicated insurance tracking system that stores COIs and endorsements, flags expiring policies, and blocks sub onboarding until verification is confirmed. Embedding these requirements directly in subcontract agreements closes the gap before work ever starts.

How Much Does Commercial Construction Insurance Cost?

Construction insurance costs vary widely. Key pricing factors include:

- Business size and annual revenue or payroll

- Type of work (residential vs. commercial, new construction vs. renovation)

- Claims history and loss experience

- Location and catastrophe exposure

- Coverage limits selected

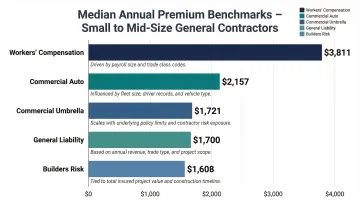

Annual Premium Benchmarks

Based on median purchasing data for small-to-medium general contractors:

| Policy Type | Average Annual Cost | Pricing Factors |

|---|---|---|

| General Liability | $1,700 | Based on $1M/$2M limits, business size, foot traffic |

| Workers' Compensation | $3,811 | Driven by payroll volume and trade class codes |

| Commercial Auto | $2,157 | Based on $1M limits, vehicle value, driver records |

| Commercial Umbrella | $1,721 | Scales based on excess coverage amount |

| Builders Risk | $1,608 | Typically 1-4% of total completed project value |

These represent median baselines. High-risk trades or contractors in catastrophe-exposed regions can pay considerably more.

Workers' Compensation Rates by Trade Class

Workers' compensation is calculated as a rate per $100 of payroll. Construction trades with higher risk classifications pay significantly more than lower-risk trades.

Using 2025/2026 Florida rate filings as a benchmark:

High-risk trades carry the steepest rates:

- Iron/Steel Erection (under 2 stories): $10.39

- Roofing - All Kinds: $6.75

Lower-risk trades fall in a tighter band:

- Plastering/Acoustical Material: $4.58

- Carpentry/Interior Trim: $4.57

- Wallboard/Drywall Installation: $4.52

- Painting: $4.48

A roofing contractor with $500,000 in annual payroll would pay approximately $33,750 in workers' comp premiums, while a painting contractor with the same payroll would pay approximately $22,400 — a difference of over $11,000 annually.

Working with a Specialized Insurance Broker

Those premium differences make broker selection matter. Working with a broker who has access to multiple carriers and real construction experience lets you compare quotes across the market in one step, rather than approaching carriers one at a time.

Soma works with hundreds of carrier partners — including Chubb, Liberty Mutual, and Markel — to place coverage for construction businesses of all sizes. Construction specialists can turn around quotes quickly, without the weeks-long delays common with generalist brokers, and can source project-specific and contractor program coverage that meets lender, owner, and contract requirements.

Frequently Asked Questions

What kind of insurance do construction companies need?

Construction companies need general liability, workers' compensation, commercial auto, and builders risk at minimum. Exact requirements depend on state law and project contract terms, with larger projects often requiring umbrella liability and specific endorsements.

What is construction general liability insurance?

Construction general liability (CGL) covers third-party bodily injury and property damage claims arising from construction operations. It is the most commonly required policy in commercial construction contracts, with typical baseline limits of $1M per occurrence / $2M aggregate.

How much does a $1,000,000 liability insurance policy cost?

Cost varies widely based on business size, trade, location, and claims history. General contractors pay an average of $1,700 annually for $1M/$2M general liability coverage, but high-risk trades like roofing or demolition pay significantly more.

What does 250/500/100 liability limit mean?

This refers to split limits on a liability policy: $250,000 per person / $500,000 per accident for bodily injury, and $100,000 for property damage. Most commercial construction contracts require higher limits than this — typically $1M per occurrence minimum.

Are 1099 contractors required to have insurance?

Most states don't legally require 1099 contractors to carry insurance — they're not employees. That said, general contractors routinely require it in their contracts, and failing to verify coverage can expose a GC to claims and retroactive workers' comp premiums.

What is the 80% rule in property insurance?

The 80% rule requires a property to be insured for at least 80% of its replacement cost to receive full claim reimbursement. For builders risk policies, coverage limits should reflect the full completed value of the project to avoid being underinsured at time of loss.