Introduction

Picture this: Your employee is making a delivery in your company van when they rear-end another vehicle at a stoplight. The damage totals $45,000—medical bills, vehicle repairs, and legal fees. You file a claim with your personal auto insurer, confident you're covered. Then comes the denial letter: "Business use is excluded under your policy." You're now personally liable for the full amount.

Most business owners assume their personal auto policy covers "work driving." It doesn't. Personal auto policies contain explicit business-use exclusions, and courts consistently uphold insurer denials for accidents during deliveries, client visits, or hauling.

This guide cuts through the confusion — who needs commercial auto insurance, what it actually covers, and how to get the right policy before a claim forces your hand.

TLDR: Key Takeaways

- Business-owned or leased vehicles require commercial auto insurance; personal policies exclude business use and will deny claims

- Commercial policies offer higher liability limits (typically $1M+) and cover all authorized drivers — not just the named insured

- Hired and Non-Owned Auto (HNOA) insurance covers liability when employees use personal vehicles for work errands

- Skipping commercial coverage risks claim denials, personal liability for damages, and regulatory penalties like fines or license suspension

- Requirements vary by state and industry — check obligations based on vehicle weight, cargo type, and how your business operates

Who Needs Commercial Auto Insurance?

Any vehicle registered under a business name or used primarily for business operations requires a commercial auto policy. Personal insurance simply won't apply in those scenarios, leaving you exposed to catastrophic out-of-pocket costs.

Your Vehicle Is Owned or Registered by the Business

If the vehicle title or registration lists your business name—LLC, corporation, or partnership—a personal auto policy will not cover it. Personal auto policies are designed exclusively for vehicles owned and registered to individuals. Insurers can and will deny claims on the grounds that a personal policy applies only to personally owned vehicles.

That denial holds up in court: the corporate structure you created to protect your personal assets becomes the very reason your personal policy won't respond.

Employees Drive for Business Purposes

Any time an employee drives a company vehicle—or uses their personal vehicle for work tasks like delivering goods, visiting job sites, or transporting clients—the business carries liability. Without a commercial policy or Hired and Non-Owned Auto (HNOA) endorsement, that liability is uninsured. If an employee causes an accident while running a work errand, the business faces direct exposure for all damages, medical bills, and legal fees.

The Vehicle Is Used to Transport Goods, Equipment, or People

Specific use cases require commercial coverage:

- Transporting products, cargo, or inventory

- Hauling tools, equipment, or materials to job sites

- Driving clients, employees, or passengers for business purposes

- Charging passengers a fare (rideshare, taxi, shuttle services)

- Towing trailers or equipment for business operations

- Operating vehicles with permanently attached equipment (cranes, lifts, plows, dump beds)

If your vehicle performs any of these functions, personal auto insurance excludes coverage by design.

Vehicle Type or Weight Exceeds Personal Policy Limits

Vehicles exceeding 10,001 pounds Gross Vehicle Weight Rating (GVWR) cannot be covered by personal auto policies. This threshold captures many standard heavy-duty pickups (Ford F-350, Ram 3500), cargo vans (Ford Transit T-250), box trucks, dump trucks, and semi-trucks.

The Federal Motor Carrier Safety Administration (FMCSA) defines any vehicle with a GVWR of 10,001 pounds or more as a Commercial Motor Vehicle (CMV), which means it falls under federal financial responsibility regulations.

Personal auto insurers like Progressive explicitly state that vehicles with a GVWR greater than 12,000 pounds are unacceptable risks for personal policies. Don't confuse the 10,001 lb insurance threshold with the 26,001 lb CDL requirement — you need commercial insurance long before you need a commercial driver's license.

Industry-Specific Triggers

Certain industries almost always need commercial auto insurance:

- Trucking and freight: Interstate carriers hauling goods

- Construction and contracting: Transporting tools, materials, and crews to job sites

- Food and beverage delivery: Restaurants, catering, meal kit services

- Healthcare: Ambulances, medical transport, home health visits

- Landscaping: Hauling mowers, equipment, and crews

- Retail delivery: E-commerce fulfillment, local delivery services

For businesses in high-complexity industries—such as hazmat transport, specialized freight, or medical transport—carriers may impose additional requirements or decline coverage altogether. Standard insurers often won't write these accounts. Soma works with hundreds of carrier partners, including specialty carriers like Chubb, Markel, and Nationwide, specifically to place coverage in situations like these.

Commercial Auto vs. Personal Auto Insurance: Key Differences

The boundary between personal and commercial auto insurance is often blurry for small business owners, especially sole proprietors and self-employed individuals who use one vehicle for both personal and work purposes. Understanding the distinctions is critical to avoiding coverage gaps.

What Personal Auto Insurance Does (and Doesn't) Cover

Personal auto policies cover the named insured and immediate family members for personal use—including commuting to and from work. They almost universally exclude business use via a specific policy exclusion clause. If an accident happens during a business errand—delivering a product, picking up supplies, visiting a client—the personal insurer can and typically will deny the claim.

Courts consistently uphold these denials. In Progressive County Mutual Insurance Co. v. Kelley, the court sided with the insurer after a policyholder was delivering pizzas at the time of the accident—a textbook business-use exclusion.

The Texas Supreme Court has consistently enforced these exclusions as clear, unambiguous contract provisions, leaving delivery drivers and business owners on the hook for all damages.

What Commercial Auto Insurance Covers Differently

Commercial auto insurance is fundamentally different in scope and structure:

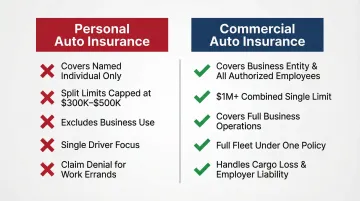

- Covers the business entity and all authorized employees with valid licenses — not just one named individual

- Provides significantly higher liability limits, typically a $1,000,000 Combined Single Limit (CSL) vs. personal policy split limits capped at $300,000–$500,000 total

- Covers an entire fleet under one policy, reducing per-vehicle costs and administrative overhead

- Handles complex legal exposure including cargo loss, employer liability for employee accidents, and client or freight broker contract requirements

When You Might Need Both

If you use one vehicle for both personal and business purposes, you may need a commercial policy for business operations and a personal auto policy for non-work use. Which policy applies depends on how the vehicle is titled and how frequently it's used for business.

Consider a sole proprietor who uses a personally-titled pickup truck mainly for commuting but occasionally hauls materials to job sites. That's a gray area — and the safest resolution is commercial auto coverage to eliminate any risk of claim denial during business use.

Hired and Non-Owned Auto (HNOA) Insurance

HNOA fills a specific and often overlooked gap: employees using their personal vehicles for work errands (making a bank run, picking up supplies, visiting clients) or the business renting or leasing vehicles. HNOA covers the business's liability in those scenarios—third-party bodily injury and property damage—but it does not cover physical damage to the employee's personal vehicle itself.

Here's how coverage splits in practice:

- HNOA covers: the business's vicarious liability if an employee causes an accident in their personal vehicle during a work errand

- HNOA does not cover: physical damage to the employee's own vehicle — that falls on their personal auto policy

What Does Commercial Auto Insurance Cover?

Commercial auto policies are modular—businesses can tailor coverage to their specific vehicles and operations. Understanding the core components helps you build the right policy.

Core Coverage Types

Liability Coverage (Bodily Injury & Property Damage): Required in most states, this covers costs if your business vehicle causes injury or property damage to a third party. It pays for medical bills, legal fees, settlements, and judgments.

State minimums can be as low as $25,000—far below the median "nuclear verdict" of $21 million in auto accident cases. Most businesses need at least $1,000,000 Combined Single Limit (CSL) to protect assets from serious litigation.

Collision Coverage: Pays to repair or replace a business vehicle damaged in an accident, regardless of fault. If your driver rear-ends another vehicle or is hit by someone else, collision coverage handles your vehicle's repair costs.

Comprehensive Coverage: Covers non-collision losses such as theft, vandalism, fire, hail, flooding, and weather events. If your cargo van is stolen or damaged in a storm, comprehensive coverage responds.

Medical Payments / Personal Injury Protection (PIP): Covers medical costs for the driver and passengers in the business vehicle after an accident, regardless of fault. PIP is mandatory in some states and provides broader benefits including lost wages and rehabilitation costs.

Uninsured/Underinsured Motorist Coverage: Protects the business if the at-fault driver has no insurance or insufficient limits. This coverage steps in so you're not left covering damages the other driver can't pay.

Beyond core coverage, several optional add-ons address industry-specific risks and asset protection gaps.

Optional and Specialty Coverages

Cargo Insurance: Protects the freight or commodities being hauled against physical loss or damage while in transit. This is separate from auto physical damage coverage, which only covers the vehicle itself. The FMCSA requires a minimum of $5,000 per vehicle in cargo insurance for household goods carriers.

Lease Gap Coverage: Covers the difference between what you owe on a leased or financed vehicle and its actual cash value if it's totaled.

Roadside Assistance & Rental Reimbursement: Roadside assistance covers towing, jump-starts, and lockouts. Rental reimbursement pays for a substitute vehicle while yours is being repaired after a covered loss—keeping operations running with minimal disruption.

Permanently Attached Equipment Coverage: Covers specialized equipment permanently installed in or on the vehicle, such as cranes, lift gates, plows, or compressors. Carriers like Progressive require this equipment to be factored into the vehicle's "stated amount" to ensure full coverage. Unattached tools and equipment require a separate inland marine policy.

What Happens If You Don't Have Commercial Auto Insurance?

Operating without commercial auto insurance exposes your business to hidden costs—financial, legal, and regulatory consequences that can cripple operations.

Insurance Claim Denial

When a business vehicle is used for work and an accident occurs, the personal auto insurer can deny the entire claim, leaving the business responsible for 100% of repair costs, medical bills, and legal fees out of pocket.

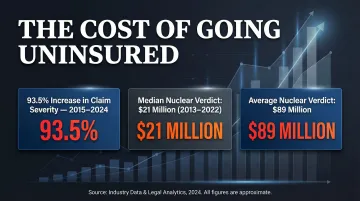

The numbers are stark: driven by social inflation, commercial auto claim severity rose 93.5% from 2015 to 2024. The median nuclear verdict for auto accidents between 2013 and 2022 was $21 million, while the average reached $89 million. Without commercial coverage, a business absorbs these judgments directly.

Personal and Business Liability Exposure

Without commercial coverage, the business owner can be held personally liable for damages. Personal assets — home, savings, retirement accounts — are all fair game in a lawsuit.

Forming an LLC or corporation doesn't protect you here. The corporate veil offers no shelter if you failed to properly insure business assets, and employee involvement adds employer liability on top of accident-related costs.

Regulatory and Legal Consequences

Most states legally require commercial auto insurance for business-owned vehicles. Operating without it can result in:

Federal Enforcement (FMCSA):

For interstate carriers, proof of financial responsibility must be electronically filed with the FMCSA. If coverage lapses, the FMCSA will immediately suspend or revoke your operating authority (MC Number), effectively shutting down your trucking business.

State-Level Penalties:

- California: Fines up to $350; suspension of vehicle registration until compliance is proven

- New York: Fines of $150 to $1,500; mandatory 30-day revocation of vehicle registration and plates

- Texas: Fines up to $1,000 for subsequent offenses; suspension of operating authority; vehicle impoundment

State DMVs and Departments of Insurance aggressively enforce commercial auto requirements. A lapse in coverage results not only in fines but in the immediate suspension of the vehicle's registration, pulling the asset off the road.

How Much Does Commercial Auto Insurance Cost?

Commercial auto insurance typically costs more than personal auto because it covers higher liability limits, more drivers, and more complex risk scenarios. The range is wide based on business specifics.

Key Pricing Factors

Several variables affect premiums:

- Industry type and risk level: Hazmat trucking costs significantly more than passenger transport

- Number of vehicles and vehicle types: Heavier vehicles cause more damage in accidents, resulting in premiums up to 363% higher than lighter vehicles

- Individual driver records and experience: Clean driving records can save 20% to 40% on premiums

- How frequently vehicles are driven and for what purpose: Long-haul interstate trucking carries higher risk than local delivery

- Coverage limits and deductibles chosen: Higher limits and lower deductibles increase premiums

- Business claims history: A history of accidents or claims drives rates up

- Geographic location: Rates can vary by 242% between states due to traffic density and litigation environments

Average Costs for $1,000,000 Liability Coverage

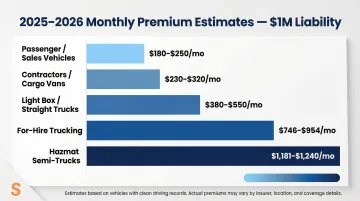

According to 2025/2026 market data, typical monthly premiums for a $1,000,000 liability limit policy include:

- Passenger / Sales Vehicles (Sedan, SUV): $180 – $250

- Contractors / Cargo Vans: $230 – $320

- Light Box / Straight Trucks: $380 – $550

- For-Hire Trucking (General Freight): $746 – $954

- Hazmat Semi-Trucks: $1,181 – $1,240

(Estimates based on businesses with clean driving records; actual premiums vary based on location and claims history.)

Commercial auto premiums increased by an average of 6.6% in Q4 2025 — the 58th consecutive quarter of rate increases. The good news: several proven strategies can meaningfully reduce what you pay.

How to Manage Costs Without Sacrificing Coverage

Invest in driver safety programs. Carriers reward businesses with formal training and safety protocols. Documented programs signal lower risk and often qualify for dedicated discounts at renewal.

Screen drivers and enforce safe driving policies. Clean records reduce premiums by 20% to 40%. Regular MVR checks and clear disciplinary policies keep your fleet's risk profile in check.

Bundle commercial auto with other business policies. Pairing commercial auto with a commercial property policy or Business Owner's Policy (BOP) typically yields multi-policy discounts. Progressive advertises an average savings of 12% on bundled auto policies.

Enroll in a telematics program. Carrier-sponsored programs tie premiums to actual driving behavior:

- Travelers' IntelliDrive offers up to 35% savings at renewal for safe driving

- Progressive's Snapshot ProView gives an automatic 5% discount for enrolling, with 8%–20% savings at renewal based on fleet habits

Compare rates across multiple carriers. A single quote rarely reflects the best available price. Soma's brokerage model lets businesses submit one application and receive quotes from hundreds of carrier partners — no waiting weeks or chasing multiple brokers.

How to Get Commercial Auto Insurance

Securing commercial auto insurance is faster and easier when you're prepared. Here's what you need and how to streamline the process.

What to Prepare Before Applying

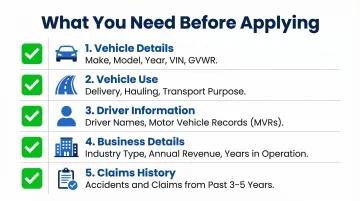

Gather the following information to speed up the quoting process:

- Vehicle details: Make, model, year, VIN, and GVWR for each vehicle

- Vehicle use: How each vehicle is used (delivery, hauling, client transport, etc.)

- Driver information: Names and driving records (MVRs) of all employees who will drive

- Business details: Business type, industry, annual revenue, and years in operation

- Claims history: Any existing claims or accidents in the past 3-5 years

Having this information ready allows brokers to generate accurate quotes quickly, often within 24-48 hours.

Navigating Complex or Hard-to-Place Accounts

Businesses in trucking, construction, healthcare transport, and manufacturing often struggle to get coverage through standard carriers. These specialty risks require carriers with specific appetite and underwriting expertise:

- New trucking ventures with limited operating history

- Drivers with prior violations on record

- Hazmat haulers requiring specialized liability limits

- Medical transport fleets with unique liability exposure

Soma's brokerage model addresses this challenge. Businesses submit one application and receive quotes from hundreds of carrier partners, including specialty carriers like Chubb, Markel, and Nationwide. This eliminates the need to wait weeks or chase multiple brokers, and it ensures access to carriers willing to write coverage that others decline. Most hard-to-place accounts receive quotes within 24-48 hours.

Frequently Asked Questions

Do I really need commercial auto insurance?

If your business owns vehicles, employees drive for work, or vehicles transport goods or people, you almost certainly need it. Most states legally require commercial auto insurance for business-owned vehicles, and personal policies exclude business use by design.

What's the difference between commercial and personal auto insurance?

Personal auto covers the named individual for personal use only. Commercial auto covers the business entity, all authorized employee drivers, and business-related operations—with liability limits that typically run much higher: $1M or more, compared to the $300K–$500K ceiling on most personal policies.

Can I use personal insurance on a business vehicle?

No. Claims from work-related driving are routinely denied under personal policies, leaving your business financially exposed. If the vehicle is titled to a business entity, personal insurance is simply ineligible from the start.

Is it cheaper to insure a car through an LLC?

Insuring through an LLC generally requires a commercial auto policy, which is more expensive than personal insurance. However, it separates business liability from personal assets—a critical risk management benefit worth the additional cost.

What happens if you don't have commercial insurance?

Expect three outcomes if a claim arises without the right coverage:

- Personal insurer denies the claim outright

- Business and personal assets become exposed to damages and legal fees

- Regulatory penalties can include fines, license suspension, or loss of operating authority

How much does a $1,000,000 liability insurance policy cost?

Cost depends on industry, vehicle type, number of drivers, and claims history. For standard cargo vans, expect $230 to $320 per month. For-hire trucking averages $746 to $954 per month, while hazmat semi-trucks range from $1,181 to $1,240 per month. Higher-risk industries pay significantly more than lower-risk businesses.