Introduction

Picture this: You've just wrapped up a consulting project when your client calls—someone was injured on a job site you worked, or a software bug you missed crashed their e-commerce store during Black Friday. Now they're threatening a lawsuit, and there's no employer standing behind you—your personal assets are exposed.

Unlike W-2 employees, independent contractors operate as separate legal entities. When something goes wrong, you're personally responsible for the financial fallout. Liability insurance is among the most important financial decisions you'll make as a self-employed worker.

This guide covers what independent contractor liability insurance is, what types exist, who needs them, how much they cost, and how to get the right coverage fast.

Key Takeaways

- You're personally liable for lawsuits, injuries, and property damage arising from your work

- General liability covers physical risks; professional liability covers service errors and financial losses

- Proof of insurance is required by most clients — and legally mandated in several states

- Costs typically run $500–$2,000/year depending on your trade, with short-term per-project policies also available

- A good broker gets you quotes from multiple carriers in one shot — no chasing, no delays

What Is Independent Contractor Liability Insurance?

Independent contractor liability insurance isn't a single policy—it's a catch-all term for several types of business insurance that protect 1099 workers from financial and legal exposure related to their work.

As an independent contractor, you're legally separate from the businesses that hire you. If a lawsuit arises from your work, the hiring company expects you to be responsible, not them. Many client contracts explicitly name contractors as the liable party for any claims stemming from the contractor's actions or negligence.

Understanding "Additional Insured" Requirements:

You'll frequently encounter requests to add clients as "additional insureds" on your policy. This means your insurance pays out first if both you and your client are named in a lawsuit related to your work.

It's a standard requirement across construction, consulting, and professional services—and a non-negotiable condition in many client contracts.

Do Independent Contractors Need Liability Insurance?

Yes. Most independent contractors need at least general liability insurance, and many need additional coverage depending on their trade.

In practice, it's often a business requirement. Up to 90% of businesses require a Certificate of Insurance (COI) from service providers before hiring. Some states go further, legally mandating liability insurance for certain professions:

- California: Contractors must carry minimum $1 million liability coverage

- Florida: General contractors need $300,000 liability and $50,000 property damage coverage

- Washington: General contractors must maintain $200,000 public liability and $50,000 property damage

The Real Cost of Being Uninsured

Without insurance, you're personally responsible for:

- Legal defense fees (often 40% of total claim costs)

- Lawsuit settlements and judgments

- Third-party medical bills

- Property repair or replacement costs

The average small business liability claim now costs $97,200, with costs increasing 18% since 2022. A single claim could wipe out years of earnings.

Insurance Reinforces Your Independent Status

Carrying your own business insurance demonstrates you operate as a legitimate independent business entity. This matters during IRS or Department of Labor audits. Both agencies consider whether a worker maintains their own insurance when evaluating independent contractor status — it's one of the clearest signals you're running a real business, not functioning as a de facto employee.

Types of Insurance Independent Contractors Need

The right combination of policies depends on your work type, industry, and client requirements. Here are the most important coverage types.

General Liability Insurance

General liability (GL) insurance is the foundational coverage for independent contractors. It protects against third-party claims of:

- Bodily injury (a client trips over your equipment at their office)

- Property damage (you accidentally damage a client's flooring during installation)

- Advertising injury (claims of libel, slander, or copyright infringement)

Real-world example: A plumber accidentally causes water damage to a client's home while repairing a pipe. GL covers the repair costs and any resulting lawsuit.

What GL Does NOT Cover:

- Your own injuries or medical expenses

- Intentional damage you cause

- Your own tools, equipment, or property

- Professional errors, faulty workmanship, or missed deadlines

- Claims exceeding your policy limits

Professional Liability Insurance (E&O)

Professional liability insurance—also called errors and omissions (E&O) insurance—covers contractors who provide advice, consulting, or skilled professional services. It protects against claims of:

- Negligence or professional mistakes

- Missed deadlines that cause client financial harm

- Incomplete work or service errors

- Failure to deliver promised results

Who specifically needs this:

- Accountants and CPAs

- IT consultants and software developers

- Financial advisors and investment professionals

- Designers, architects, and engineers

- Marketing consultants and agencies

- Any contractor whose mistake can cause financial loss, not just physical harm

Some states legally require E&O coverage. For example, Massachusetts requires home inspectors to carry minimum $250,000 E&O coverage, while Pennsylvania mandates $100,000 per occurrence and $500,000 aggregate.

Other Coverage Types to Consider

Occupational Accident Insurance (OAI): Most independent contractors don't qualify for workers' compensation, so OAI fills that gap. It typically costs 30–50% less than workers' comp and covers:

- Medical expenses from on-the-job injuries

- Disability payments and lost income during recovery

- Death and dismemberment benefits

Additional Policies Based on Work Type:

- Commercial Auto Insurance: Required if you drive for work (not just commuting)

- Commercial Property Insurance: Covers your tools, equipment, and business property

- Cyber Liability Insurance: Essential for contractors handling client data, covering breach costs and legal liability

- Business Owner's Policy (BOP): Bundles GL with property coverage, typically saving 10–25% compared to separate policies

How Much Does Independent Contractor Liability Insurance Cost?

What you pay depends on your industry, coverage limits, location, experience, and claims history. Here's a realistic breakdown of what most independent contractors can expect to spend.

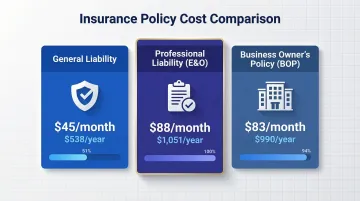

Average Monthly Costs by Policy Type:

| Policy Type | Average Monthly Cost | Average Annual Cost |

|---|---|---|

| General Liability | $45 | $538 |

| Professional Liability (E&O) | $88 | $1,051 |

| Business Owner's Policy (BOP) | $83 | $990 |

Industry-Specific Cost Variations:

High-risk industries pay more than low-risk ones:

- Construction/Trades: $82-$256/month for GL

- IT/Technology: $30/month for GL

- Consulting: $29/month for GL

- Healthcare: $31/month for GL

Several factors push premiums up or down beyond the industry baseline:

- Construction, electrical, and HVAC contractors pay more than freelance writers or graphic designers

- Jumping from $1M to $2M per-occurrence limits costs as little as $1/month more

- Prior claims on your record will raise your rates noticeably

- Higher revenue and payroll typically push premiums higher across most policy types

Flexible Coverage Options:

- Pay-as-you-go plans tie premiums to actual payroll or project activity — a practical fit for variable income

- Per-project policies offer short-term coverage (monthly or per-gig) if you don't work year-round

- Bundling GL and property coverage into a BOP typically saves 10-25% versus buying each policy separately

How to Get Independent Contractor Liability Insurance

What You'll Need Before Getting a Quote:

- Business type and specific industry

- Annual revenue or payroll figures

- Description of services you perform

- Desired coverage limits

- Any client-mandated requirements (additional insured requests, minimum limits)

Understanding the Certificate of Insurance (COI):

The COI is your proof of coverage—a one-page document summarizing your policy numbers, limits, and effective dates. You'll provide this to clients before starting work. Digital insurers can generate COIs instantly, while traditional carriers may take days. Having a COI ready is increasingly expected in professional contracting relationships.

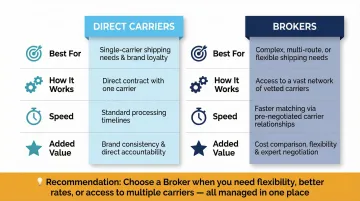

Direct Carriers vs. Brokers:

| Direct Carriers | Brokers | |

|---|---|---|

| Best for | Standard, low-risk contractors | Complex, high-risk, or hard-to-insure profiles |

| How it works | Buy directly online | Single application, multiple carrier quotes |

| Speed | Fast for simple coverage | Varies; specialized brokers can be just as fast |

| Added value | Straightforward purchasing | Risk management expertise, market negotiation |

For contractors in industries like construction, healthcare, or technology, a specialized broker typically delivers better coverage at a more competitive price than going direct.

Soma works with hundreds of carriers—including Chubb, Markel, Liberty Mutual, and Nationwide—to place coverage for independent contractors across complex industries. One application gets you quotes across multiple markets, with an expert risk management team that matches coverage to your specific operations.

Frequently Asked Questions

How much does independent contractor liability insurance cost?

Costs vary by industry and risk level. General liability averages $45/month ($538/year), while professional liability averages $88/month ($1,051/year). Per-project or pay-as-you-go options may cost less for part-time contractors.

How do I protect myself as a 1099 contractor?

Carry general liability at minimum, add professional liability if providing services or advice, maintain a current certificate of insurance, and review coverage whenever taking on higher-risk projects or new clients.

Do independent contractors need liability insurance?

Yes, most contractors need it. Clients and some states require it, and contractors are personally liable for lawsuits, property damage, and injury claims without an employer to absorb the loss.

What insurance does an independent contractor need?

Core types include general liability (most common), professional liability (for service-based work), and optionally OAI, commercial auto, or a BOP—depending on your industry .

Can independent contractors get commercial general liability insurance?

Yes, independent contractors can and should get commercial general liability insurance. It's widely available through brokers and standard carriers for self-employed workers.

Should independent contractors purchase blanket liability insurance?

"Blanket liability" isn't a standard product name. Contractors needing broad coverage across multiple clients or projects may benefit from a commercial umbrella policy or a flexible GL policy with high limits—a broker can help match the right structure to your workload.