Introduction

Pick the wrong policy and you're either paying for coverage you don't need or exposed to losses you thought were covered. For most small business owners, the choice comes down to general liability insurance versus a business owner's policy — and the distinction matters.

The wrong call could leave a business unprotected against property damage, lawsuits, or income disruption.

Below, you'll find what each policy actually includes, how they stack up against each other, and which one fits your business type.

Key Takeaways

- General liability (GL) covers third-party claims like bodily injury, property damage, and advertising injury — not your own business assets

- A BOP bundles general liability with commercial property and business interruption coverage into one package, usually at a lower combined cost

- A BOP always includes GL, so buying both is never necessary

- BOPs are designed for small, low-risk businesses; high-risk or larger operations may need to buy GL and property coverage separately

- No physical assets? GL alone may be enough. Equipment, inventory, or a lease? A BOP typically delivers better value

BOP vs. General Liability Insurance: Quick Comparison

Here's how the two policies stack up across four key dimensions.

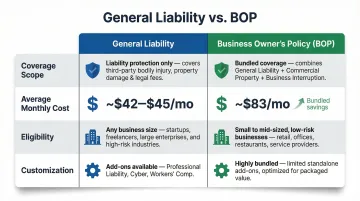

| General Liability | BOP | |

|---|---|---|

| Coverage | Third-party injury, property damage, advertising injury | Everything GL covers, plus your own property and lost income |

| Avg. Monthly Cost | ~$42–$45/month | ~$83/month |

| Eligibility | Any business, any size or risk level | Small businesses: ≤100 employees, ≤$5M revenue, low-risk industries |

| Customization | Product liability, liquor liability, targeted add-ons | GL add-ons plus professional liability, cyber, EPLI, equipment breakdown |

Coverage Scope

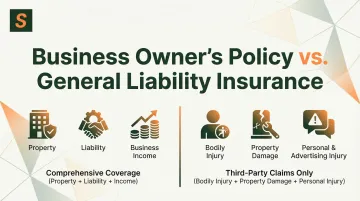

General Liability: Covers third-party bodily injury, property damage, and advertising/personal injury claims only. If a customer slips in your store or your team damages a client's equipment, GL responds. It does not protect your own business property.

BOP: Covers everything GL covers, plus damage to your own business property and lost income from covered disruptions. If fire destroys your inventory or forces you to close temporarily, a BOP replaces both the property and the revenue.

Cost

General Liability: Small businesses pay an average of $45 per month or $538 per year for standalone GL policies, according to 2026 data from Insureon. Forbes Advisor reports similar figures at $42 per month or $504 per year.

BOP: The average cost of a BOP is $83 per month or $990 annually, per Insureon. Customers automatically save up to 10% when choosing a BOP rather than purchasing GL and commercial property insurance separately, according to NEXT Insurance.

Eligibility

General Liability: Available to nearly any business, regardless of size, industry, or risk level. Even high-risk operations can secure GL coverage.

BOP: Restricted to small, low-risk businesses. Companies with 100 or fewer employees and revenues up to $5 million are typically eligible, per the Insurance Information Institute. Businesses in construction, manufacturing, or other high-risk industries often don't qualify and must purchase GL and property separately.

Customization

General Liability: Can be endorsed with product liability, liquor liability, and other add-ons tailored to specific exposures.

BOP: Supports a wider range of endorsements: professional liability, data breach coverage, employment practices liability, and equipment breakdown. Consolidating these under one policy also cuts down on administrative overhead.

What is General Liability Insurance?

General liability insurance is a standalone policy that protects businesses against financial losses from third-party claims—meaning claims from anyone who doesn't work for the business. According to the Insurance Information Institute, a Commercial General Liability (CGL) policy covers three core areas:

- Bodily Injury and Property Damage Liability - A customer slipping and falling in your store, or an employee damaging a client's equipment on-site

- Personal and Advertising Injury - Copyright infringement in marketing materials, libel, slander, or reputational harm from a public statement

- Medical Payments - Immediate medical expenses for minor injuries, regardless of fault

GL does not cover damage to the business's own property, equipment, or inventory, nor does it replace lost business income if operations are halted. Coverage applies to third-party claims, not losses the business suffers directly.

GL is typically the right fit for freelancers, independent contractors, home-based businesses, and service providers that don't rely on significant physical assets. For businesses that don't qualify for a Business Owner's Policy (BOP) due to industry risk profile, GL coverage is often the primary option available.

Use Cases of General Liability

GL handles claims such as:

- A retail customer injured by a falling display

- A consultant whose advertised claim triggers a lawsuit

- A landscaper whose crew damages a client's fence during a job

Beyond those scenarios, GL also satisfies contractual and legal requirements. Many client contracts, commercial leases, and state business licenses require proof of GL coverage. Insureon notes that "general liability insurance is by far the most common insurance coverage required in a commercial lease. It's also frequently required by mortgage lenders and in client contracts."

What is a Business Owner's Policy (BOP)?

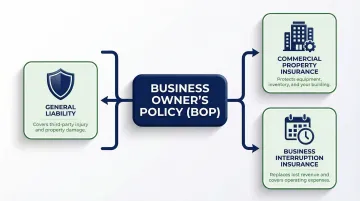

A BOP is a bundled insurance package that combines general liability, commercial property insurance, and business interruption coverage into one policy—usually at a lower combined cost than buying each separately. The Insurance Information Institute confirms that a BOP combines three core coverages:

- General Liability - Covering the same third-party claims as a standalone GL policy

- Commercial Property Insurance - Covering the business's owned or leased physical assets—equipment, inventory, furniture, and the building itself—against events like fire, theft, and vandalism

- Business Interruption Insurance - Replacing lost revenue and covering operating expenses if the business has to shut down temporarily after a covered loss

Businesses with more complex exposures can expand a BOP with optional add-ons:

- Professional liability

- Cyber/data breach coverage

- Employment practices liability

- Equipment breakdown coverage

Not every business qualifies. ISO/Verisk guidelines cap eligibility at 35,000 square feet of floor area and $6,000,000 in annual gross sales per location. High-risk industries — construction, trucking, and certain manufacturing — typically fall outside BOP eligibility and must purchase GL and property coverage separately.

Use Cases of a Business Owner's Policy

The typical BOP buyer includes:

- A retail shop with inventory and storefront property

- A restaurant with kitchen equipment and dining furniture

- A medical office with specialized equipment and patient records

- A consulting firm operating from leased office space

- A tech company with servers, computers, and office assets

For businesses signing commercial leases, a BOP is often the most efficient path to meeting lease requirements: it satisfies the landlord's property coverage demands and the liability requirement in a single policy.

BOP vs. General Liability Insurance: Which One is Right for Your Business?

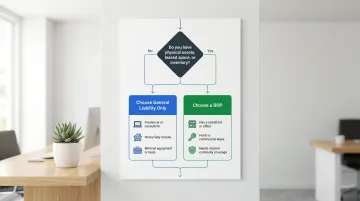

The core decision comes down to whether the business has physical assets to protect. If a business has no owned or leased property, equipment, or inventory that would cause serious financial harm if lost, GL alone may be enough. If property and income continuity matter, a BOP usually wins on both coverage breadth and cost efficiency.

Decision Framework

Choose GL only if:

- You're a freelancer, home-based professional, or independent contractor with no physical business assets

- You operate entirely remotely with no leased space

- Your business has minimal equipment or inventory exposure

Choose a BOP if:

- You operate from a storefront, office, or any space where equipment, inventory, or leased property is at risk

- You have a commercial lease requiring property coverage

- You need business interruption protection to replace lost income during recovery from a covered event

The Coverage Gap Risk

When a business with only GL experiences a fire, flood, or break-in, GL would cover claims against the business — but not the loss of its own equipment or the revenue lost during downtime. According to FEMA and Congressional Research Service data, 40% of businesses do not reopen after a disaster, and another 25% close a year after the disaster.

Hiscox's 2025 underinsurance report found that 77% of US small businesses are underinsured. Separately, 74% misunderstand GL coverage, falsely expecting it to cover property damage from fire or flood — protection that requires a BOP or standalone commercial property policy.

When to Go Beyond a BOP

High-risk or complex businesses — such as contractors, manufacturers, trucking companies, or healthcare providers — may not qualify for a BOP and will need a tailored combination of standalone GL, commercial property, and other specialty policies. That's where a specialist brokerage matters. Soma has placed coverage for thousands of complex businesses, matching each one with the right combination of policies across hundreds of carriers — no chasing multiple brokers required.

Important: Owning an LLC or other entity structure does not replace the need for insurance. The SBA notes that "a limited liability company (LLC) or a corporation status can protect your personal property from lawsuits. However, that protection has limits. Unexpected catastrophe? Business insurance can fill in any gaps in coverage."

Conclusion

GL is the right entry point for businesses with limited physical exposure. A BOP is the stronger choice for businesses carrying property, inventory, or lease obligations — and since a BOP already includes GL coverage, buying both is never necessary.

Your final decision comes down to three factors:

- Business size — smaller operations often start with GL; growing businesses typically need a BOP

- Industry — property-heavy sectors (retail, hospitality, light manufacturing) benefit most from bundled coverage

- Risk profile — the more physical assets and lease obligations you carry, the more a BOP earns its cost

If your business is complex or harder to place, Soma works with hundreds of carriers to find the right fit fast — no weeks of waiting, no chasing multiple brokers for quotes.

Frequently Asked Questions

What is the difference between a business owner's policy (BOP) and general liability insurance?

GL covers only third-party liability claims, while a BOP bundles GL with commercial property and business interruption coverage into one, typically more affordable policy.

Does a business owner's policy include general liability coverage?

Yes, GL is a component of every BOP—so businesses that buy a BOP do not need to purchase separate GL insurance.

What is not covered under a business owner's policy?

BOPs typically exclude workers' compensation, commercial auto, and professional liability (unless endorsed). High-risk industries may also be ineligible and require separate policies.

What are the advantages of a business owner's policy (BOP)?

BOPs offer bundled savings, simplified management under a single policy, and built-in protection for both liability and physical business assets.

Do I need general liability insurance if I have an LLC or a small business?

An LLC provides legal separation but not financial protection against lawsuits or property loss—GL or a BOP is still necessary to cover claims against the business.

What counts as proof of general liability insurance or a business owner's policy?

Your insurer or broker issues a Certificate of Insurance (COI)—the standard proof document required by clients, landlords, and licensing bodies.