Introduction

A roofing contractor accidentally damages a client's HVAC unit while replacing shingles. An electrician's apprentice leaves equipment in a hallway, causing a homeowner to trip and break an ankle. A plumber's work passes inspection, but six months later a faulty connection floods the client's basement, destroying $40,000 in finished living space. Without insurance, these scenarios end in lawsuits, liens, and financial ruin. The average federal jury verdict in liability cases hit $16.2 million in 2024, and even smaller claims routinely top $50,000 in legal fees alone.

This article explains what contractor general liability insurance covers, what it excludes, who needs it, and what it costs—so you can choose the right coverage before a job site incident forces the decision for you.

Key Takeaways

- Covers third-party bodily injury, property damage, and legal defense costs

- Excludes employee injuries, your own tools, and professional design errors

- Most clients, contracts, and state licensing boards require it before work starts

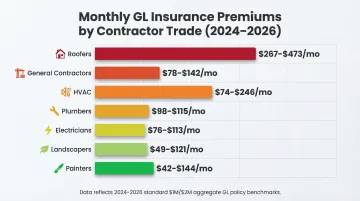

- Costs vary widely by trade—roofers pay $267–$473/month, painters pay $42–$144/month

- Solo contractors and single-crew operators need it just as much as large firms

What Is Contractor General Liability Insurance?

Contractor general liability (GL) insurance is a commercial policy that protects contracting businesses from financial losses when their work causes bodily injury, property damage, or related harm to a third party. The term "contractor liability insurance" isn't a separate product category — it's standard commercial general liability (CGL) coverage applied to contracting work.

Most contractor GL policies are written using the ISO CG 00 01 coverage form, the industry-standard template. These policies operate on an "occurrence" basis, meaning they cover incidents that happen during the policy period — regardless of when the claim is filed.

That distinction matters. If you install a deck in 2024 and it collapses in 2027, your 2024 policy responds to the claim. Construction defects routinely surface years after project completion, so occurrence-based coverage is essential.

How GL Differs from Other Policies

Contractors often confuse GL with other commercial coverages. Here's what each protects:

| Policy Type | What It Covers | What GL Cannot Replace |

|---|---|---|

| General Liability (GL) | Third-party bodily injury and property damage | Employee injuries, professional errors, your own property |

| Workers' Compensation | Employee injuries and medical expenses on the job | Third-party claims and property damage |

| Professional Liability (E&O) | Financial losses from design errors or bad advice | Physical injury or property damage |

| Business Owner's Policy (BOP) | Bundles GL with property insurance for your building/contents | Standalone GL doesn't cover your own assets |

GL covers third-party claims — employees, professional errors, and your own equipment each require separate policies.

Who Needs Contractor General Liability Insurance?

Trades That Require GL Coverage

General liability insurance isn't just for large general contracting firms. The following trades all face third-party liability exposure on every job:

- General contractors and subcontractors

- Roofers, electricians, plumbers, HVAC technicians

- Painters, carpenters, masons, drywall installers

- Landscapers, concrete contractors, welders, paving contractors

- Home inspectors and specialty trades

Contractual and Legal Requirements

Most clients, property owners, government agencies, and general contractors contractually require proof of GL insurance via a Certificate of Insurance (COI) before allowing a contractor on-site. Some states and licensing bodies mandate it as well:

- Florida: General contractors must carry $300,000 liability / $50,000 property damage; specialty contractors need $100,000 / $25,000

- Texas: Electricians must prove $300,000 per occurrence / $600,000 aggregate

- California: LLCs must carry liability insurance, and home improvement contractors must disclose coverage status to homeowners

- New York City: Department of Buildings requires $5–$25 million in GL coverage depending on building height and project scope

Why Sole Proprietors and Independent Contractors Need It

Even one-person operations face real liability exposure. If you work on client property, interact with third parties, or risk accidental damage during a job, you need GL coverage. That applies whether you're a solo carpenter or a growing subcontracting crew.

Finding the right policy isn't always straightforward — especially for trades that carriers consider higher risk. Soma works with contractors across all trades, including complex and hard-to-insure operations, placing coverage through partners like Chubb, Liberty Mutual, Kinsale, and hundreds of other insurers.

What Does Contractor General Liability Insurance Cover?

Contractor GL policies cover the core liability risks that come with active job sites: injuries, property damage, and claims that surface long after a project wraps up. Here's what each coverage component actually does.

Bodily Injury

Bodily injury coverage pays medical costs, hospital bills, and related expenses if a third party—such as a client, visitor, or bystander—is injured as a result of your work or operations.

Example: A homeowner trips over your equipment left on-site and breaks their wrist. Your GL policy covers their medical bills and any resulting lawsuit.

Property Damage

Property damage coverage pays for repair or replacement of a third party's property accidentally damaged during your work.

Example: Your crew accidentally damages a client's hardwood flooring during a renovation. The policy covers repair costs and legal defense if the client sues.

Personal and Advertising Injury

GL policies cover claims of:

- Libel, slander, or reputational harm

- Copyright infringement in advertisements

- False arrest or malicious prosecution

Example: If you or an employee makes damaging comments about a competitor on social media, this coverage responds to defamation claims.

Products and Completed Operations

This coverage extends protection beyond the active job period. If a completed project later causes injury or damage, this portion of the policy responds.

Example: Faulty wiring you installed causes a fire six months after job completion. Completed operations coverage pays for property damage and any resulting bodily injury claims. Most states allow injury claims up to 3 years after an incident — and construction defect claims can run longer — so this coverage continues working well past your final invoice.

Legal Defense Costs

GL policies pay for attorney fees, court costs, and settlements or judgments even if you're not ultimately found liable. Under standard ISO policy terms, defense costs are paid as "Supplementary Payments" outside the policy limits, meaning legal bills don't erode your coverage capacity.

Even a frivolous lawsuit can run $50,000–$150,000 in defense fees before reaching trial. Without this coverage, you'd pay those costs out of pocket — regardless of the outcome.

What's Excluded from Contractor General Liability Insurance?

GL coverage has clear boundaries. Knowing where it stops — and which policy picks up from there — prevents costly surprises when a claim hits.

Here's a quick breakdown of what GL won't cover and what fills each gap:

- Employee injuries → Workers' compensation

- Your own tools and equipment → Inland marine / equipment floater or BOP

- Faulty workmanship or professional errors → Errors & omissions (E&O)

- Pollution and environmental damage → Contractors pollution liability (CPL)

- Intentional acts → Not insurable; excluded outright

- Cyber incidents → Cyber liability policy

Employee Injuries (Workers' Compensation)

Injuries sustained by your own employees are explicitly excluded from GL coverage. These are handled by workers' compensation insurance, which is typically required by law once you have employees.

Contractor's Own Tools and Equipment

GL only covers damage to third-party property. Your own tools, equipment, and materials are not covered. A tools and equipment floater (inland marine coverage) or a Business Owner's Policy (BOP) with equipment coverage fills this gap.

Professional Errors and Faulty Workmanship (E&O)

Negligent design, bad advice, or work that simply doesn't meet the expected standard—without causing physical injury or property damage—is not covered under GL. Errors and omissions (E&O) or professional liability insurance addresses this type of claim.

Example: You design a drainage system that doesn't work properly. If there's no physical damage, just a system that underperforms, GL won't respond. You need E&O coverage.

Pollution and Environmental Damage

If your work results in a chemical spill, contamination, or other environmental harm, GL will not respond. Contractors handling hazardous materials or working in environmentally sensitive settings should consider contractors pollution liability (CPL) coverage.

Intentional Acts

Intentional damage is excluded from GL coverage — no policy covers deliberate harm. If a contractor willfully damages a client's property, there's no coverage backstop.

Cyber Liability

Cyber-related incidents — such as a data breach from contractor access to a client's systems — aren't covered under GL. As job sites rely more on connected devices and digital project management, this exposure is growing fast. A standalone cyber liability policy closes the gap.

How Much Does Contractor General Liability Insurance Cost?

The cost of a standard $1 million per occurrence / $2 million aggregate GL policy varies widely based on inherent trade risk.

Premium Benchmarks by Trade (2024–2026)

High-risk trades working at heights or with hazardous materials pay notably more than ground-level artisan contractors:

| Trade | Monthly Premium | Annual Premium | Key Risk Drivers |

|---|---|---|---|

| Roofers | $267–$473 | $3,200–$5,676 | Height risks, severe fall hazards, weather exposure |

| General Contractors | $78–$142 | $936–$1,700 | Job site injuries, property damage, subcontractor oversight |

| HVAC | $74–$246 | $888–$2,956 | Refrigerant handling, property damage potential |

| Plumbers | $98–$115 | $1,176–$1,378 | Water damage potential, pipe bursts |

| Electricians | $76–$113 | $912–$1,353 | Fire hazards, shock risks |

| Landscapers | $49–$121 | $588–$1,453 | Equipment operation, lower injury risk |

| Painters | $42–$144 | $504–$1,733 | Relatively lower risk, minimal heavy equipment |

Factors That Influence Premiums

Four variables move the needle most:

- Trade risk: Fall-heavy trades like roofing cost more than ground-level work — the premium table above reflects this spread directly.

- Payroll size: Insurers use payroll as the primary rating base, so larger crews mean higher premiums.

- Location: California premiums run 54% higher than the national average; West Virginia is 29% lower — local medical costs and legal environments drive the gap.

- Claims history: Multiple claims or construction defect litigation trigger steep rate hikes or non-renewals. A clean record is one of the most reliable ways to keep costs down.

Policy Structure Decisions

Two structural levers directly affect what you pay:

- Higher coverage limits increase premiums but protect against catastrophic claims that exhaust lower thresholds.

- Higher deductibles (e.g., $1,000 instead of $500) shift initial risk to you but can cut annual premiums by 10–15%.

Beyond structure, maintaining clean job site logs and investing in employee safety training reduces claim frequency — which pays off at renewal. Brokerages like Soma, with access to carriers including Chubb, Markel, Liberty Mutual, and Kinsale, let contractors compare rates across the market with a single application rather than approaching insurers one by one.

Frequently Asked Questions

How much is a $1,000,000 general liability policy?

For contractors, the average cost is $82–$113 per month ($981–$1,351 annually) for a $1M per occurrence / $2M aggregate policy. Costs vary widely by trade type, location, and business size—high-risk trades like roofing pay significantly more than lower-risk trades like painting.

What does general liability cover in construction?

In construction, GL covers third-party bodily injury, property damage, completed operations (defects that surface after job completion), and legal defense costs. It protects against jobsite accidents and post-project claims but excludes employee injuries and damage to your own tools.

What is excluded from a commercial general liability policy?

The main exclusions are employee injuries (need Workers' Comp), damage to your own property (need Inland Marine), professional errors (need E&O), intentional acts, pollution (need CPL), and cyber incidents (need Cyber Liability).

What is the difference between contractors liability and general liability?

There is no difference. "Contractors liability insurance" is simply what the industry calls a commercial general liability policy when sold to contracting businesses — the coverage, structure, and exclusions are identical.

Does commercial general liability insurance cover independent contractors?

Not automatically. A general contractor's GL policy does not extend to subcontractors unless they are added as Additional Insureds. That's why most contracts require independent contractors to carry their own GL coverage rather than relying on the GC's policy.

How do I know if I need general liability insurance?

If you work on client property, interact with third parties, or could cause accidental damage or injury on the job, you need GL insurance. Most clients and contracts require proof of coverage before work begins, so it's both a practical necessity and a standard contract requirement.