Introduction

Picture this: a customer slips on a wet floor in your retail store and suffers a broken wrist. An employee accidentally damages a client's expensive equipment during a service call. A competitor claims your latest social media ad infringes on their trademark. Without proper coverage, any one of these scenarios could trigger legal bills and settlement costs that devastate your business.

The financial stakes are real. According to an Insurance Journal report on The Hartford's analysis of over one million small business policies, the average slip-and-fall or customer injury claim now costs $45,000. Small businesses face roughly 12 million lawsuits annually in the U.S. They generate only 20% of commercial revenue yet bear 48% of commercial tort costs — approximately $160 billion.

Commercial General Liability (CGL) insurance protects businesses from these third-party risks. This guide explains what CGL covers, what it excludes, who needs it, how much it costs, and how to buy the right policy for your business.

Key Takeaways

- CGL covers bodily injury, property damage, personal/advertising injury, and no-fault medical payments to third parties

- Professional errors, employee injuries, cyber incidents, pollution, and vehicle damage require separate policies

- Businesses with physical premises, customer interactions, or off-site operations typically need CGL

- Annual premiums for a $1M policy range from $300 to $1,000 for most small businesses

- Occurrence policies cover incidents during the policy period; claims-made policies cover claims filed while the policy is active

What Is Commercial General Liability (CGL) Insurance?

Commercial General Liability insurance is a standardized policy form introduced by the Insurance Services Office (ISO) in 1986 to protect businesses against third-party claims for bodily injury, property damage, and personal or advertising injury. The policy covers incidents arising from business premises, operations, products, and completed work.

One important boundary: CGL covers accidental harm to customers, vendors, or the public — not mistakes made while delivering professional services like consulting, accounting, or legal advice. That gap is addressed by separate professional liability (E&O) coverage.

CGL policies provide two essential protections:

- Duty to defend: The insurer pays legal fees and court costs, regardless of fault

- Duty to indemnify: The insurer pays settlements or judgments up to the policy limit

Both protections matter. Defense costs alone routinely reach $50,000–$100,000 before a case ever reaches settlement — the policy covers that exposure whether or not a judgment follows.

What Does CGL Insurance Cover? The Three Core Coverages

A standard CGL policy divides protection into three coverage sections (A, B, and C), each addressing distinct liability risks. Understanding what each section covers — and how they interact — helps you know exactly where your protection begins and ends.

Coverage A: Bodily Injury and Property Damage

Coverage A protects your business when someone is physically harmed or their property is damaged due to your operations. This includes:

Premises liability examples:

- A customer slips on a freshly cleaned floor in your store and breaks an ankle

- A visitor trips over loose carpeting in your office lobby

- A patron is injured by falling merchandise in your warehouse

Operations liability examples:

- Your employee accidentally breaks a water pipe while installing equipment at a client's location

- A contractor damages a homeowner's hardwood floors during a renovation project

- Your delivery driver drops a package, damaging a customer's front steps

Coverage A extends beyond immediate incidents. Products-and-completed-operations protection covers claims that arise after you've finished a job or sold a product. A homeowner who discovers faulty electrical work six months after your crew left the site can still file a claim under your CGL policy.

One nuance worth knowing: some courts recognize mental or emotional injury (without physical harm) as bodily injury under CGL policies, though this varies by jurisdiction.

Coverage B: Personal and Advertising Injury

Coverage B protects against non-physical harms caused by your business communications or actions. This section covers seven specific offenses:

- Libel, slander, and defamation

- Copyright infringement in your advertising

- Invasion of privacy

- Use of another company's advertising idea

- False arrest or detention

- Wrongful eviction or entry

- Malicious prosecution

Social media disputes and digital advertising have made Coverage B more relevant than ever. A business that inadvertently uses a competitor's trademarked image in a Facebook ad — or faces a defamation claim over a negative online review — can trigger this protection.

Coverage B does have firm limits: it excludes businesses in media, publishing, or internet search industries, and doesn't cover acts committed with knowledge of their falsity.

Coverage C: Medical Payments

Coverage C pays reasonable medical expenses for third parties injured on your premises or during your operations — on a no-fault basis. This means the insurer can pay without determining liability or waiting for a lawsuit.

Covered expenses include medical and surgical costs, ambulance and hospital bills, nursing services, and funeral expenses. Typical limits run $5,000 to $10,000 per person.

The real value is speed. If a customer trips in your store and chips a tooth, Coverage C can immediately pay their dental bill — often preventing a larger bodily injury lawsuit under Coverage A before it starts.

Keep these boundaries in mind:

- Does NOT cover employees (workers' compensation handles this)

- Does NOT provide legal defense

- Does NOT cover athletic participants or product-related injuries

- Has modest sub-limits; large injury claims shift to Coverage A

What CGL Insurance Does NOT Cover

CGL policies contain explicit exclusions for risks that require specialized coverage. Understanding these gaps is critical to avoiding uninsured losses.

Professional Errors and Omissions

CGL doesn't cover mistakes made while delivering professional services — a bad recommendation from a consultant, a design flaw by an architect, a software bug that crashes a client's system, or an accountant's calculation error.

A marketing consultant who recommends a failed campaign strategy won't find coverage here. Neither will an IT provider whose system failure causes a client to lose revenue. These situations call for Professional Liability Insurance (also called Errors & Omissions or E&O coverage).

Employee Injuries and Employment-Related Claims

Workplace injuries and employment practices claims fall outside CGL entirely. If an employee slips in your warehouse and breaks a leg, CGL won't cover their medical bills or lost wages. If you terminate an employee who then sues for wrongful termination, CGL won't defend you.

You'll need separate policies to close these gaps:

- Workers' Compensation Insurance for employee injuries

- Employment Practices Liability Insurance (EPLI) for discrimination, harassment, and wrongful termination claims

Intentional Acts, Vehicles, and Business-Specific Risks

Several other categories are explicitly excluded:

- Intentional acts — deliberate harm to a person or property by you or an employee

- Vehicle accidents — incidents involving company cars, trucks, or delivery vehicles (requires Commercial Auto Insurance)

- Alcohol-related claims — bars, restaurants, and liquor stores need Liquor Liability Insurance for incidents involving intoxicated patrons

- Environmental contamination — pollution, chemical spills, or environmental damage require Pollution Liability Insurance

Cyber Liability: The Critical Gap

Standard CGL policies explicitly exclude cyber incidents through ISO endorsements CG 21 06 and CG 21 07. This means data breaches, ransomware attacks, customer data theft, and business email compromise are not covered.

The 2025 Verizon Data Breach Investigations Report tracked 22,052 security incidents and 12,195 confirmed data breaches. IBM's 2024 Cost of a Data Breach Report found the global average breach cost reached $4.88 million — none of which a standard CGL policy would touch.

What you need instead: Cyber Liability Insurance to cover breach response costs, regulatory fines, customer notification, credit monitoring, and legal defense.

Who Needs CGL Insurance?

If your business fits any of these profiles, CGL coverage is essential—not optional:

Physical premises where customers visit:

- Retail stores, restaurants, hotels

- Offices where clients meet with your team

- Warehouses or showrooms open to vendors

Employees who work at third-party locations:

- Contractors, electricians, plumbers

- Landscapers, cleaning services

- Installation or repair technicians

Businesses that manufacture, sell, or distribute products:

- Product manufacturers

- Wholesalers and distributors

- Retailers selling physical goods

Contractual Requirements and Additional Insured Endorsements

Many contracts require CGL coverage before you can do business. Commercial leases, vendor agreements, and construction contracts routinely mandate that you:

- Carry minimum CGL limits (often $1M per occurrence)

- Name the other party as an additional insured on your policy

An additional insured is a person or organization added to your policy who receives coverage protections. If a third party sues them for your negligence, your CGL policy defends and pays the claim — protecting their own insurance limits from the hit.

This is standard in construction (subcontractors naming general contractors), real estate (tenants naming landlords), and corporate vendor agreements (suppliers naming retailers).

Industry-Specific Examples

Most industries carry CGL for the same core reason — people, property, and unpredictable events. Here's how exposure looks in practice:

Retail: High foot traffic means slip-and-fall exposure. The average slip-and-fall claim costs $45,000, and that's before legal fees.

Hospitality: Hotels and restaurants deal with property damage from guests, food-related illness claims, and ongoing premises liability.

Construction: Falls account for 38.5% of workplace deaths in construction. Contractors also face completed-operations claims years after a project wraps up.

Healthcare: Clinics and outpatient facilities carry CGL for patient injuries unrelated to medical treatment — a patient slipping in the waiting room, for example.

Tech companies: Software firms with physical offices need CGL to cover visitor injuries and property damage. Most also layer on Professional Liability for errors in their software or services.

CGL Policy Types, Limits, and Cost

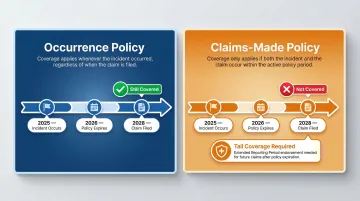

Claims-Made vs. Occurrence Policies

Occurrence policies cover any incident that happens during the policy period, even if the claim is filed years later. If a customer is injured in 2025 but doesn't sue until 2028, your 2025 occurrence policy still covers the claim.

Claims-made policies only cover claims filed while the policy is active (and after a specified retroactive date). If you cancel a claims-made policy, you lose coverage for past incidents unless you purchase "tail coverage."

Occurrence policies provide longer-term protection and are the standard for CGL — especially important for contractors and product manufacturers who face delayed claims. Claims-made policies are more common in professional liability contexts and may cost less upfront.

Policy Limits and Deductibles

CGL policies have two key limits:

| Limit Type | What It Covers | Typical Amount |

|---|---|---|

| Per-occurrence limit | Maximum paid for a single incident | $1 million |

| General aggregate limit | Maximum paid across all claims in a policy year | $2 million |

Most small businesses carry $1M per occurrence / $2M aggregate as a minimum. Don't underestimate what you need: a single fire claim averages $80,000, and a serious bodily injury claim can exceed $1 million. If your limits fall short, your business absorbs the difference.

For larger exposures, a Commercial Umbrella policy extends coverage above your CGL limits — typically an additional $1M to $5M for catastrophic claims.

What Does CGL Insurance Cost?

Your limits selection directly shapes what you'll pay. Beyond that, CGL pricing depends on:

- Industry risk level (construction and manufacturing pay more than office-based businesses)

- Business size and revenue (higher revenue = higher premiums)

- Claims history (prior claims increase costs)

- Location (urban areas with higher lawsuit frequency cost more)

- Coverage limits selected (higher limits = higher premiums)

Typical annual cost for a $1M policy:

- Insureon reports a median of $45/month ($538/year)

- The Hartford reports an average of $68/month ($810/year)

- High-risk industries like construction or manufacturing pay well above these figures

Cost-saving tip: Bundling CGL into a Business Owner's Policy (BOP) often reduces premiums compared to buying standalone property and liability policies individually.

How to Get the Right CGL Coverage for Your Business

You can purchase CGL coverage through three main structures. The right choice depends on your business size, risk profile, and coverage needs.

Standalone CGL Policy

A standalone policy works best for businesses with complex or elevated liability risks that don't own commercial property, or those needing customized limits and endorsements — for example, a consulting firm that works at client sites but leases rather than owns office space.

Business Owner's Policy (BOP)

A BOP bundles CGL, commercial property insurance, and business interruption coverage into one package — typically available to businesses with fewer than 100 employees and under $5 million in annual revenue. It's the most cost-effective option for small-to-medium businesses with straightforward risks, combining simplified purchasing with lower premiums than buying each coverage separately.

Commercial Package Policy (CPP)

A CPP suits larger businesses or those with complex, high-risk operations — heavy manufacturing, multi-location setups, or industries that don't fit standard BOP eligibility. It combines CGL, property, auto, and other specialized policies into one customizable program with flexible limits and endorsements.

Working with a Specialized Broker

Standard markets regularly decline or underprice coverage for businesses in construction, hospitality, manufacturing, and other higher-risk industries. A broker with access to specialty carriers can make the difference between adequate coverage and a significant gap.

When evaluating brokers, look for:

- Access to multiple carriers, including surplus lines markets like Markel and Kinsale

- Experience placing coverage in your specific industry

- Speed — complex placements shouldn't take weeks

- Transparent communication about exclusions and coverage gaps

Soma works with hundreds of carrier partners — including Chubb, Liberty Mutual, and Markel — to place CGL coverage for businesses that standard markets often turn away. One application generates quotes across multiple carriers, so you're comparing real options rather than waiting on a single response.

Frequently Asked Questions

Who needs commercial general liability insurance and why?

Any business with public-facing operations, physical premises, employees working off-site, or products in the market needs CGL. Many clients, landlords, and general contractors contractually require it before signing agreements, making it a practical necessity for doing business.

How much does a $1,000,000 commercial general liability policy cost?

Most small businesses pay between $300 and $1,000 annually for a $1M policy. Cost varies significantly based on industry (construction pays more than consulting), business size, location, and claims history.

What's the difference between general liability and commercial general liability?

The terms mean the same thing. "Commercial general liability" is the formal name for the standardized ISO policy form introduced in 1986; "general liability" is the shorthand most business owners and brokers use.

What's the difference between an LLC and general liability insurance?

An LLC protects your personal assets by separating business and personal liability, but it doesn't pay for legal defense or damages if the business is sued. CGL insurance handles those costs. The two work together — one shields your personal assets, the other covers the business when claims arise.

What does Coverage A of a commercial general liability policy cover?

Coverage A covers third-party bodily injury and property damage caused by your premises, operations, products, or completed work. It pays both legal defense costs and any resulting judgments or settlements, up to the policy limit.

What is the most common general liability claim?

Slip-and-fall incidents are the most frequent CGL claims, averaging $45,000 per incident. Property damage from business operations and advertising injury claims follow closely — water damage and burglary each account for roughly 20% of small business claims.