Introduction

Picture this: A small accounting firm owner arrives Monday morning to find their client portal locked, their files encrypted, and a ransom demand on every computer screen. Panicked, they call their insurance agent, only to learn their general liability policy won't pay a cent. The breach exposed tax documents for 300 clients, and the forensic investigation alone will cost $45,000. This scenario plays out daily across American businesses — and it's exactly why cyber liability coverage exists.

AI-assisted phishing emails doubled over the past two years, and ransomware now appears in 44% of all data breaches. Yet most standard business insurance policies — general liability, property, even business owner's policies (BOPs) — offer zero protection against digital threats.

The financial stakes are staggering: according to IBM's 2025 Cost of a Data Breach Report, the global average cost of a data breach hit $4.44 million.

This guide covers what cyber liability insurance is, the two main coverage types, what's included and excluded, who needs it, and how to get it.

TLDR: Key Takeaways

- Cyber liability insurance protects businesses from financial losses caused by data breaches, ransomware, and cyber incidents

- First-party coverage pays your own losses from a breach or attack

- Third-party coverage defends you against lawsuits from affected customers

- Standard policies like general liability or BOP don't cover cyber incidents

- Any business storing customer data, processing payments, or operating online needs coverage

What Is Cyber Liability Coverage?

Cyber liability coverage is business insurance that financially protects organizations when they experience cyber incidents — data breaches, ransomware attacks, network outages — resulting in financial loss, legal exposure, or reputational harm.

How It Differs from Traditional Insurance

General liability and property policies cover physical risks: bodily injury, property damage, slip-and-fall accidents. They're typically silent on digital threats. Cyber liability fills this gap specifically for technology-related risks.

General liability responds when a customer trips in your store. When a hacker steals customer credit cards from your database, that's a cyber liability claim — general liability won't cover it.

Origins and Evolution

The first cyber policy was written in 1997 by AIG to cover third-party hacker liability for companies storing credit card numbers. As businesses moved online in the late 1990s, cyber insurance emerged to protect early e-commerce pioneers.

The market has grown with the threat landscape. According to the NAIC's 2025 Cybersecurity Insurance Report, the U.S. cyber insurance market reached $9.14 billion in 2024. Coverage has expanded from basic hacker liability to comprehensive protection covering forensic investigations, ransomware payments, business interruption, regulatory fines, and reputational crisis management.

Common Terminology and Policy Types

"Cyber liability insurance," "cyber insurance," and "data breach insurance" are often used interchangeably — but coverage scope varies significantly between policies. Some are standalone policies; others are endorsements added to existing business coverage. The label matters less than what's actually covered, so always review the policy terms directly.

What a Cyber Incident Looks Like

Real-world cyber incidents include:

- A phishing email that compromises employee credentials, allowing attackers to access customer databases

- A ransomware attack that locks access to business systems for days or weeks

- A vendor breach that exposes customer records your business is responsible for protecting

- Business email compromise where an employee is tricked into wiring funds to a fraudulent account

Understanding what triggers a claim helps clarify exactly what coverage you need — which is where policy structure becomes critical.

First-Party vs. Third-Party Cyber Liability Coverage

Cyber liability policies contain two foundational coverage structures: first-party coverage (losses your own business suffers) and third-party coverage (liability claims brought against your business by others harmed by a breach you experienced).

First-Party Coverage

First-party coverage pays for direct costs your business incurs:

- Restoring or reconstructing damaged, corrupted, or stolen data

- Recovering lost revenue and ongoing operating expenses when a cyberattack halts operations

- Covering ransom payments (where legal) and negotiation costs

- Funding computer forensics to identify how the breach occurred

- Managing public relations and reputation damage

- Sending legally required notifications to affected individuals and regulators

These costs hit immediately after an attack — before any outside party files a claim. That's where third-party coverage takes over.

Third-Party Coverage

Third-party coverage protects you when customers, partners, or regulators take action against your business:

- Covering attorney fees and court costs for breach-related lawsuits

- Paying settlements or judgments you're legally obligated to fulfill

- Covering regulatory fines under breach notification laws like HIPAA, CCPA, and GDPR

- Defending against claims of defamation or copyright infringement in digital content

For regulated industries, this side of the policy matters most. HIPAA fines alone can reach $1.9 million per violation category — and that's before any civil litigation from affected patients or customers.

Coverage Structure

Most cyber liability policies include both first- and third-party components, but coverage limits and specific inclusions vary by policy. Review both sides carefully — the breadth of one doesn't guarantee the other is adequate for your industry.

Note on "Second-Party" Coverage: "Second-party" is not a standard insurance category. In insurance, the first party is the policyholder, the second party is the insurer, and the third party is anyone else harmed by the incident.

What Does Cyber Liability Insurance Cover?

Cyber liability policies typically cover six core areas — though exact coverage varies by carrier and policy terms:

Data Breach Response Costs

This coverage pays for forensic investigation, legal counsel, and mandatory notifications to affected individuals and regulators. When a breach occurs, most states require notification within 30-60 days. Notifications alone can run $50-$150 per individual once you factor in credit monitoring services.

Business Interruption Losses

Compensates for lost revenue and ongoing operating expenses when a cyberattack forces a business to halt or limit operations. A ransomware attack that shuts down systems for three days can cost a mid-sized business $100,000+ in lost revenue alone, not counting recovery costs.

Ransomware and Cyber Extortion

This covers ransom payments (where legally permissible) along with negotiation costs and system restoration. According to the Verizon 2025 Data Breach Investigations Report, the median ransom paid in 2024 was $115,000 — though 64% of victims refused to pay and relied on backups instead.

Data Restoration Costs

This covers the cost of recovering or reconstructing data lost during an attack — whether that means restoring from backups or rebuilding records that can't be retrieved.

Legal Defense and Regulatory Fines

This covers attorney fees and regulatory fines stemming from investigations or lawsuits after a breach. Recent enforcement examples include:

| Regulator | Entity | Year | Fine Amount | Violation |

|---|---|---|---|---|

| CPPA (CCPA) | Tractor Supply Co. | 2025 | $1.35 million | Failure to provide effective opt-out mechanisms |

| Irish DPC (GDPR) | LinkedIn Ireland | 2024 | €310 million | Unlawful processing of personal data for advertising |

| HHS OCR (HIPAA) | MMG Fusion, LLC | 2024 | $10,000 | Failure to conduct risk analysis and notify of breach |

Optional Add-Ons

Some policies include coverage for social engineering and fraud (business email compromise where an employee is tricked into wiring funds), media liability, and reputational harm — but these are often optional. Always review policy language carefully to confirm which add-ons apply to your specific risk profile.

What Cyber Liability Insurance Does NOT Cover

Cyber liability insurance doesn't cover everything. Policies exclude events that were preventable, resulted from negligence, or fall outside digital risk scope.

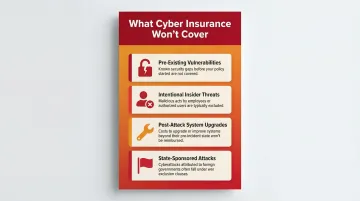

Common Exclusions

- Pre-existing vulnerabilities: Known security gaps that existed before policy purchase — and were never remediated — are excluded from coverage.

- Intentional insider threats: Deliberate employee sabotage is not covered. Some policies allow accidental employee-caused incidents, but intentional acts are off the table.

- System upgrades post-attack: Costs to harden or improve your infrastructure after a breach are not reimbursable. Insurers pay to restore what you had, not to fund upgrades.

- State-sponsored attacks: Many policies include "war exclusions" covering nation-state cyberattacks. After the $1.4 billion Merck v. ACE dispute over the "NotPetya" attack, Lloyd's of London mandated strict new exclusions for state-backed incidents that impair national security. This area is still evolving — ask about it specifically when shopping.

The Security Controls Requirement

Cyber insurance is not a substitute for proactive cybersecurity measures. Insurers increasingly require businesses to have basic controls in place — multi-factor authentication (MFA), endpoint protection, employee training — before issuing a policy. Poor security posture can result in denied claims or higher premiums.

This isn't theoretical. The City of Hamilton was denied an $18.3 million cyber insurance payout because MFA wasn't universally enforced — despite being attested during underwriting. Insurers treat "almost everywhere" as the same as nowhere.

Which Businesses Need Cyber Liability Coverage?

Small Businesses Are Prime Targets

Hiscox's 2023 Cyber Readiness Report found that 41% of U.S. small businesses experienced a cyberattack in the past year — yet many still assume cyber insurance is only for large corporations. Small and mid-sized businesses are frequent targets precisely because they tend to have weaker security controls and fewer resources to recover on their own.

High-Risk Industries

Industries with the highest cyber risk exposure include:

- Healthcare providers - Storing patient records under HIPAA regulations

- Financial services firms - Handling sensitive account data and payment information

- Retailers - Processing payment card data subject to PCI DSS requirements

- Tech companies - Holding intellectual property and client data

- Hospitality businesses - Managing reservations and payment systems

- Manufacturers - At risk from operational technology attacks and supply chain compromises

Key Triggers Indicating You Need Coverage

Your business needs cyber liability coverage if you:

- Store any form of customer personally identifiable information (PII) — names, emails, payment info, health data

- Accept online payments or process credit cards

- Use cloud-based software or remote work tools

- Work with third-party vendors who access your systems

- Rely on digital systems to operate your business

Most businesses today check at least one of these boxes. The question isn't whether you're exposed — it's whether you're covered when an incident happens.

How to Get Cyber Liability Insurance

The Application Process

Businesses apply by providing information about size, revenue, industry, data handling practices, and existing security controls. Insurers use this to assess risk and determine premium. Coverage limits commonly range from $1 million to $5 million, with premiums varying based on industry and risk profile.

That cost varies significantly depending on your business. According to Insureon's 2026 data, the average cost for small businesses is approximately $134 per month, or $1,609 annually. Costs scale based on revenue, data volume, deductible choice, and the strength of your cybersecurity controls.

Required Security Controls

Insurers now treat security controls as mandatory baseline requirements:

| Security Control | Impact | Value |

|---|---|---|

| Multi-Factor Authentication (MFA) | Mandatory for remote access, email, admin accounts | Prevents 99.9% of account compromise attacks |

| Endpoint Detection & Response (EDR) | Required for medium-to-large businesses | Identifies and isolates suspicious activity before lateral movement |

| Immutable/Offline Backups | Mandatory for ransomware coverage | Ensures data recovery without paying extortion demands |

| Employee Training | Required annually, including phishing simulations | Mitigates the human element responsible for 68% of breaches |

Implementing these controls not only ensures insurability but can yield premium discounts and lower deductibles.

Once those controls are in place, the next step is finding a policy that actually fits your exposure.

What to Look for When Comparing Policies

- Coverage limits for both first- and third-party scenarios

- Sublimits on specific coverages like ransomware

- Claims process and response time — how quickly the insurer responds when you have an incident

- Retroactive coverage dates — whether prior acts are covered

- Incident response services — whether the policy includes access to forensic experts and legal counsel

A specialized brokerage can simplify this comparison considerably. Soma, for example, works with carriers like Chubb, Liberty Mutual, and Markel, allowing businesses to get quotes tailored to their industry and risk profile — often without the weeks-long delays that come with going carrier-direct.

Frequently Asked Questions

Do I need cyber liability coverage?

If your business stores customer data, processes payments online, or relies on digital systems to operate, cyber liability coverage is strongly recommended. In regulated industries like healthcare or finance, it may be functionally required to comply with breach notification laws.

What is the average cost of cyber liability insurance?

For small businesses, the average cost is approximately $134 per month, or $1,609 annually, according to Insureon's 2026 data. Premiums vary widely based on industry, revenue, data volume, and existing security controls.

What is not covered under cyber insurance?

Common exclusions include pre-existing breaches, intentional insider acts, infrastructure upgrade costs, and in many policies, acts of war or nation-state attacks. Always review exclusions carefully before purchasing.

What is the difference between first-party and third-party cyber liability coverage?

First-party coverage pays for your own business's losses — recovery costs, notifications, and business interruption. Third-party coverage handles liability claims from customers or partners harmed by your breach. Most policies bundle both.

Is cyber liability insurance required?

Cyber liability insurance is not federally mandated in the U.S., but certain industries (healthcare, finance) face regulations that effectively make it necessary, and some business contracts or government procurement requirements now require it.

What are common cyber insurance claims?

Ransomware, business email compromise, data breaches, and malware-caused outages top the list. According to Coalition's 2026 Cyber Claims Report, email compromise and funds transfer fraud made up 60% of all claims — while ransomware remains the most financially damaging.