Introduction

Picture this: A consultant slips on an icy walkway at a client's office and fractures her wrist. The medical bills hit $15,000. That same week, a different client sues her for recommending a software platform that crashed during peak season, costing them $200,000 in lost revenue.

Two incidents. Two lawsuits. But only one insurance policy will respond to each claim. They're not interchangeable.

This confusion costs U.S. small businesses dearly. 77% of SMBs are underinsured, and most owners can't correctly explain the difference between their two most critical policies. The result? Coverage gaps that leave businesses financially exposed when claims hit.

This guide explains exactly what each policy covers, who needs what, and where the gaps are — so you can make coverage decisions based on facts, not assumptions.

Key Takeaways

- General liability covers bodily injury, property damage, and advertising injury from your business operations

- Professional liability covers financial harm from errors, negligence, or failure to deliver professional services

- GL is essential for any business with a physical location or direct customer interaction

- PL is essential for service providers, consultants, and licensed professionals

- Healthcare, finance, tech, and consulting firms typically need both policies

- Neither policy covers employee injuries (workers' comp) or data breaches (cyber liability)

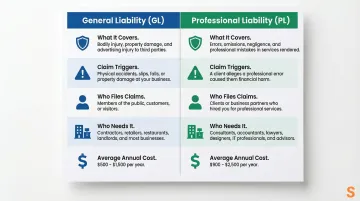

General Liability vs. Professional Liability: Quick Comparison

Here's how the two policies stack up across the factors that matter most for your business.

| Factor | General Liability (GL) | Professional Liability (PL) |

|---|---|---|

| What it covers | Bodily injury, property damage, advertising injury | Errors, omissions, negligence, breach of professional duty |

| What triggers a claim | Customer slips and falls; property is damaged; competitor sues over ad copy | Client suffers financial loss due to your advice, missed deadline, or professional mistake |

| Claim filed by | Third parties: customers, visitors, vendors | Clients receiving your professional services |

| Who typically needs it | Virtually all businesses with physical locations or client-facing operations | Service providers, consultants, healthcare professionals, finance/tech professionals |

| Average cost range | $540–$1,020 annually for $1M/$2M coverage | $504–$1,051 annually for $1M/$2M coverage |

| Can clients require it? | Yes—routinely required via Certificate of Insurance (COI) for contracts | Yes—often mandatory for professional service contracts and state licensing |

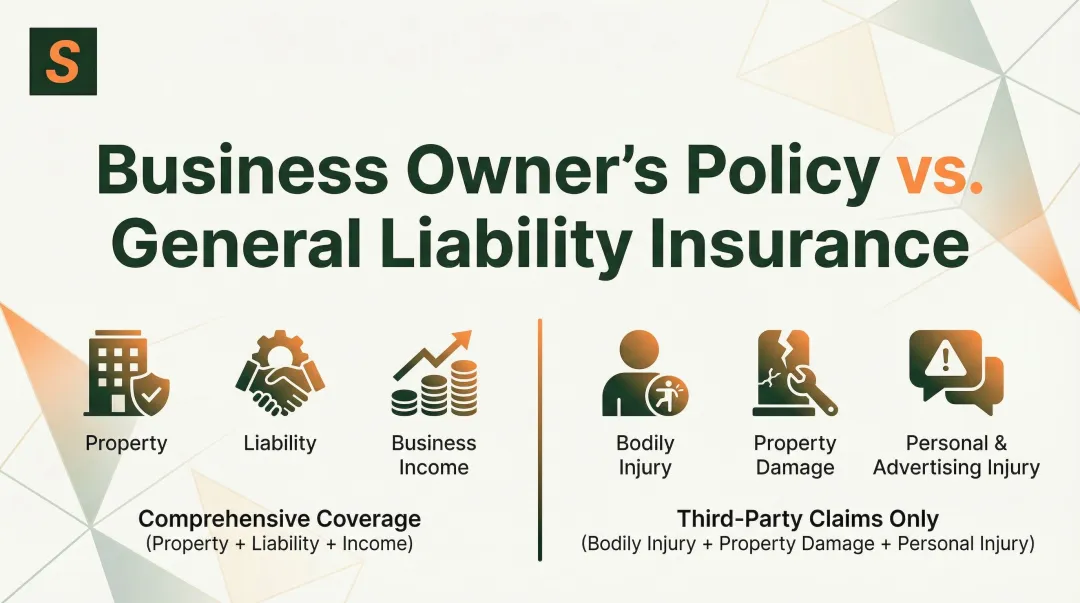

What is General Liability Insurance?

General liability (GL) insurance is the foundational business policy that protects companies from third-party claims involving physical harm or property damage connected to business operations. For most businesses, it's the first policy you should buy.

Core Coverages

Bodily Injury — A customer trips over equipment in your warehouse and breaks an ankle. GL covers medical expenses and legal defense if they sue.

Property Damage — Your employee accidentally knocks over a client's $8,000 server rack during a service call. GL pays for the replacement and any business interruption losses.

Personal and Advertising Injury — A competitor claims your marketing campaign copied their slogan and sues for copyright infringement. GL covers your legal defense and potential settlement.

According to Verisk's 2024 analysis, bodily injury accounts for 45% of GL losses with average severity reaching $154,201, while property damage averages $46,924 per claim.

What General Liability Does NOT Cover

GL policies explicitly exclude:

- Employee injuries (that's workers' compensation)

- Professional errors or bad advice (that's professional liability)

- Cyber incidents and data breaches

- Intentional acts or fraud

- Auto accidents (that's commercial auto insurance)

- Damage to your own business property

Who Needs GL Insurance

Most businesses need general liability coverage, but it's non-negotiable for:

- Contractors and construction trades

- Retail stores and restaurants

- Hospitality businesses

- Manufacturers

- Any company with a physical location where customers, vendors, or the public visit

Cost Factors for GL Insurance

Your premium depends on several variables:

- Industry risk level — Construction pays more than consulting

- Annual revenue — Higher sales indicate more transactions and exposure

- Location — Urban areas and litigious states cost more

- Employee count — More workers mean more potential incidents

- Claims history — Prior claims drive up renewal costs

- Coverage limits — Higher limits mean higher premiums

High-risk industries like construction, roofing, and plumbing typically face the steepest premiums due to routine operations that can trigger massive property damage or completed-operations claims.

Use Cases of General Liability Insurance

These scenarios show how GL pays out across common industries:

Retail Store Scenario — A customer slips on a wet floor during a rainstorm and suffers a concussion. According to The Hartford's 10-year claims analysis, slip-and-fall claims now average $45,000—double what they cost a decade ago.

A plumbing contractor accidentally breaks a water pipe in a client's home, flooding the basement and destroying $30,000 worth of finished flooring and electronics. GL covers the property damage and lost-use expenses.

Marketing Agency Scenario — An agency's ad campaign unintentionally uses a copyrighted image. The photographer sues for $25,000. GL's advertising injury coverage handles the legal defense and settlement.

What is Professional Liability Insurance?

Professional liability insurance—also called Errors & Omissions (E&O) or malpractice insurance in healthcare—protects businesses when their professional services cause a client financial harm, even when no physical damage occurred.

The critical distinction: you don't have to be actually at fault to face a costly lawsuit. Defending against claims of negligence can cost $50,000 to $100,000 even when you win.

Core Coverages

Negligence — An accountant files an incorrect tax return, triggering IRS penalties of $12,000 for the client. Professional liability covers both the penalty and legal defense costs.

Errors and Omissions — A web developer's coding mistake crashes an e-commerce site during Black Friday, costing the client $150,000 in lost sales. That financial loss claim falls squarely on the developer without E&O coverage.

Failure to Deliver — A consultant's strategic advice leads to a failed market expansion. The client sues for $500,000 alleging negligence. Professional liability covers defense costs and any settlement, even if the consultant believed the advice was sound.

CNA's 2024 claims data shows nurse professional liability claims average $236,749, while aging services claims average $259,443.

What Professional Liability Does NOT Cover

PL policies exclude:

- Bodily injury or property damage (GL covers that)

- Intentional wrongdoing or fraud

- Employee disputes or employment practices claims

- Claims from products rather than services

- Criminal acts

Industry-Specific Variations

Professional liability takes different forms across industries:

- E&O — For consultants, tech companies, financial advisors, and real estate professionals

- Medical Malpractice — For physicians, nurses, and healthcare providers

- Legal Malpractice — For attorneys and law firms

- Directors & Officers (D&O) — For corporate executives (covers management decisions, not professional services)

Some states legally require specific professional liability coverage. For example, Oregon requires attorneys to maintain $300,000 coverage through the Professional Liability Fund, while Florida requires physicians to carry $100,000/$300,000 or higher malpractice limits.

Who Needs PL Insurance

Professional liability is essential for:

- Lawyers and legal professionals

- Accountants and bookkeepers

- Financial advisors and investment professionals

- IT professionals and software developers

- Healthcare providers

- Architects and engineers

- Consultants and marketing agencies

Even businesses that don't think of themselves as professional service providers face client disputes over deliverables — E&O coverage protects against those claims.

General Liability vs. Professional Liability: Which Does Your Business Need?

The decision framework is straightforward: GL protects against "what happens at or because of your business physically," while PL protects against "what happens as a result of your expertise or advice."

Ask yourself two questions:

- Do customers, vendors, or the public interact with my physical space or operations?

- Do clients rely on my professional judgment, services, or deliverables?

Situational Recommendations

Choose GL if:

- You're a contractor, retailer, restaurant, or manufacturer

- Customers visit your physical location

- Your employees work at client sites

- Your operations could cause bodily injury or property damage

Choose PL if:

- You're a consultant, accountant, lawyer, or IT professional

- Clients pay you for expertise, advice, or professional services

- Your deliverables could cause financial losses

- You provide healthcare, financial, or technical services

Choose BOTH if:

- You're a healthcare provider (physical injuries + professional errors)

- You run a financial services firm (office visitors + investment advice)

- You're a tech company (office operations + software services)

- You operate any business that both has customer-facing operations AND provides professional services

The Coverage Gap Problem

Most businesses choose one policy and assume they're covered. That assumption is costly. Only 31-42% of SMBs carry professional liability, while 62-65% carry general liability—leaving a massive exposure gap for service providers.

Carrying only one policy creates dangerous vulnerabilities. If a client suffers financial harm from your advice, your GL policy will deny the claim—it explicitly excludes professional services. Conversely, if someone gets injured at your office, your PL policy won't respond.

Client Contracts and State Regulations

Client contracts and state regulations often determine which policies are required. Certificates of Insurance (COIs) are now standard, non-negotiable prerequisites in commercial contracts, particularly in construction, real estate, and professional services.

Some clients won't sign contracts without proof of both GL and PL coverage. Certain professions—healthcare, law, finance, real estate—may be legally required to carry professional liability to maintain their licenses.

Finding the Right Coverage

Matching coverage to your specific business can get complicated—particularly for hard-to-insure operations like late-night bars, hazmat trucking, or SaaS startups. Soma works with hundreds of carrier partners, including Chubb, Liberty Mutual, and Markel, to place the right coverage for businesses that standard brokers often decline. One application returns industry-specific quotes without the usual wait.

Conclusion

General liability and professional liability aren't competing options—they protect against fundamentally different risks. The right choice depends on whether your business faces physical/third-party exposure, professional service exposure, or both.

Most businesses with any client-facing service component benefit from carrying both policies. The cost of dual coverage—typically $1,000 to $2,000 annually for small businesses—is minimal compared to the catastrophic financial exposure of facing an uncovered $200,000 lawsuit.

Coverage needs shift as your business changes — new services, new clients, and new contracts can open gaps you didn't have before. Revisit your policies annually, and work with a broker who has access to multiple carriers and can place the right coverage fast, especially if your business operates in a complex or hard-to-insure space.

Frequently Asked Questions

How much does a $1,000,000 general liability insurance cost?

The average cost for a $1M per-occurrence / $2M aggregate GL policy ranges from $540 to $1,020 annually ($45 to $85 per month) for U.S. small businesses. High-risk industries like construction pay significantly more, while low-risk consultants pay less. Cost depends on industry, revenue, location, and claims history.

Do I need both general liability and professional liability insurance?

Most service-based businesses need both. GL covers physical injuries and property damage; PL covers professional errors and financial losses. A claim in the excluded category means you pay defense costs and settlements out of pocket.

What is considered professional liability insurance?

Professional liability (also called E&O or malpractice insurance) covers financial losses a client suffers due to professional negligence, errors, omissions, or failure to deliver services as promised. It applies to any business providing expert advice, professional services, or specialized deliverables.

What does commercial general liability not cover?

GL excludes professional errors/omissions, employee injuries (workers' comp), intentional acts, auto accidents (commercial auto), cyber events (cyber liability), and damage to your own property. If a client sues over bad advice rather than physical harm, GL won't respond — that's where professional liability picks up.

What is not covered by professional liability insurance?

PL excludes bodily injury and property damage (GL), intentional fraud or criminal acts, employment disputes (EPLI), and product-related physical harm. If someone is injured on your premises rather than harmed by your advice, you'll need GL coverage to respond.

Is public liability insurance the same as professional liability insurance?

No. "Public liability" is a UK/Australian term for what the U.S. calls general liability—it covers third-party injury and property damage. Professional liability specifically covers financial harm from professional services. They are distinct coverages protecting against different risks.