Introduction

Construction accounts for roughly 20% of all US workplace fatalities each year — yet many small contractors are underinsured against the risks they face daily. Between jobsite falls, equipment theft, third-party property damage, and the legal liability attached to every project, a single workplace injury or lawsuit can wipe out years of profit before the next bid goes out.

Generic small business coverage won't protect you here. Standard Business Owner's Policies (BOPs) routinely exclude the risks construction businesses face most — tools in transit, contractor defect claims, and damage to structures mid-build. Specialized construction insurance is a baseline requirement for operating responsibly and staying solvent.

This guide covers the 9 essential insurance types small construction businesses should carry — what each policy covers, who needs it, and when it's legally or contractually required.

Key Takeaways

- Construction businesses face industry-specific risks—jobsite injuries, equipment theft, third-party liability—that require specialized coverage, not generic policies

- The 9 essential coverages span liability, property, workers' protection, vehicle use, and digital risk—each addressing a distinct exposure small contractors face

- Legal requirements cover workers' comp and commercial auto; clients and project contracts typically mandate general liability and builder's risk

- Costs vary widely by trade, revenue, and location—bundling policies can cut premiums by 10–20% or more

Why Small Construction Businesses Need Specialized Insurance Coverage

Construction consistently ranks among the most dangerous industries in the United States. In 2024, the Bureau of Labor Statistics recorded 1,034 fatal work injuries in construction and extraction occupations, with a fatal injury rate of 9.2 deaths per 100,000 full-time workers—nearly three times the national average of 3.3 per 100,000.

Small construction businesses face compounding risk exposure:

- They work with subcontractors across multiple jobsites

- They own expensive equipment that moves between locations

- They handle client contracts with strict liability requirements

- They face legal obligations that vary by state and project type

Generic small business policies routinely exclude construction-specific risks like contractor defect claims, damage to structures under construction, or tools stolen from jobsites. Standard BOPs cover fixed-location assets—office furniture, computers—but exclude mobile equipment, in-transit materials, and completed operations liability.

Those coverage gaps carry a steep price. The National Safety Council reports that work injuries cost employers $176.5 billion in 2023, covering medical expenses, lost wages, and productivity losses.

Yet 77% of small businesses are underinsured—leaving them personally liable for claims that can exceed their annual revenue.

The 9 Essential Types of Insurance for Small Construction Businesses

Below is a breakdown of each policy type—what it covers, why small construction businesses need it, and when it's required by law or contract.

General Liability Insurance

General Liability (GL) is the foundational policy for any construction business. It covers third-party bodily injury, property damage, and advertising injury claims arising from your business operations or completed work. The products-completed operations endorsement is critical—it protects you from claims filed months or years after a project is finished, such as a client alleging faulty workmanship caused property damage.

Most states require proof of GL coverage as a condition for contractor licensure. Washington State mandates $200,000 in public liability and $50,000 in property damage, while Georgia requires $300,000 to $500,000 per occurrence depending on license tier. Many general contractors and project owners also require subcontractors to carry GL before awarding contracts, making this coverage non-negotiable in practice.

Workers' Compensation Insurance

Workers' comp covers medical expenses and lost wages for employees injured on the job. Most states legally require any construction business with at least one employee to carry it, with severe penalties for non-compliance including fines, license suspension, and personal liability for injury costs.

Construction faces stricter mandates than most other industries. While some states allow exemptions for businesses with 3–5 employees, Florida requires workers' comp for construction firms with just 1 employee. Employer's liability coverage, typically bundled with workers' comp, protects against employee lawsuits alleging unsafe working conditions.

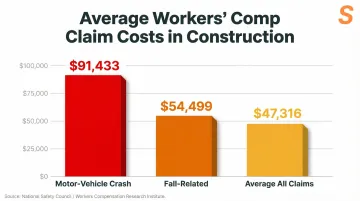

The cost of not carrying coverage quickly becomes clear in claim data:

- Average workers' comp claim: $47,316

- Motor-vehicle crash claims: $91,433 average

- Fall-related claims: $54,499 average

Commercial Auto Insurance

Personal auto policies do not cover vehicles driven to jobsites, used for hauling materials, or operated for any business purpose. Commercial auto insurance is essential for any construction business that owns or uses vehicles in operations—trucks, vans, trailers, or heavy equipment transported on public roads.

Most states mandate commercial auto coverage for business-owned vehicles. Transportation incidents accounted for 38.2% of all workplace fatalities in 2024 (1,937 deaths), making this the deadliest hazard contractors face. Bodily injury claim severity increased 9.2% from 2023 to 2024, driven by medical inflation and litigation costs. For larger vehicles like dump trucks or concrete mixers, specialized commercial truck policies may be required.

Builder's Risk Insurance

Builder's risk (also called course-of-construction insurance) covers buildings and structures under active construction or renovation for damage caused by fire, weather, vandalism, or theft. It fills a critical gap: standard property insurance doesn't cover unfinished structures, and general liability doesn't cover damage to the project itself.

The AIA A201 General Conditions typically assign the project owner responsibility for purchasing builder's risk on an "all-risks" basis. In practice, lenders financing the project require proof of coverage before releasing funds, and contractors are often required to purchase it for custom builds or renovations. Builder's risk is priced at 1–4% of the total completed value of the project—a $500,000 custom home might cost $5,000 to $20,000 to insure against total loss from fire or storm before completion.

Commercial Property Insurance

Commercial property insurance covers a construction business's owned or rented physical assets—office space, tools stored on-premises, furniture, and equipment—against losses from fire, theft, vandalism, wind, or lightning. This policy protects fixed-location assets only; it does not cover tools or equipment once they leave the premises.

General liability, commercial property, and business interruption coverage can often be bundled into a Business Owner's Policy (BOP), which can be a cost-effective option for smaller construction businesses with a physical office or storage location. However, BOPs typically exclude mobile equipment and in-transit materials, making additional coverage necessary for most contractors.

Inland Marine / Tools & Equipment Insurance

Inland marine insurance (and the related contractor's tools and equipment coverage) protects movable property—tools, mobile equipment, and materials—that are in transit, stored off-site, or on an active jobsite. It covers losses from theft, vandalism, or accidental damage wherever the property travels.

The distinction matters: commercial property insurance covers items at a fixed location, while inland marine covers items wherever they go. Construction equipment theft costs the U.S. industry up to $1 billion annually, with recovery rates below 25% due to a lack of standardized identification and rapid resale. Inland marine policies are split into scheduled equipment (high-value items like excavators listed individually) and unscheduled equipment (blanket coverage for smaller tools under a certain value).

Professional Liability (Errors & Omissions) Insurance

Professional liability insurance (E&O) protects against client claims alleging mistakes, omissions, substandard work, or missed deadlines. It covers legal defense costs, settlements, and judgments—even if the claim is unfounded. Standard GL policies exclude damages from professional errors or design flaws, making E&O essential for contractors offering design-build services, project management, or any consulting role.

Design-build utilization is projected to hit 47% of all construction spending by 2025, shifting design-related liability from architects directly to contractors. A 2026 survey of professional liability insurers found that 60% experienced higher claim severity in 2025, with 93% citing rising defense costs and 80% identifying structural engineering as the discipline with the highest claim severity.

Cyber Liability Insurance

Construction businesses store sensitive data—client contracts, payment information, employee records—and rely on digital tools for project management, making them active targets for ransomware, phishing, and data breaches. Cyber liability insurance covers regulatory fines, breach response costs, and litigation expenses.

Small businesses are frequently targeted because they have weaker cybersecurity defenses than large firms. Ransomware is present in 88% of all small and medium business breaches, and the average cost of a data breach in the United States hit a record high of $10.22 million in 2025. Business email compromise (BEC) is a common attack vector, intercepting wire transfers between general contractors and subcontractors.

Commercial Umbrella / Excess Liability Insurance

Umbrella insurance provides an additional layer of liability coverage that kicks in when the limits of an underlying policy—general liability, commercial auto, or employer's liability—are exhausted. It protects against catastrophic claims that exceed standard policy limits.

For small construction businesses working on larger projects or for commercial clients, umbrella coverage is increasingly required by contract. It's a cost-effective way to significantly extend protection. For example, if your general liability policy has a $1 million limit and a claim reaches $2 million, the umbrella policy covers the additional $1 million (minus any applicable deductible).

How to Build the Right Insurance Package for Your Construction Business

The right insurance mix depends on several business-specific factors:

- Trade type: Roofing and steel erection carry higher risk than painting or carpentry

- Number of employees: More workers mean higher workers' comp premiums

- Project scale: Larger projects require higher liability limits

- Subcontractor use: General contractors need coverage for subcontractor-caused incidents

- State regulations: Workers' comp thresholds and licensing requirements vary widely

A common mistake is underinsuring to save on premiums. A single lawsuit or major loss can far exceed years of premium savings. Small businesses should assess their highest-risk exposures first and build coverage around those.

Working with a specialized insurance brokerage like Soma allows small construction businesses to get coverage quotes matched to their operations through a single application. Soma works with hundreds of carrier partners — including Chubb, Liberty Mutual, and Markel — to place project-specific and contractor program coverage quickly, without the back-and-forth of chasing multiple brokers.

How Much Does Construction Insurance Cost for Small Businesses?

Construction insurance costs vary based on trade type, annual revenue, employee count, location, and claims history. There's no single industry-wide price — every quote is individualized.

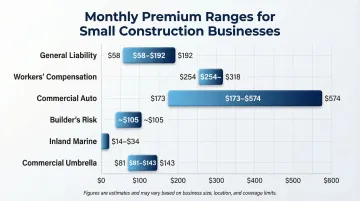

Indicative Monthly Premium Ranges:

- General Liability: $58 to $192 per month

- Workers' Compensation: $254 to $318 per month

- Commercial Auto: $173 to $574 per month

- Builder's Risk: $105 per month (or 1-4% of project value)

- Inland Marine / Tools: $14 to $34 per month

- Commercial Umbrella: $81 to $143 per month

These are ballpark figures to help set budget expectations, not guarantees. A low-risk artisan contractor might pay around $2,500 annually for basic GL and workers' comp. A high-risk trade like roofing with multiple vehicles can easily exceed $17,000 annually.

Bundling through a Business Owner's Policy (BOP) or working with a broker who shops across multiple carriers are the two most reliable ways to control costs. Either approach can reduce your total premium without cutting the coverage your jobs actually require.

Conclusion

Small construction businesses face a uniquely complex risk profile. Skipping or undervaluing key coverages to cut costs often creates far greater financial exposure than the premiums saved. A single uninsured incident can wipe out years of profit or force a business to close entirely.

Getting the right coverage starts with understanding your specific exposure. Before purchasing or renewing any policy, work through these three areas:

- Your trade risks — the hazards specific to your work (roofing, excavation, electrical, etc.)

- State requirements — workers' comp thresholds, contractor licensing bonds, and any mandated minimums

- Contract obligations — coverage types and limits your clients or GCs require before work begins

If you need help placing construction coverage — especially if your business has been flagged as hard-to-insure — Soma works with hundreds of carrier partners to find the right fit. Reach out for a customized quote.

Frequently Asked Questions

What kind of insurance should a construction company have?

At minimum, most construction companies need general liability, workers' compensation, and commercial auto insurance. Builder's risk, inland marine, and professional liability are added based on project type and trade. Contract requirements and state licensing rules often dictate the full package.

How much does insurance cost for a small construction business?

Costs vary by trade, revenue, employee count, and location. Small contractors typically pay $2,500 to $10,000+ annually. Roofing and steel erection trades pay significantly more than painting or carpentry. Bundling options like BOPs can reduce total premiums.

Is workers' compensation required for small construction businesses?

Most states require workers' comp for any construction business with at least one employee — Florida at the 1-employee threshold, Georgia at 3+. Penalties for non-compliance include fines, license suspension, and personal liability for injury costs. Sole proprietors may be exempt but should evaluate coverage regardless.

Do subcontractors need their own insurance, or does the general contractor's policy cover them?

Subcontractors need their own policies — most general contractors require proof of coverage (general liability, workers' comp, and commercial auto) before hiring subs. A GC's policy typically won't cover subcontractor-caused incidents, leaving both parties exposed without separate coverage.

Can I bundle multiple construction insurance policies together?

Many insurers offer Business Owner's Policies (BOPs) that bundle general liability, commercial property, and business interruption coverage. Workers' comp, commercial auto, builder's risk, and inland marine are typically purchased separately. A broker who works with multiple carriers can help package these into a cost-effective program.