Introduction

Managing a large construction project means juggling dozens of contractors, each carrying their own insurance — a patchwork that leaves gaps, creates disputes, and wastes time. When a claim arises, determining which contractor's policy responds becomes a legal maze. Multiple insurers point fingers at each other while the project stalls and legal fees mount. Coverage limits vary wildly across subcontractors, leaving owners and general contractors exposed when an underinsured party causes a major incident.

Wrap-up insurance solves this by consolidating coverage under a single policy for everyone on the project. Instead of tracking certificates from 50 different subcontractors, one unified program covers all parties — cutting gaps, simplifying claims, and often lowering total insurance costs. What follows covers the two main types (OCIP and CCIP), what's included, the trade-offs, and how to get coverage in place.

Key Takeaways

- Wrap-up insurance consolidates liability, workers' comp, and builder's risk coverage for all contractors and subcontractors under one project-specific program

- Owner Controlled (OCIP) programs are sponsored by the project owner; Contractor Controlled (CCIP) programs are managed by the general contractor

- Coverage typically includes general liability, workers' compensation, builder's risk, and umbrella/excess liability — commercial auto is not covered

- Cost savings average 20% or more, with fewer coverage disputes and higher policy limits than individual contractor plans

- Best suited for projects valued at $10 million or more due to administrative complexity and setup costs

What Is Wrap-Up Insurance?

Wrap-up insurance is a centralized, project-specific solution that covers all major parties on a construction project — owners, general contractors, and subcontractors — under one coordinated program instead of each carrying separate policies. The "wrap-up" name reflects how a single sponsor manages coverage for everyone on-site, with unified terms and limits across the board.

When wrap-up insurance is used:

Wrap-up programs are typically deployed on large-scale construction projects. While historically reserved for projects valued at $100 million or more, the market has evolved significantly. General liability-only wrap-ups are now viable for projects as small as $10 million for residential developments or $25 million for commercial projects. Full wrap-up programs including workers' compensation remain most common on projects exceeding $100 million in hard construction costs.

Why the traditional model fails:

When each contractor carries separate coverage, several problems emerge:

- Coverage gaps leave owners exposed when an incident falls into a gray area between two insurers

- Overlapping limits waste premium dollars on redundant coverage

- Carrier disputes stall claims resolution as multiple insurers argue over which policy responds

- Tracking dozens of certificates of insurance adds administrative overhead throughout the project lifecycle

A wrap-up program replaces that fragmented approach with one master policy — one set of terms, one claims process, and one point of accountability for the entire project.

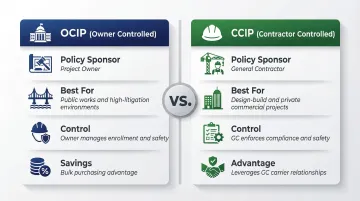

Types of Wrap-Up Insurance: OCIP vs. CCIP

Owner Controlled Insurance Program (OCIP)

An OCIP is a wrap-up program where the project owner purchases and administers a single consolidated insurance policy on behalf of all enrolled contractors and subcontractors.

The owner acts as policy sponsor, with direct control over coverage terms, carrier selection, safety programs, and claims management.

Why owners choose OCIPs:

- Cost efficiency — Bulk purchasing across all trades delivers better rates than individual contractors could obtain. Owners can save a minimum of 20% on insurance costs compared to contractors arranging separate policies and adding profit/administration markups

- Uniform coverage — Eliminates gaps and disputes between contractors' individual policies by establishing consistent terms and limits for all enrolled parties

- Direct safety oversight — The owner controls jobsite safety standards and monitors loss experience directly, rather than relying on subcontractors' varying safety cultures

- Centralized claims — All incidents are reported through one administrator and one insurer, simplifying investigations and resolutions

Contractors reduce or exclude their own insurance costs from bids, and the owner recoups those savings through the consolidated program.

That model works well when the owner wants full oversight — but when a general contractor has strong carrier relationships and a proven safety record, a CCIP often makes more sense.

Contractor Controlled Insurance Program (CCIP)

A CCIP is a wrap-up program managed by the general contractor rather than the owner. The general contractor purchases and administers the policy, which extends coverage to enrolled subcontractors throughout the project. This gives the GC direct control over subcontractor compliance, safety requirements, and claims outcomes.

Why general contractors prefer CCIPs:

- Trade-level enforcement — The GC controls jobsite behavior and enforces safety protocols across all trades, reducing incidents and improving loss experience

- Competitive advantage — Including the CCIP in bids reduces friction with subcontractors, who benefit from not having to arrange their own coverage

- Favorable underwriting terms — GCs can leverage their own claims history and carrier relationships to negotiate better premiums and higher limits than an owner-arranged policy might secure

- Rolling program efficiency — Experienced GCs can establish ongoing CCIP relationships with carriers, reducing setup time across future projects

The CCIP market has grown significantly. Fifteen years ago, CCIPs represented just 5-8% of wrap-up programs, but the split is now roughly 50-50 with OCIPs, driven by general contractors' safety expertise and the efficiency of rolling programs across multiple projects.

OCIP vs. CCIP comparison:

| Factor | OCIP | CCIP |

|---|---|---|

| Policy Sponsor | Project owner | General contractor |

| Who Benefits Most | Owners seeking cost control and direct oversight | GCs with strong safety records and carrier relationships |

| Best For | Public works, multi-contractor developments, high-litigation environments | Design-build projects, private commercial developments, experienced GCs |

| Administrative Control | Owner manages enrollment and compliance | GC manages enrollment and compliance |

A third option — a Partner-Controlled Insurance Program (PCIP) — exists where an owner and general contractor jointly purchase the program and share its benefits and responsibilities.

What Does Wrap-Up Insurance Cover?

Coverage included in a wrap-up policy varies by program design, but most OCIPs and CCIPs include four core coverages:

1. Commercial General Liability (CGL)

Covers third-party bodily injury and property damage claims arising from construction activities on the site. If a falling tool injures a pedestrian or construction equipment damages an adjacent building, the CGL policy responds.

2. Workers' Compensation

Provides coverage for all enrolled contractors' and subcontractors' employees injured on the job site, eliminating the need for each firm to carry separate workers' comp policies. This consolidation ensures uniform coverage and simplifies claims administration.

3. Builder's Risk Insurance

Covers physical damage to the structure under construction — and often materials on-site — caused by fire, weather, vandalism, and similar perils. Builder's risk protects the project property itself, not third-party claims. Note that some projects carry a standalone builder's risk policy alongside the wrap-up rather than bundling it into the program.

4. Umbrella/Excess Liability

Provides an additional layer of coverage above the limits of the underlying general liability policy. This is especially important on high-value projects where a single incident could exhaust primary limits. For example, if the GL covers $2 million and the umbrella provides $10 million, a $7 million claim would be covered across both layers.

Optional Add-On Coverages

Depending on project complexity, wrap-up programs can include:

- Professional Liability: Covers design-build projects where architect or engineer errors could trigger claims

- Pollution Liability: Applies to brownfield redevelopment, industrial construction, or any project with significant environmental exposure

- Railroad Protective Liability: Required when construction activities occur near active rail lines and could interfere with rail operations

Commercial auto insurance is universally excluded from wrap-ups. Vehicles regularly leave construction sites, making it difficult to verify whether damage occurred on-site or off-site, and vehicle ownership varies widely among subcontractors. Every enrolled contractor must maintain separate commercial auto coverage, which requires manual tracking by the program administrator.

What's Excluded

Wrap-up policies typically exclude:

- Off-site work: Fabrication shops, material storage yards, and work performed away from the project site — unless specifically endorsed

- Post-completion claims: Coverage ends when construction finishes unless you purchase a completed operations extension

- Professional design errors: Not covered under standard CGL; requires a separate professional liability add-on

These exclusions catch contractors off guard most often — particularly off-site fabrication work and post-completion defect claims. Confirm with your broker which gaps apply to your specific project before finalizing the program structure.

Key Benefits of Wrap-Up Insurance

Elimination of Coverage Gaps and Disputes

Because all parties are enrolled under one policy with uniform terms, there are no conflicts between contractors' individual policies about which insurer is responsible for a claim. No risk exists that an uninsured or underinsured subcontractor leaves the owner or GC exposed to liability.

Consolidating coverage under one master policy eliminates the costs of overlapping coverage and delays caused by coverage disputes or "finger-pointing" between multiple insurance carriers.

Cost Savings

Those same consolidation advantages translate directly into cost savings. The policy sponsor negotiates more favorable rates than any individual contractor could secure on their own. Contractors typically reduce their insurance costs — and therefore their bids — frequently offsetting much of the wrap-up program's cost. Owners can save a minimum of 20% on insurance costs by taking an OCIP approach compared to contractors arranging insurance and adding profit/administration markups.

Streamlined Claims Management

A single policy means all claims from the project go through one administrator and one insurer, leading to:

- Faster reporting and investigation

- More consistent claim handling

- Efficient resolution without multi-party legal disputes

- Lower administrative costs compared to coordinating multiple insurers

Higher and More Consistent Coverage Limits

Because the policy is project-specific and purpose-built, insurers can tailor aggregate limits to the project's actual value — not the caps on each subcontractor's individual policy. Two additional advantages follow from this structure:

- Higher limits: Coverage scales to the project, not to the smallest contractor's policy ceiling

- Reduced admin load: GCs shed the burden of collecting and tracking certificates of insurance for every enrolled subcontractor

Limitations and Challenges to Consider

Complexity and Administrative Demands

Setting up and managing a wrap-up program requires significant coordination among the project owner, general contractor, subcontractors, and insurance administrators:

- Enrollment management — Each contractor must be properly enrolled, with contract language aligned to program requirements

- Payroll reporting — Ongoing compliance reporting is required throughout the project

- Unenrolled contractor risk — Poorly administered programs can leave subcontractors working without coverage, creating serious exposure

Cost and Project Size Considerations

Wrap-up programs involve substantial upfront setup costs and administrative fees, which means they typically only generate net savings on projects above a certain value threshold. General liability-only CIPs are generally used on projects with hard construction costs of $25 million or more, while programs including workers' compensation are most common on projects of at least $100 million.

For smaller projects, the costs of program setup and administration often outweigh the benefits, making traditional individual policies more practical.

Common Exclusions and Jurisdictional Restrictions

- Professional liability and design errors are usually excluded unless specifically added

- Off-site work is typically not covered

- Completed operations coverage (protecting against claims that arise after the project is finished) may require a separate endorsement

New York's Scaffold Law (Labor Law 240/241) imposes absolute liability on owners and general contractors for gravity-related injuries, regardless of worker fault. The result: insurance costs reach 8-10% of total development costs, roughly 2x-5x higher than comparable states.

Consequently, primary GL deductibles in New York have climbed to $1 million-$5 million per occurrence, and excess liability capacity has shrunk significantly.

New York is an extreme case, but other jurisdictions impose their own regulatory restrictions on wrap-up programs, particularly for public projects. Reviewing state statutes before structuring a CIP can prevent costly compliance gaps down the line.

How to Get Wrap-Up Insurance for Your Project

Step 1: Project Evaluation

Begin by assessing whether a wrap-up program is appropriate:

- Project scope and value — Is the total construction value at least $10 million (residential) or $25 million (commercial)?

- Timeline — Does the project duration justify the setup and administration costs?

- Number of contractors — Are multiple trades and subcontractors involved?

- Risk profile — Are there complex exposures that benefit from unified coverage?

Determine which type (OCIP or CCIP) fits best based on who will sponsor the program and who has the strongest carrier relationships.

Step 2: Engage Insurance Providers and Contractors Early

Hold pre-bid meetings to:

- Set expectations with all contractors about the wrap-up program

- Outline the enrollment process and compliance requirements

- Surface any coverage challenges before construction begins

- Clarify the insurance credit methodology (how contractors will reduce their bids to reflect insurance savings)

Contractors must submit an Insurance Cost Worksheet (ICW) to document the insurance costs removed from their bids.

Step 3: Select the Right Broker or Administrator

Working with a broker who specializes in construction and complex commercial insurance is critical. Look for brokers with the Construction Risk and Insurance Specialist (CRIS) certification, which certifies knowledge of construction insurance and risk management.

The right broker will:

- Structure the program to match your project's risk profile

- Negotiate terms and limits with carriers

- Manage subcontractor enrollment and compliance

- Provide ongoing oversight throughout the project lifecycle

Soma's construction specialists place wrap-up coverage through carriers like Chubb, Liberty Mutual, and Kinsale, structuring programs that satisfy lender, owner, and contract requirements for large-scale, multi-trade developments.

Step 4: Plan for Completed Operations Coverage

A good broker will flag this during Step 3: once construction ends, your wrap-up program needs to transition to ongoing operations coverage. Completed operations liability — covering claims arising from defects in finished work — should be built into the program design from the start to avoid a lapse in protection once the project closes out. Tail coverage periods typically extend through the applicable state statute of repose, often up to 10 years after substantial completion.

Frequently Asked Questions

What does "wrap up" mean in insurance?

"Wrap up" refers to the consolidation — or "wrapping up" — of multiple insurance coverages and multiple parties (owners, contractors, subcontractors) into a single, unified project-specific policy, eliminating the need for each party to carry separate individual policies.

How does wrap up insurance work?

One party — the owner in an OCIP or the general contractor in a CCIP — purchases a master policy covering all enrolled contractors and subcontractors. Enrolled contractors reduce their bids to reflect removed insurance costs, and all claims run through the single centralized program.

What does wrap insurance cover?

Wrap-up insurance typically covers general liability, workers' compensation, builder's risk, and umbrella/excess liability, with optional add-ons like professional liability or pollution liability. It excludes off-site work and usually commercial auto.

Who pays for wrap-up insurance?

In an OCIP, the project owner pays; in a CCIP, the general contractor pays. Either way, contractors reduce their bids to reflect the insurance costs they no longer carry, so the economic burden is shared across the project.

What is the difference between OCIP and wrap?

Wrap-up insurance is the broad category, while OCIP is a specific type where the project owner purchases and controls the program. A CCIP follows the same structure, but the general contractor serves as sponsor and administrator instead.

What is construction wrap up insurance?

Construction wrap-up insurance is a project-specific program built for construction jobs — usually those valued at $10 million or more — bundling general liability, workers' comp, and builder's risk into one policy that covers all parties on the job site.