Introduction

A delivery driver in a company van runs a red light and crashes into another vehicle, sending two people to the hospital. The business owner assumes their personal auto insurance will cover it—until the claim is denied. Personal auto policies explicitly exclude business use, leaving the owner facing a $300,000 lawsuit with no coverage.

Commercial auto insurance is a policy designed to protect businesses from financial loss when a company-owned, leased, or rented vehicle is involved in an accident. It covers property damage, medical expenses, and liability arising from business vehicle use—exposures that personal auto policies won't touch.

This guide covers what commercial auto insurance includes, how it differs from personal coverage, who needs it, and what to look for when choosing a policy—so you can protect your business before a claim forces the issue.

Key Takeaways

- Commercial auto insurance covers liability, physical damage, and medical costs for business vehicles—personal policies exclude business use

- Most businesses need it if vehicles are owned by the company, used for deliveries, or driven by employees for work

- Policies typically use Combined Single Limits (CSL) of $500,000 to $1,000,000, far exceeding personal auto minimums

- Median cost is around $245 per month, varying by industry, fleet size, and driver records

- One application through a commercial broker can return quotes from multiple carriers—useful for complex fleets or hard-to-place risks

What Does Commercial Auto Insurance Cover?

Commercial auto policies bundle several coverage types, allowing businesses to select what fits their operations. Most states legally require bodily injury and property damage liability at minimum for commercial vehicles.

Liability Coverages

Bodily Injury Liability pays medical costs, lost wages, and legal fees when your driver injures someone else in an at-fault accident. Property Damage Liability covers repairs or replacement of others' property: vehicles, buildings, fences, or equipment.

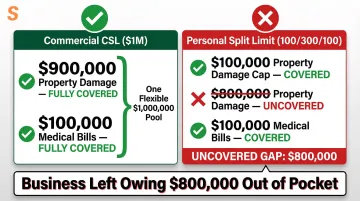

These are foundational coverages required in most states. Commercial policies often use a Combined Single Limit (CSL), which pools bodily injury and property damage into one maximum payout per accident. A $1,000,000 CSL can be applied flexibly: if property damage is $800,000 and injuries are $200,000, the entire limit covers both.

Personal policies, by contrast, use split limits (for example, 250/500/100), which cap each category separately. That structure can leave you exposed if one category exhausts its limit before the other is fully covered.

Physical Damage Coverages

Collision Coverage pays to repair your own vehicle after hitting another object or rolling over, minus your deductible. Comprehensive Coverage handles non-collision damage: theft, fire, vandalism, hail, or flooding.

Both typically require a deductible ranging from $500 to $2,500. Higher deductibles lower premiums but increase out-of-pocket costs when filing a claim.

Additional Coverages

Once liability and physical damage are in place, supplemental coverages close the remaining gaps:

- Medical Payments / Personal Injury Protection (PIP) covers medical bills and lost wages for your driver and passengers, regardless of fault

- Uninsured/Underinsured Motorist (UM/UIM) reimburses you when hit by a driver with not enough or no insurance

- Hired and Non-Owned Auto (HNOA) covers liability when employees use personal or rented vehicles for business errands, acting as excess coverage over their personal policies

What Commercial Auto Insurance Does NOT Cover

Just as important as knowing what's covered is knowing what isn't:

- Cargo or contents inside the vehicle requires separate Inland Marine or Cargo insurance

- Employee injuries during work are covered by Workers' Compensation, not commercial auto

- Personal use accidents: if an employee uses a company vehicle for personal errands without permission, the claim may be denied

- Rental vehicle physical damage: HNOA covers liability only, not damage to the rental itself

Commercial Auto vs. Personal Auto Insurance: Key Differences

While the terminology overlaps, commercial and personal auto policies serve fundamentally different purposes. Personal auto insurers often deny claims outright when a vehicle is used for business, leaving owners financially exposed.

Coverage Limits and Structure

Commercial policies carry much higher liability limits to account for greater business risk. Personal policies typically use split limits (e.g., 250/500/100), which divide coverage into three caps:

- $250,000 bodily injury per person

- $500,000 bodily injury per accident

- $100,000 property damage per accident

Commercial policies commonly use a Combined Single Limit (CSL) of $500,000 to $1,000,000 or more — a single pooled amount covering any combination of bodily injury and property damage in one incident.

The difference matters in real claims. If a crash causes $900,000 in property damage and $100,000 in medical bills, a $1,000,000 CSL covers both. A split limit policy would cap property damage at $100,000, leaving the business on the hook for the remaining $800,000.

Number of Drivers and Vehicles

Personal policies cover a primary driver and household members across a limited number of vehicles. Commercial policies scale to cover entire fleets—dozens of vehicles and drivers, including employees who only drive occasionally for work.

How Policies Are Written and Rated

Commercial underwriters assess business-specific risk factors that don't apply to personal auto:

- How vehicles are used (hauling, transporting people, delivery)

- Vehicle weight and type (box trucks, tractor-trailers)

- Driver records across multiple employees

- Garaging location and annual mileage

- Industry risk profile (construction, trucking, food service)

Personal auto underwriting focuses on individual driver history, commute distance, and household composition.

When Personal Insurance Falls Short

A contractor uses his personal pickup truck to haul tools and materials to a job site. On the way, he rear-ends another vehicle, causing $75,000 in damage and $50,000 in medical bills. His personal auto insurer denies the claim, citing the business-use exclusion in the policy. The contractor is now personally liable for $125,000 out of pocket — with no coverage to fall back on.

Who Needs Commercial Auto Insurance?

General rule: If a vehicle is owned, leased, or rented by a business—or if employees drive any vehicle for work purposes beyond commuting—commercial auto insurance is likely needed and may be legally required. Requirements vary by state and vehicle type.

Businesses That Commonly Require It

Industries that typically need commercial auto coverage include:

- Contractors and construction firms hauling tools, equipment, and materials on job sites

- Trucking and logistics companies running box trucks, tractor-trailers, or delivery fleets

- Landscapers whose crews transport mowers, trimmers, and supplies between sites

- Caterers and food service businesses delivering meals or operating food trucks

- Retail delivery operations bringing products directly to customers

- Healthcare providers with mobile staff or ambulance services

- Hospitality businesses operating courtesy shuttles or passenger vans

Signs You May Need Commercial Auto Instead of Personal

You likely need commercial auto if any of these apply:

- Vehicles are registered or titled in a business name

- Employees drive company vehicles regularly

- You transport goods or people for a fee

- You haul tools or equipment as part of business operations

- Vehicles exceed weight or size limits for personal auto policies (typically over 10,000 lbs)

State and Contractual Requirements

Many states mandate minimum commercial auto liability coverage for business vehicles. For example:

- California requires 15/30/5 split limits

- New York requires 25/50/10

- Texas requires 30/60/25

State minimums are a floor, not a ceiling. Many client contracts and government projects require $1,000,000 Combined Single Limits before awarding work—so verify both state requirements and contract terms when selecting your coverage limits.

Types of Vehicles Covered by Commercial Auto Insurance

Commercial auto insurance covers a broad range of vehicles beyond standard company cars:

- Box trucks and cargo vans

- Service utility trucks and work pickup trucks

- Food trucks and delivery vehicles

- Dump trucks and tractor-trailers

- Specialty vehicles (with endorsements for hazmat or passenger transport)

Hired and Non-Owned Auto (HNOA)

HNOA extends coverage to vehicles the business doesn't own. If an employee uses their personal car for a business errand or the company rents a vehicle temporarily, HNOA provides liability coverage. It acts as excess coverage over the employee's personal policy but does not cover physical damage to the employee's or rented vehicle.

Fleet Coverage

Fleet coverage is designed for businesses with multiple vehicles—typically five or more. Fleet policies simplify administration by consolidating all vehicles under one policy, often at a lower cost than insuring each vehicle individually. They also allow flexible driver assignments, covering "any driver" or assigning specific drivers to specific vehicles.

How Much Does Commercial Auto Insurance Cost?

Commercial auto insurance typically costs more than personal auto coverage due to higher risk exposure and broader limits. According to Insureon's 2026 data, the median cost for small businesses is $245 per month, with annual premiums ranging from under $375 to over $16,000 depending on operations.

Key Factors That Affect Premiums

Insurers calculate premiums based on several risk factors:

- Type and number of vehicles: Heavy-duty trucks and specialized vehicles cost more than sedans

- How vehicles are used: Delivery, passenger transport, and heavy cargo hauling increase risk

- Annual mileage: Higher mileage means more exposure to accidents

- Garaging location: Urban areas with heavy traffic or high crime rates increase premiums

- Driver records: Accidents, violations, and inexperienced drivers raise costs

- Coverage limits selected: Higher CSLs and lower deductibles increase premiums

Industry type drives some of the widest cost gaps. Insureon's data shows:

- Nonprofit organizations: $168/month

- Real estate businesses: $192/month

- Construction contractors: $264/month

- Installation contractors: $299/month

- For-hire transport trucks: $954/month

Ways to Reduce Commercial Auto Insurance Costs

If your premiums land on the higher end, several strategies can bring them down:

- Maintain clean driver records: Implement formal hiring policies and conduct annual MVR (Motor Vehicle Record) reviews

- Install telematics and dashcams: Monitor speeding, harsh braking, and distracted driving. Samsara's 2025 Safety Report found that fleets using AI dashcams and in-cab coaching achieved a 73% reduction in crash rates over 30 months

- Choose higher deductibles: Accepting a $1,000–$2,500 deductible lowers premiums — keep sufficient reserves to cover the out-of-pocket gap

- Store vehicles securely: Garaging vehicles in secure lots reduces theft and vandalism risk

- Bundle policies: Combining commercial auto with General Liability or a Business Owner's Policy (BOP) often yields discounts

- Work with a specialized broker: Brokers with access to multiple carriers can find more competitive rates by shopping your risk across dozens of insurers

How to Get the Right Commercial Auto Coverage for Your Business

Prepare for a quote by gathering the following information:

- Vehicle details (make, model, year, VIN)

- List of all drivers with license numbers and driving records

- How vehicles are used (delivery, passenger transport, hauling)

- Minimum state-required liability limits

- Annual mileage estimates

Once you have this information ready, a specialized broker can move quickly. Coverage requirements vary significantly across industries — a trucking operation needs very different limits and endorsements than a construction fleet or a hospitality shuttle service. Working with a broker who understands your industry helps match your business to the right carrier and structure from the start.

Soma works with hundreds of carrier partners — including Chubb, Liberty Mutual, Markel, and Nationwide — and specializes in placing coverage for complex and hard-to-insure businesses. A single application is typically all it takes to turn around quotes.

Review your policy whenever your operations change. Common triggers include:

- Adding new vehicles to your fleet

- Hiring additional drivers or changing driver roles

- Expanding into new states with different liability minimums

- Shifting how vehicles are used (for example, adding delivery runs to a previously passenger-only fleet)

Frequently Asked Questions

What is the difference between commercial and regular auto insurance?

Personal auto insurance covers vehicles used for personal purposes and excludes business use. Commercial auto insurance is designed for vehicles used in business operations, offering higher limits, broader driver coverage, and business-specific protections.

Can you use personal insurance for a commercial vehicle?

No. Personal auto policies typically exclude business use, meaning claims can be denied if the vehicle was being used commercially at the time of the accident. Without a commercial policy in place, a denied claim leaves your business absorbing the full cost of damages or injuries.

What does a commercial auto insurance policy cover?

Core coverages include bodily injury and property damage liability, collision, comprehensive, medical payments, uninsured/underinsured motorist, and hired/non-owned auto coverage. Additional endorsements may be required for specialty operations.

Who is insured under a commercial auto policy?

The named insured (typically the business) and any employees with a valid license who are authorized to drive covered vehicles are insured. Family members not employed by the business are generally not covered unless given explicit permission.

How long do commercial auto insurance policies last?

Commercial auto policies are typically offered in 6-month or 12-month terms. Most carriers default to 12-month terms, though 6-month options are more common for higher-risk fleets.

Do I need an LLC for commercial auto insurance?

No, an LLC is not required for commercial auto insurance. Sole proprietors and other business structures can also qualify. The key factor is how the vehicle is used, not the legal structure of the business.