Key Takeaways

- New construction requires two insurance phases: builder's risk during construction and standard homeowners insurance after move-in

- New builds cost 42% less to insure than older homes due to modern materials and updated building codes

- The biggest risk is a coverage gap during handoff — confirm your homeowners policy activates on closing day, not after

- Bundling, safety devices, and new construction discounts can cut annual premiums by 10–25%

Understanding the Two Phases of New Construction Insurance

Insuring a new construction home isn't a single event—it's a two-phase process. During the construction phase, builder's risk insurance protects the structure and materials. After move-in, standard homeowners insurance takes over. Understanding both phases and managing the handoff correctly is critical.

The type of insurance required depends on who is building:

- Licensed contractor builds: The contractor typically carries builder's risk coverage during construction

- Owner-builder or spec home purchase: You may need to secure your own builder's risk policy

The most critical rule is the "no-gap" principle: the moment one policy ends, another must begin. Even a single day without coverage exposes you to serious uninsured losses with no recourse.

Two specific clauses make this gap dangerous. Standard homeowners policies include "vacancy clauses" that void coverage for vandalism, glass breakage, and water damage if a home sits unoccupied for 30 to 60 consecutive days. On the other side, builder's risk policies automatically terminate the moment you move in — regardless of whether the official policy end date has passed.

Builder's Risk Insurance: Protecting Your Home During Construction

Builder's risk insurance (also called "course of construction insurance") is a temporary property policy that protects the physical structure while it's being built. It covers the building itself, on-site materials, and sometimes equipment.

What Builder's Risk Covers

Typical covered perils include:

- Fire, lightning, wind, and hail

- Theft of building materials

- Vandalism and explosions

- Accidental damage to the structure

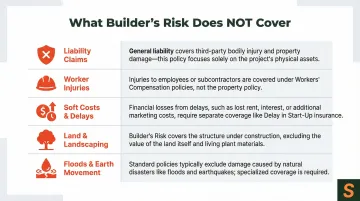

Builder's risk is strictly a property policy — the table below outlines what falls outside its scope and why each gap matters.

What Builder's Risk Does NOT Cover

| Excluded | Why It Matters |

|---|---|

| Personal liability | Requires contractor's general liability policy |

| Worker injuries | Requires workers' compensation coverage |

| Soft costs (loan interest, permits, architectural fees) | Must be added via endorsement |

| Land, landscaping, existing structures | Property policy exclusions |

| Floods, earth movement, mechanical breakdowns | Standard perils exclusions |

Who Carries the Policy?

In most cases, the general contractor carries builder's risk insurance. Before work begins, take these steps:

- Verify coverage with your contractor

- Confirm policy limits match your project value

- Request a certificate of insurance

- If the contractor's coverage is insufficient, purchase your own policy

Dwelling Under Construction Endorsement vs. Standalone Policy

For smaller projects (under 6 months), a "dwelling under construction" endorsement on an existing homeowners policy is usually enough. For major builds or long-term renovations, a **standalone builder's risk policy** is recommended.

Homeowners Insurance for New Builds: What You Need After Move-In

Once the builder's risk policy ends — typically when the home is complete and ready for occupancy — a standard homeowners insurance policy must be in place. Schedule it to begin the exact day the construction policy expires, with no gap between the two.

The Six Standard Coverages (A–F)

Standard homeowners policies include six coverage types:

- Coverage A (Dwelling): Protects the structure itself. For new builds, insure at full replacement cost — not market value — to account for current construction costs.

- Coverage B (Other Structures): Covers detached garages, fences, and sheds if your new build includes them.

- Coverage C (Personal Property): Covers furniture, electronics, and belongings — especially relevant when moving expensive items into a brand-new home.

- Coverage D (Additional Living Expenses): Pays for temporary housing if the home becomes uninhabitable after a covered event.

- Coverage E (Liability): Covers injuries or property damage you're legally responsible for, including incidents involving guests.

- Coverage F (Medical Payments): Pays for minor guest injuries regardless of fault.

HO-3 vs. HO-5: Choosing the Right Policy

| Feature | HO-3 (Special Form) | HO-5 (Comprehensive Form) |

|---|---|---|

| Dwelling Coverage | Open perils (all risks unless excluded) | Open perils |

| Personal Property | Named perils (only listed risks covered) | Open perils (all risks unless excluded) |

| Claim Settlement | Actual cash value (depreciated) | Replacement cost (full value) |

| Best For | Budget-conscious homeowners | New or high-value homes |

For new builds, an HO-5 policy is the stronger choice. It covers personal property against accidental damage — like spilling paint on an expensive rug — that an HO-3 policy would deny.

The 80% Rule: Avoiding Coinsurance Penalties

Insurers typically require dwelling coverage equal to at least 80% of your home's full replacement cost. Falling below this threshold results in partial claim payments — even for covered losses.

Example: Your home's replacement cost is $500,000. You must carry at least $400,000 in coverage (80%). If you only carry $395,000 — 98.75% of the required minimum — a $250,000 fire claim would only pay $246,875, leaving you $3,125 short.

For new builds: Set coverage limits based on current construction costs, not purchase price or market value. Land value doesn't factor into replacement cost.

Insurance Binders: Bridging the Gap

If there's a potential gap between the builder's policy ending and your homeowners policy starting, a temporary insurance binder provides short-term coverage (typically 30 to 90 days) while the full policy is finalized. Lenders require proof of insurance before closing, and binders satisfy this requirement.

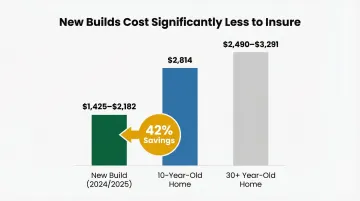

How Much Does New Construction Insurance Cost?

New construction homes are significantly cheaper to insure than older homes. Modern materials, updated electrical and plumbing systems, and current building code compliance all reduce the likelihood of claims.

Average annual premiums:

- New build (2024/2025): $1,425 to $2,182

- 10-year-old home: $2,814

- 30+ year-old home: $2,490 to $3,291

This represents a 42% savings compared to older homes.

Factors That Determine Your Premium

Several variables shape what you'll pay:

- Flood zones, hurricane belts, and wildfire areas increase premiums; building code requirements also vary by region

- Square footage, construction materials, and dwelling coverage limit all affect the base rate

- Your chosen deductible directly impacts the premium — higher deductibles lower monthly costs

- Credit history (where applicable) and prior claims history factor into final pricing

Builder's Risk Insurance Costs

If you're covering an active build rather than a finished home, the cost structure is different. Builder's risk insurance is priced at 1% to 5% of total construction value annually.

Example: For a $400,000 build:

- Low end (1%): $4,000 annually

- High end (5%): $20,000 annually

Wood-frame construction in hurricane-prone coastal areas pushes premiums toward 5%. Inland projects in mild climates fall closer to 1%.

How to Save on New Construction Homeowners Insurance

Top Discounts for New Builds

New construction homes qualify for some of the best rates available. Common discounts include:

- New construction: Homes built within the last 10 years qualify for one of the largest available discounts

- Bundling home and auto: Average savings of 14% ($466/year); some carriers offer up to 23%

- Claims-free history: Stay loss-free for 3 to 5 years to earn additional premium reductions

- Safety devices (5%–20% off): Smart smoke detectors, security systems, water leak sensors, and deadbolt locks each typically qualify

Shop Around: Rates Vary by Over $1,000

Premium rates for identical coverage can differ by $1,000 or more between carriers — even for the same new build in the same zip code. That gap is entirely avoidable with the right comparison process.

Working with an independent broker who accesses multiple carriers lets you compare rates, coverage terms, and exclusions in a single submission rather than applying separately to each insurer.

Review Coverage Limits at Key Milestones

Getting the right rate at purchase is only half the job. Construction costs and home values shift over time, so your limits need to keep pace. Review your coverage:

- When the home is completed

- At move-in

- Annually thereafter

A key check: confirm your dwelling limit reflects replacement cost — what it costs to rebuild — not market value, which can be significantly lower.

Frequently Asked Questions

Frequently Asked Questions

How much is new construction insurance?

Builder's risk insurance during construction costs 1% to 5% of total build value. Homeowners insurance for a completed new build averages $1,425 to $2,182 annually, which is 42% less than for older homes due to modern materials and updated systems.

Can you get insurance on a new build?

Yes, new builds are insurable in both phases: during construction via builder's risk insurance, and after completion via standard homeowners insurance. New builds typically qualify for lower rates because modern materials, updated electrical and plumbing systems, and current building code compliance all reduce damage risk.

What is insurance on a new building during its construction?

This is builder's risk insurance (also called course of construction insurance). It's a temporary policy covering the structure and building materials against fire, theft, vandalism, and weather damage while the home is under construction.

Is builders risk insurance worth it?

Yes, builder's risk insurance is worth it for owner-builders or when the contractor's policy has coverage gaps. Without it, losses from fire, theft, or weather during construction come entirely out of pocket, which can reach hundreds of thousands of dollars on a single incident.

Is homeowners insurance cheaper on new construction?

New homes are generally cheaper to insure. The same factors that make them safer to build—modern materials, updated systems, current code compliance—translate directly into lower premiums. A comparable 30-year-old home averages $2,490 annually versus $1,425 for a new build.

What is the 80% rule for homeowners insurance?

The 80% rule requires homeowners to carry dwelling coverage of at least 80% of the home's full replacement cost to receive full claim payouts. For new construction, set coverage limits based on current construction costs, not purchase price or market value.