Introduction

Searching for "one-week truck insurance" usually means something urgent is happening — you just bought a truck at auction, need to move an empty rig between terminals, or your annual policy lapsed and you have a repair trip scheduled tomorrow. Getting the coverage wrong in any of these situations doesn't just mean a denied claim. It means personal liability exposure on a commercial vehicle, potential CDL suspension, and fines that can exceed $21,000 per day of violation.

True 7-day commercial truck policies don't exist as a standard market product. Most temporary truck insurance caps at 5 consecutive days, with a 30-day pro-rated binder as the next available option. Both are strictly non-hauling — add commercial cargo and the coverage is void.

What follows covers the actual policy structures available, realistic cost ranges by situation, and which option fits your specific need.

Key Takeaways

- Short-term truck policies cap at 5 consecutive days, not 7

- Specialty providers publish rates from $140 for 24 hours up to $540 for 5 days

- Commercial cargo hauling is strictly prohibited under any temporary policy

- Need a full week? A 30-day pro-rated binder is the only compliant path

- These policies cover empty-truck moves, not revenue-generating operations

How Much Does One-Week Truck Insurance Cost?

Here's the pricing reality: one-week truck insurance doesn't exist as a single policy. Underwriters cap short-term commercial truck programs at 5 consecutive days. If you need coverage for 7 full days, a pro-rated 30-day binder is your only compliant option.

This distinction matters because drivers who misunderstand it end up assuming they can haul cargo under a "temporary" policy, or they end up with a 2-day uninsured gap when a 5-day policy expires mid-trip.

Typical Cost Ranges

NITIC, a specialty commercial truck risk retention group, publishes the clearest public price schedule for short-term truck policies. These are provider-specific figures for non-hauling transit coverage:

| Duration | Published Price |

|---|---|

| 24 hours | $140 |

| 48 hours | $240 |

| 72 hours | $340 |

| 96 hours | $440 |

| 5 days | $540 |

A few things to note about this pricing:

- These rates are for high-risk, non-hauling transit — moving a purchased truck home or taking it for repairs

- You can typically add physical damage coverage as an optional layer, which increases the daily rate

- Market averages will vary; these represent one specialty provider's published schedule

Best use cases by duration:

- 24 hours — Auction pickup, single-day transit to a repair shop

- 2–5 days — Out-of-state transport, terminal relocation, extended repair trip

The 30-Day Binder Option

If you genuinely need 7+ days of coverage, a pro-rated 30-day commercial binder is what you need. Key facts to know before going this route:

- No published pricing — cost varies by truck class, driver history, liability limits, and cargo type

- Short-rate penalty applies if you cancel early; you may not recover the full unused premium

- Required for cargo hauling — the 5-day temporary product explicitly prohibits commercial loads

Soma works with specialty trucking markets across both tiers — short-term transit policies and 30-day binders — and can issue a fast COI for owner-operators who need proof of coverage before a move.

Key Factors That Affect One-Week Truck Insurance Costs

Temporary truck insurance costs more per day than an annual policy pro-rated to the same period. Underwriters have far less premium to absorb potential losses over seven days, so they price conservatively from the start. Several variables drive exactly where your quote lands.

Truck Type and Weight Class

Vehicle classification is one of the first things underwriters evaluate. A Class 6 box truck or hotshot pickup is generally easier and cheaper to place on a short-term basis than a Class 8 tractor-trailer combination.

Heavy combination vehicles carry higher loss severity, more complex liability exposure, and tighter underwriting appetite — all of which push premiums up and reduce the number of available programs.

Driver History and CDL Status

Short-term policies get closer scrutiny on MVR (Motor Vehicle Record) because the carrier earns less premium over the policy period. AmTrust's small-fleet program, for example, permits up to four minor violations or two minor violations plus one accident in the prior 36 months — but disqualifies drivers with DUI, reckless driving, felony, or license suspension in the prior five years. These thresholds vary by carrier, but the direction is consistent: recent major violations either disqualify drivers entirely or significantly raise rates.

Coverage Limits and Add-Ons

The federal minimum for interstate for-hire general freight over 10,001 lbs is $750,000 under 49 CFR § 387.9. Many freight brokers require $1 million CSL — C.H. Robinson, for instance, requires at least $1 million automobile liability from carriers on their network. Carrying only $750K can disqualify you from broker networks that mandate $1M, which directly limits which loads you can accept.

Optional add-ons that increase the daily rate:

- Physical damage (collision and comprehensive) — often required by lenders on financed trucks

- Cargo coverage — typically unavailable on short-term non-hauling policies

- Higher deductible elections — can reduce premium but shift risk back to the operator

Operating Radius and Route

Local, regional, and over-the-road (OTR) classifications affect placement. Your garaging ZIP code and the states your route crosses both influence eligibility and premium — some carrier programs have appetite restrictions in specific states, and interstate routes must satisfy each state's minimum liability requirements.

What Short-Term Truck Insurance Actually Covers

Temporary truck policies are intentionally narrow. They cover essential transit liability, not commercial operations. Understanding the exact boundaries prevents claim denials at the worst possible moment.

Primary Liability (The Non-Negotiable)

Every short-term truck policy must include primary liability — bodily injury and property damage caused to third parties. For interstate for-hire operations on vehicles at or above 10,001 lbs, the federal floor is $750,000 for non-hazardous general freight, $1 million for most hazmat operations, and $5 million for specified hazardous materials including Division 1.1–1.3 explosives and poison gas.

These minimums apply even on short-term policies. If a program is quoting below these thresholds for an interstate move, it's not FMCSA-compliant.

Physical Damage (Optional but Often Critical)

Collision and comprehensive coverage can be added to protect the insured truck itself. If your truck is financed or leased, your lender almost certainly requires physical damage as a condition of the loan — confirm this before assuming the base policy is sufficient. Not all short-term programs offer physical damage as an option, so verify availability in writing before binding.

What Temporary Truck Insurance Does NOT Cover

Most coverage mistakes trace back to these four exclusions:

- Commercial cargo hauling — the single most critical exclusion; attaching a loaded trailer voids the policy instantly

- Vehicle registration — temporary coverage cannot be used to register a commercial vehicle

- Revenue-generating operations — any trip where you're being paid to transport goods

- Geographic zones outside the policy's valid states — crossing into an unlisted state eliminates coverage

Violating the cargo exclusion doesn't just trigger a claim denial. The driver becomes personally liable for every dollar of damages from that accident.

FMCSA Compliance and Filing Limitations

Owner-operators running under their own MC number face an additional complication: short-term policies do not automatically satisfy FMCSA continuous insurance filing requirements.

FMCSA uses Form BMC-91 (or BMC-91X) for bodily injury and property damage filings. Under 49 CFR § 387.313, federal certificates remain continuously effective until formally cancelled — and cancellation requires 30 days' written notice to FMCSA.

Before binding a short-term policy, confirm with your broker whether the program supports the required regulatory filing. A valid COI without the corresponding FMCSA filing still leaves your operating authority technically non-compliant.

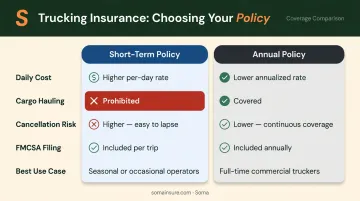

Short-Term vs. Annual Commercial Truck Insurance

Choosing between a 1–5 day temporary policy and a short-lived annual policy isn't just about price — the right answer depends on whether cargo is moving, how long the gap actually is, and whether you can afford a cancellation penalty.

| Factor | Short-Term Policy | Annual Policy |

|---|---|---|

| Daily cost | Higher per day, no down payment | Lower per day, significant upfront |

| Cargo hauling | Prohibited | Permitted under policy terms |

| Cancellation risk | None — fixed term | Short-rate penalties may reduce refund |

| FMCSA filing | Program-dependent; often unsupported | Standard, continuous filing supported |

| Best for | Empty truck transit only | Active commercial hauling operation |

Annual policies can carry minimum earned premium clauses — meaning even if you cancel after two weeks, the carrier keeps a percentage of the full-year premium regardless. Repeated early cancellations raise red flags with underwriters reviewing future applications. If neither option fits your window cleanly, the three workarounds below cover most real-world gaps.

Three Practical Workarounds for a 7-Day Gap

When neither a 5-day policy nor a full annual policy fits cleanly, three approaches apply:

- 5-day policy + park: Lowest cost option, but it leaves a 2-day uninsured gap. Only viable if the truck sits idle on days 6 and 7.

- Pro-rated 30-day binder with early cancellation: If cargo must move during the window, this is your only real choice — though short-rate cancellation penalties apply.

- Temporary Non-Trucking Liability on an existing driver setup: The most cost-effective route for empty tractor moves between terminals. Valid only off-dispatch and outside active business use.

What Most People Get Wrong About Temporary Truck Insurance

Assuming "Temporary" Means "Commercial"

This is the most expensive mistake in short-term truck coverage. The moment commercial cargo is attached to a truck running on a temporary policy, the coverage is void — full stop. Any accident at that point becomes full personal liability exposure.

Under 49 CFR Part 386, fines for failing to maintain required financial responsibility can reach $21,114 per day, with each day of a continuing violation counted as a separate offense.

Ignoring Document Preparation

Automated underwriting systems reject incomplete applications immediately. Have these ready before starting the process:

- Vehicle Identification Number (VIN)

- CDL or commercial driver's license copy

- Origin and destination route details

- Proof of insurable interest (Bill of Sale or title for a purchased vehicle)

Confirm that the policy's effective time matches your actual departure time, not just the calendar date. A policy effective at 12:01 AM doesn't cover a 6:00 PM departure the day before.

Defaulting to the Cheapest Quote

A quote that doesn't meet the freight broker's required liability limit — often $1 million CSL — is useless for that load, regardless of the premium. Many broker contracts also require additional insured status and waivers of subrogation. If those endorsements aren't on the COI, the broker won't accept it.

Conclusion

True one-week truck insurance doesn't exist as a single product. What does exist:

- 1–5 day non-hauling transit policies for short repositioning moves without cargo

- 30-day pro-rated binders for situations requiring longer windows or cargo coverage

- Non-Trucking Liability for empty tractor moves off dispatch

Choosing the wrong option — or misunderstanding the cargo exclusion — creates compliance gaps and personal liability exposure on a commercial vehicle.

The right coverage matches the exact operational window, truck class, and intended use. Soma works with hundreds of carrier partners across specialty trucking markets and can identify and bind the right short-term or binder option for your situation — including a broker-ready COI issued same day.

Frequently Asked Questions

Can you get temporary insurance on a truck?

Yes. Temporary truck insurance is available through specialty markets in 24-hour to 5-day increments. These policies are designed for non-commercial transit — moving an empty truck from an auction or to a repair shop — not for hauling cargo or paid hauling jobs.

How much does one-week truck insurance cost per day?

Published pricing from specialty providers runs from $140 for a 24-hour policy to $540 for 5 days, working out to roughly $100–$140 per day. Cost increases with higher liability limits, physical damage add-ons, heavier truck classes, and adverse driver history.

Can I haul cargo with a temporary truck insurance policy?

No. Commercial cargo hauling is strictly prohibited under short-term truck policies. Attaching a loaded trailer voids the coverage entirely, leaving the driver personally liable for all damages.

What is the maximum duration for a short-term truck insurance policy?

Most short-term programs cap at 5 consecutive days. No standard market offers a true 7-day product. If you need more than 5 days of coverage, a pro-rated 30-day commercial binder is the next available option.

Is short-term truck insurance available in all U.S. states?

Availability varies by state, truck class, and carrier program. NITIC, one specialty provider, is licensed in 48 states. Your garaging ZIP and the states your route crosses both affect eligibility. Interstate routes must also meet minimum liability requirements in every state traveled.

What is the difference between non-trucking liability and short-term truck insurance?

Non-trucking liability (NTL) describes when coverage applies — specifically, when a leased owner-operator uses the truck for personal purposes while off dispatch. Short-term truck insurance describes how long the policy lasts. Confusing the two can result in a rejected COI or an uncovered accident while under dispatch.