The short answer: box truck insurance is not a single number. Costs vary based on who you are, what you haul, where you operate, and how long you've been in business. This guide breaks down realistic cost ranges by operator profile, explains every coverage type involved, and walks through what actually moves the price up or down.

Key Takeaways

- The national median for box truck commercial auto is $909/month according to Insureon's 2025 data

- Business age is the single biggest pricing variable — new ventures pay substantially more than established operators

- The FMCSA minimum is $750K liability, but most freight brokers and platforms require $1M

- Box truck insurance combines multiple coverages; your total cost depends on operation type, cargo, and routes

- A multi-carrier broker like Soma lets you compare quotes from dozens of carriers with one application

How Much Does Box Truck Insurance Cost?

There is no universal rate. Insureon's 2025 benchmark puts the national median for commercial auto on box truck operations at $909/month ($10,910/year) — but that's an aggregate figure across all operator profiles, truck sizes, and coverage structures, not a quote for your situation.

What actually determines your number:

- Operator profile — new venture vs. established carrier

- Driving record — violations and claims history

- Cargo type — hazmat, high-value goods, or general freight

- State and operating radius — local, regional, or interstate

- Coverage stack — what your broker, shipper, or platform requires

The table below provides planning ranges based on operator type. These are directional estimates — actual premiums depend on your specific application.

| Operator Profile | Est. Monthly Range | Est. Annual Range | Notes |

|---|---|---|---|

| Established local/private carrier | $250–$600 | $3,000–$7,200 | Clean record, 3+ years, no cargo insurance needed |

| General for-hire/contract hauler | $600–$1,100 | $7,200–$13,200 | $1M liability + cargo; Insureon median is $909/mo |

| Amazon Relay (experienced) | $670–$1,170 | $8,000–$14,000 | Amazon's Relay-wide planning range for experienced carriers |

| Amazon Relay (newer carrier) | $1,000–$1,500 | $12,000–$18,000 | Amazon's range for newer Relay operators |

| First-year new venture | $1,200–$2,600+ | $14,400–$31,200+ | New authority surcharge + full coverage stack |

Established Local or Private Carriers

If you're hauling your own goods — furniture for your retail store, supplies for your service business — the coverage stack is simpler. Commercial auto liability and physical damage typically cover it. No cargo insurance is needed when you own the freight. Operators with 3+ years of clean history and a local radius will see the lowest premiums in the market.

General For-Hire and Contract Haulers

Once you're hauling freight for others, the coverage requirements expand. Owner-operators working broker loads or direct shipper contracts typically need:

- $1M auto liability — standard for most for-hire operations

- Motor truck cargo — $100K minimum; $250K for higher-value loads

- Physical damage — covers your truck if it's financed or leased

If you're operating as a 1099 solo driver, occupational accident coverage is worth considering as a workers' comp alternative.

New Ventures, Amazon Relay, and Moving Companies

This is the most expensive profile — and the one that produces the most sticker shock. New authority, platform mandates, and liability layering all push premiums higher simultaneously:

- New authority surcharge — carriers price first-year operations as higher risk without a track record

- Platform-mandated limits — Amazon Relay requires $1M auto liability, $1M/$2M general liability, and $100K cargo minimum

- General liability layer — moving companies require GL for in-home work; Amazon requires it for platform access

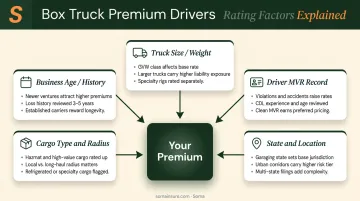

Key Factors That Affect Box Truck Insurance Premiums

Underwriters combine operational, vehicle, and business risk factors into every rate. No two operators pay the same premium.

Truck Size and Weight Class

A 26-foot box truck costs more to insure than a 16-footer — the vehicle is worth more, it causes more damage in an accident, and it typically carries more cargo. The critical threshold is 26,001 lbs GVWR, which is where Class B CDL requirements begin under FMCSA rules. Body length alone doesn't determine CDL status — Enterprise lists its 26-foot box truck at 25,999 lbs GVWR, keeping it just below the CDL threshold. Check the door jamb for the actual rating before assuming.

Business Age and Operating History

New operators face a measurable rate surcharge because insurers have no loss history to evaluate. A clean first year is the fastest path to lower renewal pricing. A single claim, though, can reset that trajectory and push your next renewal up 20–40%.

Cargo Type and Operating Radius

What you haul affects both your auto liability and cargo premiums. Carriers rate cargo risk by theft exposure and value:

- General dry goods — baseline pricing

- Electronics, pharmaceuticals, alcohol — rated higher due to theft exposure and cargo value

- Interstate routes — carry a premium over local-only operations; more states, more miles, more exposure

Driving History and Driver Profiles

Commercial auto policies weight MVR violations more heavily than personal auto. A DUI or at-fault accident doesn't just affect that driver's rating. If a carrier views the hire as a hiring-standards issue, the violation can raise the entire fleet's premium.

Location and State of Operation

Your state — and your ZIP code within that state — affects your rate. Several location factors drive higher premiums:

- High-litigation states (Florida, Louisiana, California, New York) — consistently produce elevated commercial auto rates due to jury verdict averages

- Urban ZIP codes — carry a surcharge even within an otherwise lower-cost state

- Rural states — generally lower premiums where traffic density and verdict awards are modest

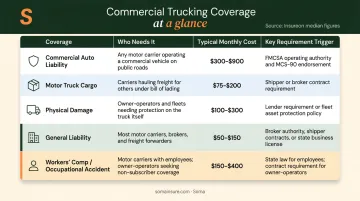

Box Truck Insurance Coverage Types and What They Cost

Box truck insurance works as a stack of individual coverage lines — your total premium reflects every line your operation requires. Understanding what each line covers (and what it costs) helps you build a policy that satisfies regulators, brokers, and lenders without overpaying.

Commercial Auto Liability

This is the foundation of any box truck policy and typically the largest single line item. It covers third-party bodily injury and property damage from on-road accidents.

- FMCSA minimum: $750,000 for interstate for-hire carriers with GVWR over 10,001 lbs

- Market standard: $1M — OOIDA confirms most shippers and brokers require $1M, not the federal floor

- Insureon median: $909/month across box truck commercial auto policies (all sizes/profiles)

Purchasing at the $750K minimum satisfies federal law but will fail most broker and platform COI checks.

Motor Truck Cargo Insurance

Covers freight lost, stolen, or damaged in transit. There is no federal filing requirement for general commodity carriers — the FMCSA minimum applies only to household goods carriers ($5K per vehicle / $10K per occurrence). Most brokers set their own thresholds:

- Most freight brokers require $100K minimum

- Amazon Relay specifically requires $100K

- High-value freight (electronics, medical equipment) often requires $250K

Cargo type and declared value are the primary pricing drivers for this line.

Physical Damage Coverage

Covers repair or replacement of your truck (collision plus comprehensive). Required by most lenders if the vehicle is financed. A higher deductible (moving from $1,000 to $2,500) can reduce this premium, though the right deductible depends on your cash reserves and whether a loss would create a genuine out-of-pocket hardship.

General Liability and Workers' Compensation

These two lines apply based on operation type:

| Coverage | Who Needs It | Insureon Median (Box Truck) |

|---|---|---|

| General liability | Movers, Amazon Relay, anyone with on-premises exposure | $52/month ($621/year) |

| Workers' compensation | W-2 employees (required by most states) | $673/month ($8,080/year) |

| Occupational accident | 1099 solo operators as workers' comp alternative | ~$130–$163/month (OOIDA) |

General liability covers third-party claims that happen off-road: damage inside a customer's home, a client injury at a loading dock. Moving platforms and most freight brokers require it as part of their COI checklist.

Solo 1099 operators who aren't legally required to carry workers' comp should consider occupational accident coverage instead. Providers like OOIDA offer it in the $130–$163/month range — significantly cheaper than a full workers' comp policy.

New Venture vs. Established Operator: The Real Cost Difference

Business age functions as a pricing tier. New operators pay more across every coverage line because carriers have no loss history to evaluate — no claims data, no driver records, no proof of how operations are actually run.

| Factor | New Venture (Year 1) | Established Operator (3+ Years) |

|---|---|---|

| Monthly premium range | $1,200–$2,600+ | $250–$1,100 |

| Carrier availability | Fewer carriers willing to write | Broader market access |

| Down payment at policy start | Often 15–25% of annual premium | Standard billing available |

| Renewal after clean year | Meaningful premium reduction | Stable or modest decrease |

| Renewal after one claim | Significant increase + possible non-renewal | Rate increase, but more manageable |

The down payment requirement catches many new operators off guard. A $20,000 annual premium with a 20% down payment means $4,000 due before the truck moves. Stack that against the FMCSA operating authority fee ($300), LLC filing costs, and the truck purchase or lease — and your Day 1 capital requirement looks nothing like the monthly premium figure you budgeted around.

Build the down payment into your startup budget as a fixed line item, not an afterthought. If you're working with a broker, ask upfront what the estimated down payment will be — that number matters as much as the monthly rate.

How to Lower Your Box Truck Insurance Premium

Some factors are fixed — business age, state, truck size. But several levers can meaningfully reduce what you pay:

- Pay the annual premium upfront — Progressive advertises 13% or more in savings for full payment versus monthly installments

- Raise your physical damage deductible — moving from $1,000 to $2,500 can reduce this component of your premium; only do this if your cash reserves can absorb the higher deductible in a loss

- Install telematics — Progressive's Smart Haul program reported average savings of $1,261 for new truck customers enrolled in a recent period; eligibility varies by vehicle and program

- Protect your first year — a clean year one (no claims, no violations) is the highest-leverage premium reduction available to a new operator; the renewal difference between a clean year and a year with one claim can easily exceed $3,000–$5,000 annually

- Shop across carriers — premiums for identical coverage can vary 30–50% between carriers depending on their current appetite for your operator profile

That 30–50% pricing spread is where broker access makes a practical difference. Soma's trucking insurance program places coverage through carriers including Chubb, Progressive, Kemper, and Ascend using a single-application model: one submission reaches multiple carrier markets simultaneously, rather than requiring operators to approach each carrier independently.

For a risk class where pricing varies this significantly, comparing carriers isn't optional. It's how operators avoid leaving thousands of dollars on the table each renewal cycle.

What Most Box Truck Operators Get Wrong About Insurance Costs

Assuming Personal Auto Covers Commercial Use

Personal auto policies exclude for-hire commercial activity. This is a standard, unambiguous exclusion. If you file a claim while operating commercially under a personal policy, coverage will be denied. You absorb all damages, medical costs, and legal fees personally.

Buying to the Legal Minimum and Failing COI Checks

The FMCSA $750K minimum satisfies federal law. It does not satisfy the freight market. Most brokers require $1M, Amazon Relay requires $1M, and any platform-based hauling will have its own mandatory coverage stack. Purchasing the cheapest policy available often means failing COI checks, losing freight opportunities, and having to re-purchase coverage at the right limits anyway — with a policy gap on your record.

Ignoring the True First-Year Cost Structure

The monthly premium is not the only number that matters in year one. Factor in:

- Down payment: Typically 15–25% of the annual premium, due at policy start

- Installment surcharge: Paying monthly costs more than paying annually

- Claims impact: A minor first-year claim can trigger a renewal increase that exceeds what the claim paid out

A new operator who budgets $1,200/month for insurance but doesn't account for a $4,000 down payment and the installment premium is setting up a cash flow problem from day one.

Frequently Asked Questions

How much is insurance on a 26ft box truck?

Established operators with clean records typically pay $600–$1,100/month, depending on coverage and state. First-year ventures on a 26-footer should plan for $1,500–$2,600+. Insureon's $909/month median is a useful ballpark reference, not a 26-foot-specific figure.

What kind of insurance do I need for a box truck?

At minimum: commercial auto liability. For for-hire hauling, add motor truck cargo. Moving companies need general liability for in-home exposure. Operations with W-2 employees need workers' compensation; 1099 solo operators should consider occupational accident coverage as a substitute.

Is a 26 foot box truck a commercial vehicle?

When used for business purposes, yes. The CDL threshold is 26,001 lbs GVWR, and many commercial 26-foot trucks are built at 25,999 lbs to stay just below it. Check the door jamb for the actual GVWR. Regardless of CDL requirements, personal auto insurance will not cover a box truck in commercial use.

Can I use my personal auto insurance for a box truck?

No. Personal auto policies explicitly exclude commercial and for-hire use — any claim filed while operating for business will be denied, leaving you personally liable for damages, injuries, and legal costs. Commercial auto coverage is required from day one of commercial operation.

What is the minimum liability coverage required for interstate commerce?

FMCSA requires $750,000 for interstate for-hire carriers hauling nonhazardous property in vehicles over 10,001 lbs GVWR. In practice, most freight brokers and shippers — including Amazon Relay — require $1M. Budget to that level from the start.