Introduction

Picture this: two weeks into framing a new home, a fire tears through the structure overnight. The damage is extensive — framing, lumber, temporary wiring, all of it gone. The contractor's general liability policy won't respond because there's no third-party injury claim. The owner's homeowners policy excludes active construction. Nobody's covered.

That gap is exactly what builder's risk insurance exists to fill. Yet confusion about what it actually protects, who's responsible for buying it, and when it needs to start leaves real financial exposure on projects of every size. According to NFPA data, fires in structures under construction cause an annual average of $370 million in direct property damage — and fire is just one of the top three builder's risk claim types, alongside theft and water damage.

Getting the policy right before a project starts — not after the first loss — is what this guide is for.

Key Takeaways

- Builder's risk is property insurance specifically for structures under construction, separate from general liability or homeowners policies

- Covers the building, on-site materials, temporary structures, and materials in transit

- Floods, earthquakes, employee theft, and faulty workmanship are standard exclusions

- Cost typically runs 1%–4% of total project value

- Coverage must be in place before materials arrive on-site; policies don't backdate

What Is Builder's Risk Insurance?

Builder's risk insurance — also called course of construction insurance — is a specialized property policy that covers a structure and its materials while actively under construction. Unlike a permanent property policy, the insurable asset changes in value and risk profile every day the project moves forward.

The Coverage Gap It Fills

Three common policies appear to cover construction losses — but each has a critical blind spot:

- General liability responds to third-party injury or property damage claims — not physical damage to the project itself

- Homeowners insurance typically excludes or severely limits coverage during active construction, including theft of uninstalled materials

- Commercial property insurance generally provides only a $250,000 sublimit for newly constructed buildings, with coverage ending as early as 30 days after construction begins

Builder's risk is the policy that covers first-party physical damage to the project itself.

Policy Forms: All-Risk vs. Named-Peril

Two policy structures exist, and the difference matters:

- All-risk (open-peril): Covers any cause of loss not specifically excluded — the industry standard for most projects

- Named-peril: Only covers events explicitly listed in the policy; if a peril isn't named, the loss isn't covered

All-risk is what AIA contract documents require and what most lenders mandate. Named-peril policies routinely exclude perils like water intrusion and faulty workmanship damage — gaps that only surface after a loss is already filed.

Who Should Be Listed as Named Insureds

Builder's risk works best when all financially exposed parties are on one policy:

- Property owner

- General contractor

- Subcontractors (all tiers)

- Lenders (as loss payees)

Consolidating everyone onto a single policy eliminates post-loss disputes about which party's insurer is responsible — a fight that can delay rebuilding by months.

Why It's Written as Inland Marine

That single-policy structure also explains a technical quirk worth understanding: builder's risk is written on an inland marine form, not a standard commercial property form.

The NAIC's Nationwide Inland Marine Definition specifically classifies "Builders Risks or Installation Risks" within inland marine. The practical reason is portability — this classification lets the policy follow materials as they move (from warehouse to staging yard to job site), rather than anchoring coverage to a fixed address.

What Does Builder's Risk Insurance Cover?

Covered Property

A standard builder's risk policy covers:

- The structure under construction (foundations, framing, electrical, plumbing, HVAC)

- Permanently installed fixtures and equipment

- Temporary structures — scaffolding, construction forms, job site trailers

- Construction signs

- Materials in transit to the site

- Materials stored off-site at warehouses or staging yards

Those last two points matter most on larger projects where materials are ordered months in advance and stored before they ever reach the job site.

Covered Perils

Under a typical all-risk policy, covered causes of loss include:

- Fire and lightning

- Explosion

- Windstorm and hail

- Smoke

- Theft and vandalism

- Riot or civil commotion

- Vehicle or aircraft impact

- Sprinkler leakage

- Collapse

All-risk coverage catches unanticipated events that a named-peril list might miss. Named-peril policies only respond to what's explicitly listed — if a freak event occurs that isn't named, the claim gets denied.

Soft Costs and Optional Endorsements

Soft costs are the indirect financial losses triggered when a covered event delays a project — not labor or materials, but expenses like:

- Extended construction loan interest

- Permit re-application fees

- Revised architectural and engineering drawings

- Lost rental income on a building intended for lease

Soft cost coverage is an endorsement, not standard. On any project with a construction loan, skipping it is a meaningful gap.

Other valuable add-ons available through most carriers:

| Endorsement | What It Covers |

|---|---|

| Flood | Rising water and storm surge damage |

| Earthquake / earth movement | Seismic damage to the structure |

| Ordinance and law | Added cost to rebuild to current code after a loss |

| Pollutant cleanup | Remediation costs following a covered event |

| Debris removal | Clearing the site after a covered loss |

Carriers including Chubb and Zurich offer earthquake, flood, and named windstorm as coverage options — but none of these are included automatically. They require explicit endorsement.

What Builder's Risk Insurance Does NOT Cover

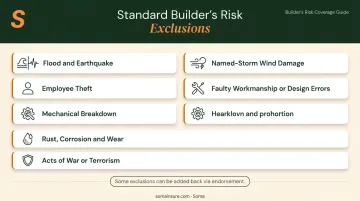

Standard Exclusions

Nearly every builder's risk policy excludes:

- Flood and earthquake (unless endorsed)

- Named-storm wind damage (unless endorsed)

- Employee theft

- Faulty workmanship, defective design, or planning errors

- Mechanical breakdown

- Rust, corrosion, and wear and tear

- Acts of war or terrorism

Worth noting: if faulty workmanship causes a fire, the fire damage is typically covered even though the workmanship itself isn't. The resulting loss is covered — the underlying defect is not.

Coverage That Needs Separate Policies

Builder's risk covers the structure under construction. Separate policies are needed for everything else:

- Third-party injuries and property damage → Commercial general liability

- Contractor tools and mobile equipment → Inland marine / tools & equipment floater

- Vehicles on or traveling to the job site → Commercial auto

- Employee injuries → Workers' compensation

The Transition Gap at Occupancy

Builder's risk terminates when the building is occupied, put to its intended use, or the policy expires — whichever comes first. The owner must have permanent property insurance ready to activate before anyone sets foot in the finished building. There's no grace period between policies; if occupancy happens before permanent coverage is bound, the building is uninsured.

Why Existing Policies Aren't Enough

That gap at occupancy isn't the only coverage trap. Assuming a current homeowners or commercial property policy covers an active project is one of the most expensive misconceptions in construction.

- Standard homeowners policies typically exclude theft of uninstalled building materials during construction

- Commercial property forms include only a $250,000 sublimit for newly acquired or constructed property — and that coverage often ends just 30 days after construction begins

A standalone builder's risk policy is the only form specifically designed for this exposure — not a redundancy, but a necessity.

Who Needs Builder's Risk Insurance — and Who Pays?

Every party with money at risk needs to be protected:

- Property owners (residential and commercial) — their asset is being built

- General contractors — responsible for the work and often contractually liable

- Subcontractors — their installed work is at risk before the project closes out

- Lenders — financing the project and holding a security interest in the asset

Who Buys the Policy?

The contract should specify this clearly. The AIA A101-2017 standard contract defaults to the owner purchasing and maintaining property insurance — unless the contract explicitly shifts that obligation to the contractor.

A contract provision might read: "Owner shall purchase and maintain builder's risk insurance on an all-risk completed-value form for the full insurable value of the project, naming the Contractor and all Subcontractors as additional insureds."

The most expensive outcome is when both parties assume the other has it handled and neither does. That scenario is more common than it should be, and the resulting uninsured loss falls on whoever the contract holds responsible.

For Renovation and New Construction

Builder's risk applies to both new builds and renovation projects, though renovation coverage differs — particularly because the existing structure is also at risk. The contract between owner and contractor should address this explicitly for any significant renovation scope.

Brokers like Soma, which place construction coverage across carriers including Chubb, Liberty Mutual, and Kinsale, let contractors and owners compare terms across multiple markets with a single submission. On complex projects, that comparison matters: deductibles, covered perils, and sublimits for theft or flood can differ substantially from one carrier to the next.

How Much Does Builder's Risk Insurance Cost?

Typical Premium Range

Builder's risk policies typically cost between 1% and 4% of total construction costs. Using that range as a baseline:

- A $250,000 residential build would generate an estimated premium of roughly $2,500–$10,000

- A $2 million commercial project would generate an estimated premium of roughly $20,000–$80,000

These are illustrative calculations based on the cited range — actual premiums depend heavily on project-specific factors.

Factors That Affect Cost

Project-level variables:

- Wood-frame structures carry higher fire risk than masonry or steel, which pushes premiums up

- Coastal areas, flood zones, and high-crime locations increase exposure — and cost

- Longer project timelines mean a longer exposure window, which raises total premium

- Renovations often cost more to insure than new builds because the existing structure is also at risk

Policy-level variables the buyer controls:

- Raising your deductible is the most direct way to lower your premium

- Coverage limit should equal full construction cost — labor, materials, and overhead — but excludes land value

- Policy duration should match the project schedule; a mismatch leaves gaps or wastes money

- Endorsements for flood, earthquake, and soft costs each add to the base premium

Of all these variables, the coverage limit is where owners most often get it wrong.

Watch for under-insurance: If your coverage limit is set below actual rebuild cost and a total loss occurs, you absorb the difference out of pocket. Set the limit to match full anticipated construction cost — not a rough estimate.

When Does Builder's Risk Insurance Start and End?

When to Bind Coverage

Coverage should be in place before materials are first delivered to the job site. Most policies state that coverage begins on or after the policy effective date — meaning any loss before that date is uninsured.

Binding coverage after construction is already underway creates real exposure. Projects already in progress face additional underwriting scrutiny, US Assure notes that projects more than 30% complete are subject to additional underwriting review — they can still qualify, but the process takes longer and terms may be less favorable.

When Coverage Ends

Builder's risk terminates at whichever of these events occurs first:

- The building is occupied (ISO CP 00 20 triggers at 60 days after occupancy or intended use)

- Construction is complete (ISO CP 00 20 triggers at 90 days after completion)

- The project is abandoned

- The policy expires

Projects running over schedule need a formal extension before the end date passes — not after. A lapsed policy that wasn't extended leaves the project uninsured during any remaining construction.

Renovation Projects

For renovation work, a standalone builder's risk policy is required when the renovation scope is significant relative to the existing structure's value. US Assure uses a 20% threshold: if existing-structure coverage is needed, the renovation limit must be at least 20% of the existing structure's value. Property and project owners should confirm with their broker whether existing coverage applies to major renovation work before assuming it does.

Frequently Asked Questions

What is covered in a builder's risk policy?

A standard policy covers the structure under construction, building materials on-site and in transit, temporary structures, and fixtures against perils like fire, theft, windstorm, hail, vandalism, and explosion. Flood, earthquake, soft costs, and ordinance compliance require separate endorsements.

How much builder's risk coverage do I need?

The coverage limit should equal the full anticipated cost of construction: all labor, materials, and soft costs if that endorsement is added. Land value is excluded. Under-insuring leaves the owner responsible for the gap between the policy payout and actual rebuild costs.

Is builder's risk insurance required by law?

No federal or state law universally mandates it, but lenders, government contracts, and SBA 7(a) construction loan programs commonly require it contractually. Most financed projects will carry this requirement regardless of legal mandates.

Who pays for builder's risk — the owner or the contractor?

It depends on the contract. Residential new builds are often purchased by the owner; commercial projects are often purchased by the general contractor, who factors the cost into the bid. The contract should specify this clearly before work begins.

When does builder's risk insurance start and end?

Coverage should begin before materials arrive on-site. It ends upon occupancy, abandonment, or policy expiration — whichever comes first. Most policies allow 60–90 days post-occupancy before terminating, depending on the form.

Does builder's risk cover renovation projects?

Yes, but coverage terms and cost differ from new construction because the existing structure is also at risk. A standalone builder's risk policy is typically needed when renovation scope exceeds 20% of the existing structure's value. Homeowners should not assume their current policy covers major renovation work.