The problem? Pricing varies dramatically. A solo IT consultant might pay under $35/month. A general contractor could pay $140+/month for the same coverage structure. Most businesses don't know where they fall — or why.

This guide breaks down actual CGL premium ranges by risk tier and industry, explains the factors that move pricing up or down, and covers what most businesses miss when budgeting for coverage.

Key Takeaways

- CGL premiums span roughly $29/month for low-risk professionals to $142+/month for high-risk contractors, based on published industry medians

- Industry risk level, employee count, annual revenue, location, and claims history are the primary pricing drivers

- 91% of small businesses purchase a $1M per occurrence / $2M aggregate limit structure

- Standard CGL excludes professional errors, employee injuries, auto incidents, and cyber events — all of which require separate policies

- Hard-to-insure industries (construction, hospitality, trucking, childcare) often need specialty or surplus lines markets

How Much Does Commercial General Liability Insurance Cost?

CGL premiums don't follow a fixed schedule. Two businesses in the same industry with different revenue, employee counts, or claims histories can receive very different quotes from the same carrier.

Insureon's published data shows a median of $45/month ($538/year) across its small-business customer base, with annual policies ranging from roughly $250 to over $3,000. About 22% of businesses pay under $30/month; 41% pay between $30 and $60/month.

Misunderstanding this variability creates real problems:

- Underestimating premiums leads to budget shortfalls at renewal

- Selecting inadequate limits to cut costs leaves gaps in coverage

- Excluded claims get denied — a surprise no business wants mid-crisis

Low-Risk Business Tier

Typical monthly range: ~$29–$45/month

Published medians from industry sources include:

- IT consultants: $31/month

- Photographers: $29/month

- Accountants/CPAs: $30/month

- Freelancers (general): $45/month

Policies at this tier typically carry $1M/$2M limits with minimal add-ons. Coverage focuses on visitor injury, accidental property damage, and advertising injury.

Best for: Solo operators, home-based businesses, and office-only professionals with limited physical client interaction.

Mid-Risk Business Tier

Typical monthly range: ~$38–$44/month

Published medians include:

- Retail stores: $42/month

- House cleaners: $44/month

- Engineers: $38/month

- Property managers: $44/month

- E-commerce businesses: $42/month

Policies at this tier include products/completed operations coverage alongside premises liability — important for businesses that sell physical goods or work inside client properties. Some businesses in this tier also need professional liability (E&O) for service-related decisions.

Best for: Businesses with customer foot traffic, physical storefronts, or those selling physical products.

High-Risk Business Tier

Typical monthly range: ~$54–$142/month

Published medians include:

- General contractors: $142/month

- Restaurants: $141/month

- Human/social services (daycare proxy): $91/month

- Auto repair shops: $54/month

- Electricians: $57/month

- Manufacturers: $50/month

Premiums at this tier reflect constant exposure: job-site accidents, customer injuries, equipment use, and completed work claims. Many businesses here also carry specialty endorsements based on their operations:

- Liquor liability for restaurants and bars

- Abuse and molestation coverage for childcare providers

- Contractors' errors coverage for construction firms

Best for: Construction, food service, manufacturing, childcare, and transportation businesses where physical risk is part of daily operations.

Key Factors That Affect Your CGL Insurance Premium

Insurers build CGL premiums using a combination of operational, technical, and risk-based factors. No two businesses are priced identically.

Industry and Type of Work

Industry is the single largest pricing driver. The published gap between an IT consultant ($31/month median) and a general contractor ($142/month median) reflects the difference in daily exposure — one works at a desk, the other manages job sites.

Some industries carry risks that standard admitted carriers won't underwrite at all. These businesses typically end up in surplus lines markets, where carriers have more pricing flexibility:

- Construction with complex completed-operations exposure

- Bars and nightclubs facing dram shop liability

- Childcare providers with abuse and molestation exposure

Soma works with carriers like Markel, Kinsale, Chubb, and Liberty Mutual to place exactly these types of businesses — including many that standard brokers decline outright.

Business Size: Employees and Revenue

More employees means more opportunities for accidents, which raises premiums directly. Higher revenue signals greater operational exposure — particularly in contractor and manufacturing industries where more revenue means more active jobs and more completed work in the field.

Insurers often audit CGL policies at renewal, reconciling estimated payroll or revenue against actual figures. If your business grew significantly during the policy year, expect a premium adjustment.

Coverage Limits and Deductibles

The standard structure — $1M per occurrence / $2M aggregate — is used by 91% of small businesses. Stepping up to $2M/$4M limits typically adds 15–25% more to the annual premium, though the exact difference depends on industry and risk profile.

Deductibles work the other way: choosing a higher deductible reduces the monthly premium but increases your out-of-pocket cost when a claim occurs. This trade-off only makes sense if you have the cash reserves to absorb it.

Business Location and Claims History

Geography affects pricing through state tort environments, local claim rates, and population density. Businesses in high-litigation states or dense urban markets generally pay more, though no reliable universal state-by-state differential figures exist in published industry data.

Claims history is equally significant. A clean record over several years can reduce premiums at renewal, while prior claims — even settled ones — signal elevated risk and trigger surcharges. Newer businesses often start at higher rates until they build a track record.

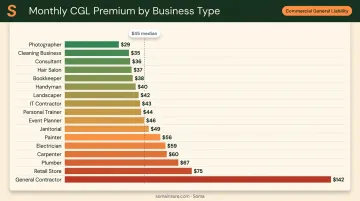

CGL Insurance Cost by Industry and Business Type

The table below summarizes published monthly premium medians by business type, along with the primary risk exposure driving cost.

| Business Type | Monthly Median | Primary Risk Factor |

|---|---|---|

| Photographer | $29 | Client/studio injury, property damage |

| Accountant/CPA | $30 | Visitor injury, advertising injury |

| IT Consultant | $31 | Client injury, property damage |

| Engineer | $38 | Visitor injury, third-party property damage |

| Real estate business | $40 | Open-house injury, client property |

| Retail store | $42 | Foot traffic, products sold |

| E-commerce | $42 | Product-caused injury or damage |

| House cleaner | $44 | Wet-floor injury, client property damage |

| Property manager | $44 | Premises injury, property damage |

| Box truck business | $52 | Non-driving third-party injury |

| Manufacturer | $50 | Product liability, premises operations |

| Auto repair shop | $54 | Customer injury, third-party property |

| Electrician | $57 | Electrical injury, fire/property damage |

| Hotel/hospitality | $68 | Guest injury, premises exposure |

| Human/social services | $91 | Participant injury, professional care |

| Restaurant | $141 | Customer injury, food/product claims |

| General contractor | $142 | Job-site injury, completed operations |

When Standard Markets Won't Write the Risk

Construction, trucking, hospitality, security agencies, childcare, and certain manufacturing operations frequently fall outside standard carrier appetite. The reasons vary:

- Prior claims history or adverse loss runs

- Assault and battery / abuse and molestation exposure

- New ventures with no operating track record

- Complex multi-policy exposure stacks across several lines

- Specialty commodities or hazmat operations

When standard carriers decline, surplus lines markets offer the pricing flexibility and underwriting appetite to fill the gap. Soma places these hard-to-insure businesses with carriers including Kinsale, Markel, Chubb, and Liberty Mutual, covering industries from construction and trucking to hospitality and childcare.

How the Rate-per-$1,000 Calculation Works

Many CGL policies are priced using a rate applied per $1,000 of payroll or revenue. The formula:

Exposure × Rate ÷ $1,000 = Base Premium

If a contractor has $500,000 in annual payroll and the carrier assigns a rate of $4.00 per $1,000, the base premium before adjustments would be $2,000. As revenue or payroll grows, so does the base premium, which is why growth-stage businesses often see significant CGL increases at renewal even without any claims.

How to Lower Your CGL Insurance Premium

Bundle Policies Strategically

Combining CGL with commercial property insurance in a Business Owner's Policy (BOP) typically costs less than buying each policy separately. According to the Insurance Information Institute, BOPs are generally designed for smaller, lower-risk businesses — commonly those with fewer than 100 employees and under $5 million in revenue.

High-risk industries (construction, trucking, hospitality with liquor liability) typically don't qualify for a BOP and need standalone CGL paired with separate lines.

Manage Risk Proactively

A lower-risk profile at renewal translates directly to more favorable pricing. Practical steps:

- Implement documented safety protocols and employee training programs

- Avoid filing small claims that can be absorbed out-of-pocket

- Maintain clean job-site documentation and incident logs

- Address hazards before they result in claims

For complex or high-risk operations, working with a broker that reviews your exposure profile before renewal — not just after a claim — can meaningfully reduce what you pay at the next renewal cycle.

Calibrate Limits and Payment Timing

Buying $5M in limits when your contracts only require $1M wastes premium dollars. Match your coverage limits to actual contractual requirements and risk exposure.

Payment structure matters too. Paying the annual premium upfront rather than in monthly installments often yields a carrier discount — the exact percentage varies, but Insureon notes it's one of the more consistent cost-reduction options available.

What Most Businesses Miss When Budgeting for CGL Insurance

Focusing Only on Monthly Premium

A lower premium often comes with a higher deductible. A business saving $30/month by choosing a $2,500 deductible over a $500 one might save $360/year — but face $2,000 more in out-of-pocket costs on a single mid-sized claim. Compare the full cost picture, not just the monthly number.

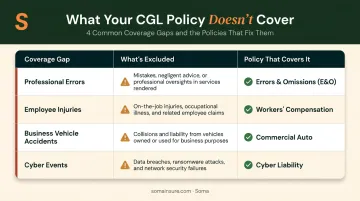

Assuming CGL Covers Everything

Standard CGL has clear exclusions that surprise many business owners at claim time:

| Coverage Gap | What's Excluded | Policy That Covers It |

|---|---|---|

| Professional errors/negligence | Mistakes in your services or advice | E&O / Professional Liability |

| Employee injuries | Work-related illness or injury | Workers' Compensation |

| Business vehicle accidents | Incidents in company vehicles | Commercial Auto |

| Cyber events / data breaches | Ransomware, data theft, breach response | Cyber Liability |

Hiscox reports that 77% of surveyed U.S. small businesses are underinsured. Businesses that assume CGL covers every liability exposure tend to find the gaps only after a claim is denied.

Underestimating Growth's Impact at Renewal

Coverage gaps aren't the only surprise at renewal. If your business grows revenue, adds employees, expands locations, or takes on higher-risk contracts, insurers will audit your payroll and revenue figures — and any exposure above the original estimate triggers a premium adjustment. Budget for renewal based on projected growth, not just what you paid in year one.

Frequently Asked Questions

How much does commercial general liability insurance cost for different coverage limits?

The most common structure — $1M per occurrence / $2M aggregate — runs a median of about $45/month across small businesses. Stepping up to $2M/$4M typically adds $200–$500 annually, though the exact difference depends on your industry and business size.

What is the standard commercial general liability policy?

A standard CGL policy typically carries $1M per occurrence / $2M aggregate limits and covers third-party bodily injury, property damage, personal and advertising injury, and products/completed operations. This structure is used by 91% of small businesses purchasing through Insureon.

How do you calculate commercial general liability insurance rate per $1,000?

Insurers assign a class-based rate (dollars per $1,000 of payroll or revenue), then multiply that rate by total payroll or revenue to produce the base premium. Adjustments for claims history, location, and coverage limits are applied from there.

What factors drive up commercial general liability insurance costs the most?

Industry risk level, employee count, prior claims history, and operating in a high-litigation state are the biggest premium drivers. Construction and restaurant businesses routinely pay three to five times more than comparable office-based businesses.

Can I bundle CGL insurance with other policies to save money?

Yes — combining CGL with commercial property in a BOP is a common strategy for qualifying small businesses. Adding workers' comp or commercial auto through the same carrier can also unlock discounts when bundled with the same carrier.

Is commercial general liability insurance tax deductible?

Yes. IRS Publication 334 confirms that premiums for insurance covering business liability are deductible as ordinary business expenses. Consult a tax professional for guidance specific to your business structure and state.