This guide covers what those numbers actually look like by trade and coverage tier, the factors underwriters use to set your rate, how year-end audits can change your final bill, and concrete steps to keep costs under control.

Key Takeaways

- A standard $1M/$2M GL policy for a small-to-mid-sized contractor typically costs between $750 and $2,500 per year, with trade type and location pushing premiums in either direction

- Premiums are estimates at inception; auditable policies reconcile the final cost against actual revenue, payroll, and subcontractor spend at year-end

- High-risk trades like roofers and general contractors pay significantly more than lower-risk trades like painters or electricians

- Managing subcontractor COIs, keeping clean loss runs, and shopping multiple carriers can cut your annual premium

How Much Does General Liability Insurance Cost for Contractors?

There is no single price for contractor general liability insurance. The premium quoted at policy inception is an estimate. The final cost gets settled at the year-end audit, once the carrier reconciles actual gross receipts, payroll, and subcontractor spend against the projections used to calculate your deposit premium.

Cost by Coverage Tier

| Tier | Who It Fits | Estimated Annual Cost |

|---|---|---|

| Entry-level | Lower-risk trades, minimal operations, limited project sizes | $500–$800/year |

| Standard ($1M/$2M) | Most small-to-mid-sized contractors across all trades | $750–$2,500/year |

| High-limit / umbrella-stacked | GCs, commercial projects, high-hazard trades | $2,500+/year |

The $1M per occurrence / $2M aggregate structure is the most common — The Hartford reports an average of $824/year for contractor GL at this limit, while Insureon's contractor data shows a median of $981/year, with 97% of their contractor clients choosing the $1M/$2M structure. Most licensing boards and commercial contracts require at least this level.

Cost by Contractor Trade

Published medians from carrier and platform data, ordered from lowest to highest risk:

| Trade | Estimated Annual Premium | Monthly Equivalent |

|---|---|---|

| Drywallers | $688/year | ~$57/month |

| Electricians | $684/year | ~$57/month |

| Painters | $704/year | ~$59/month |

| Flooring installers | $759/year | ~$63/month |

| Landscapers | $432–$864/year | $36–$72/month |

| HVAC technicians | $941/year | ~$78/month |

| Plumbers | ~$1,380/year | ~$115/month |

| Excavation contractors | $1,522/year | ~$127/month |

| Roofers | ~$1,596/year | ~$133/month |

| General contractors | $1,700/year | ~$142/month |

Two trades consistently sit at the high end for distinct reasons:

- Roofers carry elevated exposure from height-related work, falling objects, water intrusion risk, and completed-work claims

- General contractors carry vicarious liability for every subcontractor on the project, meaning their policy responds to sub errors even when the sub carries its own coverage.

Geography multiplies these baseline rates considerably. New York's Scaffold Law holds property owners and GCs strictly liable for gravity-related injuries, pushing premiums well above national medians. A 2025 study commissioned by the Building Trades Employers' Association found New York construction insurance costs running 200%–500% above comparable states.

States with stronger tort reform generally keep premiums near the lower end of each trade range.

These figures are medians, not quotes. Trade, location, revenue, and claims history all shift your actual number — sometimes by more than the ranges above suggest.

Key Factors That Determine Your General Liability Insurance Premium

Underwriters weigh a specific set of risk factors to price a contractor's GL policy. Know what they're looking for and you'll have a much clearer picture of what you'll pay — and where you have room to push back.

Trade Classification and Type of Work

Insurance carriers assign every contractor an ISO classification code that reflects the statistical risk level of their daily operations. The code determines both the exposure base (payroll, gross sales, or another measure) and the base rate applied to it.

High-severity trades like roofing and excavation carry significantly higher base rates than finish work like painting or flooring. If your classification doesn't accurately reflect your actual work, the carrier can reassign it at audit — potentially increasing your premium retroactively. Contractors who perform multiple trade types need to ensure their policy reflects the full scope of operations, not just the primary one.

Business Size: Revenue, Payroll, and Subcontractor Costs

GL premiums scale with business activity. Higher gross receipts and payroll signal more active job sites and broader exposure, so the carrier charges more.

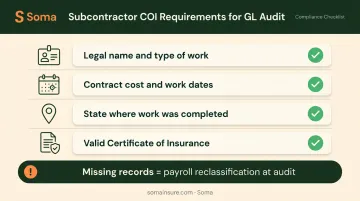

Subcontractors require particular care. When you hire subs, carriers want proof those subs carry their own insurance. Without documented Certificates of Insurance (COIs), the auditor may treat subcontractor payments as additional payroll — rated at the applicable trade class. Travelers' audit guidelines specify the following for each subcontractor on record:

- Legal name and type of work performed

- Contract cost and work dates

- State where work was completed

- Valid Certificate of Insurance

Missing or incomplete records won't receive the benefit of the doubt at audit.

Geographic Location and State Laws

State laws governing construction liability function as a rate multiplier on top of the base trade premium. New York's Scaffold Law is the clearest example: it creates absolute liability for gravity-related injuries on construction sites, which means insurers price New York contractor GL substantially higher than in states where comparative negligence applies.

States with meaningful tort reform — where contributory negligence standards limit plaintiff recovery — generally see contractor GL premiums closer to national medians.

Claims History and Years in Business

Carriers typically review three to five years of loss runs when underwriting a contractor. Frequent or severe past claims indicate poor safety practices and drive rates up. A clean multi-year record qualifies contractors for preferred pricing tiers and access to a broader range of A-rated carriers.

New businesses pay more by default. Without documented loss history, underwriters have no track record to work with and price for the unknown. Carriers like Great American require at least three years of continuous contracting experience and five years of loss runs for their GC programs.

Coverage Limits and Deductibles

Higher coverage limits increase the premium; higher deductibles lower it but shift more out-of-pocket risk to the contractor. The relationship isn't perfectly linear — carriers use increased-limit factors to calculate the cost of higher limits, so doubling your limits won't double your premium, but it will raise it meaningfully.

Policy design choices add up quickly. Common add-on endorsements — blanket additional insured status, completed operations extensions, blanket waiver of subrogation — each carry their own cost impact and are frequently required by project owners and GCs before work begins.

What's Actually Included in a Contractor's GL Premium

A standard contractor GL policy (ISO form CG 00 01) provides four core coverages:

- Coverage A: Third-party bodily injury and property damage caused by an occurrence on the job site

- Coverage B: Personal and advertising injury (defamation, wrongful eviction, copyright infringement in ads)

- Coverage C: No-fault medical payments for third parties injured on your premises

- Products and completed operations: Covers qualifying injury or property damage arising from work you've already finished — this is particularly relevant to contractors, where defect claims often emerge months or years after project completion

Common Add-Ons

Contractors typically bundle GL with three additional lines:

- Tools and equipment (inland marine): Covers owned tools and equipment against theft, damage, and loss — approximately $14/month as a standalone addition

- Commercial umbrella: Stacks additional limits above GL and other underlying policies — approximately $143/month for GCs who need limits above the standard $1M/$2M

- Professional liability: Required for design-build contractors or those offering consulting services — not included in standard GL

What GL Does Not Cover

Knowing these exclusions upfront prevents costly surprises when a claim is filed:

- Damage to your own tools and property (requires inland marine/tools coverage)

- Worker injuries (requires workers' compensation)

- Vehicle accidents on the way to or from a job site (requires commercial auto)

- Professional design errors on design-build projects (requires professional liability)

GL is third-party coverage only — if a claim involves your own equipment or employees, a separate policy applies.

How to Lower Your General Liability Insurance Costs

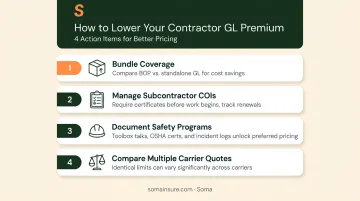

Baseline rates are set by trade and location, but contractors have genuine leverage over the final premium through operational discipline and smart policy structuring.

Bundle Coverage Where It Makes Sense

Combining general liability with commercial property coverage in a Business Owner's Policy (BOP) typically costs less than buying both policies separately. This structure works best for contractors who maintain a shop, office, or storage facility with insurable property. A mobile contractor who operates entirely from job sites gains less from the property component.

Soma's access to carrier partners including Chubb, Liberty Mutual, and Kinsale allows contractors to compare bundled program structures alongside standalone GL options — useful when your risk profile is complex or doesn't fit neatly into a standard market appetite.

Manage Subcontractor COIs Rigorously

The "no COI, no pay" approach is the single most effective administrative control for audit cost management. Every subcontractor you hire should provide a current certificate of insurance before work begins, and that certificate should be tracked and renewed as policies expire.

A manual spreadsheet works for small operations, but it breaks down quickly as subcontractor volume grows. Purpose-built COI tracking tools — or assigning a dedicated staff member to manage compliance — prevent the documentation gaps that give auditors cause to reclassify subcontractor payments as direct payroll.

Maintain Clean Loss Runs and Document Safety Programs

Carriers offer underwriting credits for documented safety programs because toolbox talks, OSHA certifications, and incident logs demonstrate active claim prevention. A multi-year clean loss run unlocks preferred pricing tiers and access to a wider selection of A-rated carriers who would otherwise pass on the risk.

That documentation has a second use: when you move carriers, it becomes part of your submission package and directly influences the rates you're offered. Start with a simple log of safety meetings, training dates, and certifications.

Compare Multiple Carrier Quotes Before Binding

Premiums for identical coverage limits can vary significantly between carriers for the same risk profile, particularly for trades in the middle of the risk spectrum where carrier appetite is less predictable than for clearly standard or clearly high-hazard accounts.

Working with a broker who submits to multiple carriers simultaneously gives you an actual market comparison rather than a single take-it-or-leave-it price. When reviewing quotes, look beyond the headline premium:

- Confirm limits and deductibles are equivalent across all options

- Check for exclusions specific to your trade or scope of work

- Flag any policy priced 20%+ below market — the difference is usually in the exclusions

What Most Contractors Get Wrong About GL Insurance Costs

Three mistakes consistently cost contractors more than they expect.

Choosing the Lowest Premium Without Reading Exclusions

A policy priced well below market often contains gaps: residential work exclusions, action-over exclusions (which can bar coverage when a subcontractor's employee sues the GC), or subcontractor restrictions that limit coverage for work performed by others.

These exclusions don't appear as line items — they're buried in endorsements. The result is a denied claim that costs far more than the premium savings ever would.

Underestimating What Year-End Audits Add to the Bill

Many contractors budget for the deposit premium and treat it as the total cost. It isn't. If revenue grew mid-year, a large subcontractor was added, or payroll ran higher than projected, the audit produces an additional charge at reconciliation.

Estimating conservatively at inception — and tracking actuals against projections throughout the year — prevents audit surprises.

Letting Coverage Lapse Between Projects

Even a short gap in coverage signals risk to underwriters, eliminates renewal discounts, and can disqualify a contractor from preferred pricing tiers that require three to five years of continuous coverage history.

Keep coverage active year-round. The cost of maintaining it through slower periods is far lower than the cost of re-entering the market as a new account.

Frequently Asked Questions

How much should general contractor insurance cost?

Insureon's data puts the median at $1,700/year for a $1M/$2M policy; NEXT reports most GC customers in a $57–$224/month range. GC premiums sit at the top of the contractor spectrum because GCs carry vicarious liability for every subcontractor's errors on the project.

How is general liability insurance calculated for contractors?

Underwriters estimate the premium at inception using trade class code, projected revenue, payroll, and subcontractor costs. At year-end, the carrier audits your actual figures and adjusts the premium up or down based on what your business actually did, not the original projection.

Which contractor trade pays the most for general liability insurance?

Roofers and general contractors top every published premium survey. Roofers face extreme physical hazard from heights, falling objects, and water intrusion. GCs pay heavily for a different reason: they carry vicarious liability for the entire project scope, not just their own crew's work.

Does my state affect how much I pay for contractor general liability insurance?

Yes — significantly. State liability laws act as a rate multiplier on base trade premiums. New York's Scaffold Law creates strict liability for gravity-related construction injuries, driving premiums 200%–500% above comparable states according to industry research. States with tort reform typically keep contractor GL premiums near the lower end of national ranges.

Is a $1 million general liability policy enough for most contractors?

The $1M per occurrence / $2M aggregate structure meets most licensing requirements for smaller residential and commercial jobs. General contractors, commercial work, or contracts with large project owners typically require higher limits, either through a higher-limit GL policy or a commercial umbrella layered on top.

Can a new contractor business get general liability insurance at an affordable rate?

New businesses pay more without loss history, but the gap can be narrowed. Documenting trade experience, holding relevant certifications (OSHA 10 or 30, trade licenses), and working with a broker who submits to multiple carriers at once all improve your starting rate.