Introduction

A single injury claim can cost a home daycare provider tens of thousands of dollars — and that's before legal fees. According to NAEYC's 2024 survey of early childhood educators, 63% of family child care providers reported liability insurance cost increases, and 57% reported difficulty finding affordable coverage. The market is under real pressure, and providers are caught in the middle.

Costs also vary dramatically. A basic homeowners endorsement might run a few hundred dollars annually. A comprehensive commercial package can exceed $2,000. That gap isn't just about price — it reflects what actually gets covered when a claim hits.

The lower end of that range comes with a catch: standard homeowners policies don't cover home daycare operations. Most exclude commercial activities entirely. A provider who assumes they're protected often finds out otherwise only after filing a claim.

This guide breaks down what home daycare insurance actually costs, what drives premiums up or down, and how to build a coverage budget that reflects your real exposure — not just the minimum required to stay licensed.

TL;DR

Key takeaways before you read further:

- Home daycare insurance typically runs $400–$2,500+ annually, depending on coverage type and scope

- Costs rise with more children in care, employees on staff, higher coverage limits, prior claims, or urban location

- Costs stay lower for solo providers with 2–3 children, a clean claims history, and minimal operational risk

- Expect higher premiums when you have staff, transport children, or run a full-time operation with larger enrollment

How Much Does Home Daycare Insurance Cost?

Home daycare insurance doesn't have a fixed price. Costs shift based on coverage type, enrollment size, location, and your specific risk profile. Providers who underestimate these costs either choose coverage too thin to handle a real claim, or skip it entirely and face out-of-pocket liability.

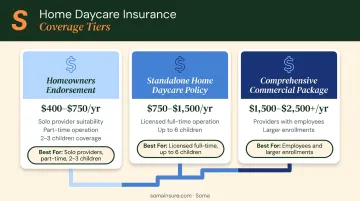

Typical Cost Ranges by Policy Tier

| Policy Tier | Typical Annual Range | Best For |

|---|---|---|

| Homeowners Endorsement | ~$400–$750 | Solo providers, 2–3 children, part-time, minimum compliance |

| Standalone Home Daycare Policy | ~$750–$1,500 | Licensed full-time providers, up to 6 children |

| Comprehensive Commercial Package | ~$1,500–$2,500+ | Providers with employees, larger enrollments, state-mandated minimums |

Important caveat: No single authoritative source publishes standardized price ranges for each tier. Wisconsin's insurance regulator states that daycare liability premiums "vary significantly among companies according to their rating factors." These ranges reflect the market landscape, but your actual quote will depend on your operation — get multiple quotes before committing.

Entry-level (homeowners endorsement): Some insurers, like American Family, offer a home-business option that extends limited personal property, medical-expense, and personal-liability coverage to small daycares. What this generally excludes:

- Professional liability

- Abuse and molestation coverage

- Workers' compensation

- Umbrella protection

For most licensed providers, this gap in coverage becomes a problem the moment a serious claim arrives.

Mid-range (standalone policy): Purpose-built home daycare policies cover general liability, professional liability, and business property. Markel's in-home daycare program, for example, accepts providers caring for 1–18 children and offers limits up to $1M per occurrence/$3M aggregate — but auto, property, and homeowners insurance remain separate.

High-end (comprehensive package): Full commercial coverage adds abuse and molestation, workers' compensation, and umbrella layers. Providers typically reach this tier when they employ staff, transport children, or face state-mandated minimums above basic policy limits.

Key Factors That Affect Your Home Daycare Insurance Premium

Premiums are shaped by a combination of operational, geographic, and risk-profile factors. Knowing these helps you anticipate costs and compare quotes intelligently.

Number of Children in Care

Enrollment is one of the most direct premium drivers. More children means higher probability of incidents — injuries, allergic reactions, disputes over supervision. Insurers typically tier pricing around enrollment bands, and at a certain threshold, a homeowners endorsement becomes inadequate and a standalone commercial policy is required.

Markel's program accepts providers from 1–18 children under a single standalone structure, which illustrates how broadly enrollment can range within specialized markets.

Location and State Regulations

Where you operate affects both your baseline costs and your minimum requirements.

- Texas requires $100,000 per occurrence of negligence coverage for listed family homes. Providers who can't obtain coverage must notify parents and HHSC — which means going uninsured isn't quietly an option.

- The Bipartisan Policy Center found that 13 states require liability coverage for family home-based providers, while 21 states require coverage for certain licensed family child care home types under NAEYC's broader review.

- Urban areas carry higher litigation costs and lawsuit frequency, which translate to higher premiums regardless of individual risk.

Number of Employees and Payroll

Hiring even one part-time assistant changes your insurance picture in three specific ways:

- Workers' compensation becomes required in most states

- Insurers calculate workers' comp rates per $100 of payroll — more payroll means higher premiums

- Professional liability exposure expands because you're now responsible for a second person's conduct

- NCCI designates class code 8869 for child care services under workers' comp classification

Claims History and Experience Level

Underwriters weigh both your track record and your credentials when pricing coverage:

- Prior claims flag you as higher risk at renewal — even a single incident can shift your rate tier

- Formal training and certifications signal professionalism, which specialty carriers factor into risk assessment

- Licensing compliance matters to the markets most home daycare providers depend on, even when carriers don't advertise explicit credential discounts

Coverage Limits and Deductibles

Higher limits cost more; higher deductibles lower your premium. A few practical examples:

- Choosing a $2M aggregate instead of $1M can add $100–$300 or more annually, depending on the carrier

- A $500 deductible costs more in premium than a $1,500 deductible

- Selecting low limits to reduce premium saves money until a claim exceeds those limits — then you're personally responsible for the difference

The goal isn't the cheapest premium — it's the right coverage floor for your enrollment size and operations.

What Does Home Daycare Insurance Cover — And What Does Each Part Cost?

Total insurance cost is built from multiple coverage types. Most providers need a combination, not a single policy. Here's what each layer covers:

General Liability Insurance

The foundation of any home daycare insurance program. Covers:

- Bodily injury (a child falls, breaks an arm)

- Third-party property damage

- Legal defense costs

Most states require general liability at minimum for licensed home daycares. Markel's in-home program includes GL as its core coverage with limits up to $1M per occurrence. Typical annual cost for standalone GL coverage in the daycare segment runs roughly $400–$800 depending on enrollment and location, though rates vary significantly by carrier.

Professional Liability (Errors & Omissions) Insurance

Covers negligence claims — for example, a parent alleges their child was injured because supervision was inadequate. This is often purchased as an add-on to general liability.

For home daycare providers, it closes a gap that GL alone leaves open:

- General liability covers accidents — a child trips, property gets damaged

- E&O covers claims that your professional judgment or conduct was deficient

Business Property Insurance

Covers daycare-specific equipment — toys, educational materials, playground equipment, kitchen appliances used for meal prep — against fire, theft, or vandalism. This is a distinct coverage from standard homeowners property protection.

Most homeowners policies exclude business-use items entirely. That $3,000 worth of childcare equipment in your living room likely has zero protection under your personal home policy.

Abuse and Molestation Coverage + Workers' Compensation

Abuse and molestation coverage is frequently underestimated. Great American Insurance specifically warns that this coverage is "often misunderstood and purchased with minimal, ineffective limits" — and that abuse/molestation limits are separate from general liability and professional liability limits. A single unsubstantiated allegation can trigger expensive legal defense costs before any claim is ever proven. Without adequate limits, those defense costs come directly out of pocket.

Workers' compensation becomes relevant the moment you hire anyone. It covers medical bills and lost wages for employees injured on the job, and most states mandate it regardless of whether staff are full-time or part-time. Rates apply per $100 of payroll under NCCI class code 8869 for child care services, with state-specific factors affecting the final premium.

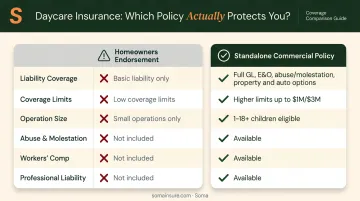

Endorsement vs. Standalone Policy — What's the Difference?

Some providers add a daycare endorsement to their homeowners policy. Others purchase a standalone commercial policy. The right choice depends on the scope of your operation — and the wrong choice can leave a claim entirely uncovered.

| Dimension | Homeowners Endorsement | Standalone Commercial Policy |

|---|---|---|

| Coverage breadth | Basic liability extension only | GL, E&O, abuse/molestation, property, auto options |

| Coverage limits | Typically low | Higher limits available (up to $1M/$3M with Markel) |

| Eligibility | Generally limited to smaller operations | Accepts providers from 1–18+ children |

| Abuse/molestation | Rarely included | Available as standard component |

| Workers' comp | Not included | Can be bundled |

| Professional liability | Not included | Available as add-on or bundle |

The Texas Department of Insurance states explicitly that homeowners insurance will not cover losses related to a daycare operated from a listed family home. This is a documented exclusion, not an ambiguous policy gap.

A standalone policy costs more upfront, but it provides coverage that actually responds when a claim occurs. For any provider operating full-time or caring for more than three children, a standalone commercial policy is the right starting point.

How to Estimate the Right Budget for Home Daycare Insurance

Rather than choosing the cheapest option available, anchor your budget to your actual risk profile. Work through these questions first:

- How many children are in care, and on what schedule? Part-time solo provider vs. full-time 6-child program are completely different risk profiles.

- Do I have employees? Even one part-time aide adds workers' comp and expanded professional liability costs.

- Does my state mandate specific minimums? Texas requires $100,000 per occurrence — that's your floor, not your ceiling.

- Do I transport children? If yes, commercial auto or hired & non-owned auto coverage becomes necessary.

- Do I have significant business property to protect? Equipment, playground structures, and kitchen appliances need separate coverage from your homeowners policy.

Each "yes" expands your coverage need and your budget accordingly.

Once you've mapped out your risk profile, the next step is finding a broker who understands childcare risk specifically. Soma places home daycare coverage through specialty carriers that standard markets often decline, and a single application gets you quotes across multiple carriers. Their process is built to handle everything from a 2-child home operation to a full infant care program — including licensing and renewal deadlines.

What Most Home Daycare Providers Get Wrong About Insurance Costs

Focusing Only on Upfront Premium

The cheapest policy often carries low coverage limits or excluded risks. A $400/year endorsement sounds reasonable until a claim exceeds its limits, and the provider is personally liable for everything above that ceiling. The upfront premium is not the real cost of insurance — the real cost is what you pay when a claim happens.

Assuming Homeowners Insurance Is Sufficient

Beyond premium costs, the type of policy matters just as much. Standard homeowners policies explicitly exclude commercial activities, including home daycares. Most providers don't discover this exclusion until they file a claim — exactly when it's too late to fix. The Texas DOI documents this clearly: daycare-related losses are not covered under homeowners insurance for a listed family home. That exclusion means a full denial of coverage, not a partial reduction.

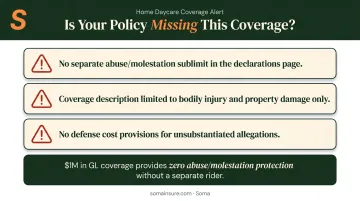

Skipping Abuse and Molestation Coverage

This is the most consistently overlooked gap in home daycare insurance. Even a single unsubstantiated allegation can trigger legal defense costs that run into the tens of thousands before the case is ever resolved. Carriers like Great American Insurance treat abuse/molestation limits as entirely separate from general liability and E&O. A policy with $1M in GL coverage provides zero protection for an abuse claim unless that coverage is specifically added. Providers working with a broker who understands daycare-specific risks — such as Soma, which places this coverage as a standard component rather than an optional add-on — are far less likely to discover this gap at claim time.

Key signs a policy is missing this protection:

- No separate abuse/molestation sublimit listed in the declarations

- Coverage description limited to "bodily injury" and "property damage" only

- No defense cost provisions for unsubstantiated allegations

Conclusion

Home daycare insurance costs range from a few hundred dollars for a basic homeowners endorsement to over $2,000 for a comprehensive commercial package. The right coverage isn't the cheapest option — it's the one that fits what you're actually running.

Knowing the key coverage types and the factors that move your premium helps you budget accurately and avoid gaps. The main components to account for:

- General liability and professional liability for incident and negligence claims

- Abuse and molestation coverage — often excluded from standard policies

- Business property for equipment and supplies used in your care space

- Workers' comp if you employ assistants

Pricing shifts based on enrollment size, location, number of employees, and claims history. Get those variables clear before you shop, and you'll be comparing quotes on an even footing.

Frequently Asked Questions

How much does insurance cost for an in-home daycare?

Typical annual costs range from roughly $400 for a basic homeowners endorsement to $2,000+ for a comprehensive standalone commercial policy. The exact figure depends on coverage type, number of children, location, and whether you have employees. See the pricing section above for a full breakdown by policy tier.

What type of insurance do daycares need?

The core coverage types are general liability, professional liability (E&O), business property, abuse and molestation, and workers' compensation if you have employees. Most states require general liability at minimum for licensed home daycares, but relying on GL alone leaves significant gaps.

Does homeowners insurance cover a home daycare?

Standard homeowners insurance does not cover commercial activities, including home daycare operations. Some insurers offer a home-business endorsement with limited coverage, but these typically exclude professional liability, abuse and molestation, and workers' compensation. They may also fall short of state licensing requirements.

Is home daycare insurance required by law?

Most states require at least general liability insurance for licensed home daycare providers. Requirements vary — Texas mandates $100,000 per occurrence, while other states set different minimums. Check your state's childcare licensing agency for the specific mandates that apply to your operation.

How can I lower my home daycare insurance costs?

Several practical steps can reduce your premium:

- Choose a higher deductible to lower your annual cost

- Maintain a clean claims history over time

- Complete formal childcare training or certifications

- Keep enrollment small enough to avoid hiring staff

- Compare multiple carrier quotes through a specialized brokerage in one application