Introduction

Restaurants run on open flames, extreme-temperature equipment, continuous plumbing and electrical systems, and perishable inventory that can represent thousands of dollars on any given day. Few businesses carry that combination of physical risk under one roof.

A single kitchen fire, burst pipe, or equipment failure can trigger losses ranging from tens of thousands to hundreds of thousands of dollars — enough to force a temporary closure or permanent shutdown.

Commercial property insurance (CPI) is designed to protect these physical assets — the building structure, specialized equipment, contents, and even lost income during forced closures. However, coverage varies significantly depending on policy structure, endorsements chosen, and whether the restaurant owner understands critical details like the 80% coinsurance rule.

This guide breaks down what a standard restaurant CPI policy actually covers, which add-ons are worth considering, the exclusions owners most commonly miss, and how the coinsurance rule affects your payout when you need it most.

TLDR: Key Takeaways

- Restaurant commercial property insurance covers the building (if owned), business personal property, tenant improvements, and business interruption

- Food spoilage, equipment breakdown, and outdoor property coverage require separate add-ons

- Standard policies exclude flood, sewer backup, wear and tear, employee theft, and liquor liability

- The 80% coinsurance rule can significantly reduce your claim payout if you underinsure your property value

What Does Commercial Property Insurance Cover for a Restaurant?

A standard commercial property insurance policy for a restaurant covers physical damage to property caused by named perils—typically fire, wind, hail, lightning, burst pipes, accidental water discharge, theft, and vandalism. Understanding exactly what falls under each category is critical for restaurant owners, especially given that cooking equipment causes 59% to 61% of all restaurant building fires.

Building Structure Coverage

If the restaurant owns its building, CPI covers damage to the structure itself:

- Walls, roof, and foundation

- Permanently installed HVAC systems

- Electrical wiring and plumbing

- Fire suppression systems (essential in commercial kitchens)

Structural coverage applies to covered perils only—not every event that damages the building. Fire is the most relevant example for restaurants given kitchen fire risk. U.S. fire departments respond to an estimated 5,900 restaurant building fires annually, resulting in $172 million in direct property damage. When fires escape the cooking area, average losses jump to $59,000 per incident, compared to just $840 for confined fires.

Other common structural claims include wind, hail, and burst pipes.

Business Personal Property (BPP)

BPP often represents the highest dollar value for restaurants. It covers movable items inside the building the business owns:

- Commercial ovens, grills, fryers, and ranges

- Walk-in coolers and freezers

- Refrigeration units and ice machines

- Prep tables and commercial mixers

- Point-of-sale systems and computers

- Tables, chairs, and bar fixtures

- Food and beverage inventory

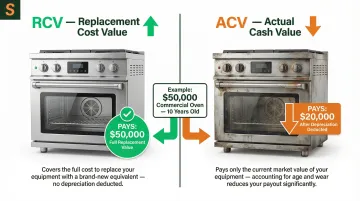

Critical distinction: Replacement Cost Value (RCV) vs. Actual Cash Value (ACV)

- RCV pays to replace the item new, without deducting depreciation

- ACV pays replacement cost minus depreciation based on age and wear

For restaurants with older but still functional commercial equipment, ACV payouts can be significantly lower than replacement cost—leaving owners thousands of dollars short at claim time. Average kitchen equipment costs range from $30,000 to $150,000+, so the RCV vs. ACV choice carries real financial weight.

Tenant Improvements and Build-Outs

Many restaurants lease their space and invest heavily in custom build-outs:

- Built-in bar areas

- Permanently installed kitchen hoods

- Custom flooring and tile work

- Interior partitions and decorative millwork

- Commercial-grade ventilation systems

These "tenant improvements and betterments" are typically the tenant restaurant's responsibility to insure, not the landlord's. Disputes can arise when a loss occurs and the insurer questions ownership of improvements—the lease agreement usually governs this.

Franchise restaurant operators may face additional insurance requirements from the franchisor that dictate what improvements must be covered and at what limits.

Business Interruption Insurance

Beyond physical property, protecting your revenue stream matters just as much. Business interruption (BI) coverage activates when a covered physical loss forces the restaurant to temporarily close or relocate, compensating for:

- Lost net income during the restoration period

- Ongoing fixed expenses like rent and utilities

- Payroll for retained employees

BI coverage is high-stakes for restaurants because thin operating margins leave little buffer. A forced closure of even 4–8 weeks can wipe out months of profit. Standard policies offer 12 months of coverage, but claims experts warn this is rarely enough for major rebuilds given supply chain and permit delays. Extended Period of Indemnity endorsements pushing coverage to 18 or 24 months are strongly recommended.

One important restriction: BI only triggers after covered physical damage. Closures due to pandemics or government orders are excluded unless specifically endorsed.

Restaurant-Specific Add-On Coverages Worth Considering

While building, BPP, and BI form the core of a standard restaurant CPI policy, several important coverages are not automatic and require specific endorsements. Failing to add these is one of the most common and costly gaps restaurant owners face.

Food Spoilage Coverage

Food spoilage coverage protects against financial loss when refrigerated or frozen inventory is lost due to equipment failure or a power outage caused by a covered peril. Without this endorsement, a refrigeration failure that wipes out thousands of dollars of inventory may not be covered.

Key details:

- Typically has its own sub-limit (often just $1,000-$2,500 by default)

- A single weekend cooler breakdown can result in $2,500 to $18,000+ in lost inventory

- May require documented equipment maintenance

- Adjust limits to match peak seasonal inventory values

Equipment Breakdown Coverage

Standard CPI does not cover internal mechanical or electrical failure—it only covers external damage from covered perils. Equipment breakdown coverage (sometimes called "boiler and machinery" coverage) steps in where standard CPI stops, covering events like:

- Refrigeration compressor failure

- Boiler malfunction

- Electrical panel short

- Motor burnout

For a busy restaurant, the financial impact extends well beyond repair costs to spoilage and lost revenue. The average restaurant equipment breakdown costs nearly $5,000, but major failures can reach $200,000 to $223,000 for refrigeration and electrical equipment.

Outdoor Property and Signage

Restaurants often invest in exterior signage, patio furniture, fencing, awnings, and outdoor lighting. Standard CPI may provide limited coverage for outdoor property, often at significantly lower sub-limits than the main building.

Common risks that expose this gap include:

- Wind and hail damage to awnings, signage, and fencing

- Snow load collapse of patio structures

- Theft or vandalism of outdoor furniture and lighting

Restaurant owners often assume outdoor items are fully covered under the building limit — they frequently are not. Check your outdoor property sub-limits and increase them to reflect what you've actually invested in your exterior.

What Commercial Property Insurance Does NOT Cover

Many restaurant claims are denied or reduced because owners assumed coverage existed for a peril that's actually excluded. Knowing what's left out is just as critical as knowing what's covered.

Flood and Water-Related Exclusions

Standard commercial property insurance typically excludes flood damage from rising water—a separate flood insurance policy (often through the NFIP or a private insurer) is required. Sewer backup is also excluded unless you add a specific endorsement.

Restaurants near waterways, coastal areas, or in flood-prone zones are especially at risk of being caught without this coverage.

Gradual Deterioration and Maintenance Issues

Damage from gradual wear and tear, deferred maintenance, or slow deterioration is not covered. Insurers frequently argue that damage resulted from pre-existing deterioration rather than a sudden covered event. It's one of the most common sources of restaurant property insurance disputes.

Action step: Regular equipment maintenance and documentation can both reduce risk and support a claim if one arises.

Other Common Exclusions

Standard commercial property insurance typically excludes:

- Employee theft — add a crime coverage endorsement to close this gap

- Liquor liability claims — requires a standalone liquor liability policy

- Customer bodily injury — falls under general liability, not property coverage

- Earthquake and earth movement damage — requires separate coverage in most states

- Ordinance or code upgrade costs — often needs its own endorsement when local codes require upgrades during repairs

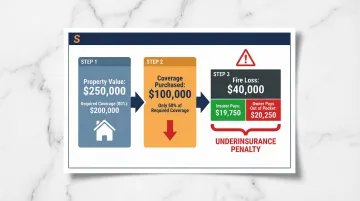

The 80% Coinsurance Rule: Why It Matters for Restaurant Owners

Most commercial property policies require that the insured carry coverage equal to at least 80% of the property's full replacement cost value. If a restaurant owner insures the property for less than 80% of its actual value to save on premiums, and then files a claim, the insurer may only pay a proportional share of the loss—even if the damage is far below the coverage limit.

How the Math Works

Imagine a restaurant with a true replacement value of $250,000, an 80% coinsurance requirement, and a $250 deductible. The owner, trying to save money, only buys $100,000 in coverage. A kitchen fire causes $40,000 in damage.

| Metric | Calculation | Amount |

|---|---|---|

| Actual Replacement Value | Appraised value of property | $250,000 |

| Coinsurance Requirement | 80% of $250,000 | $200,000 (minimum required) |

| Actual Limit Purchased | Chosen by the insured | $100,000 (only 50% of required) |

| Fire Damage (Loss) | Cost to repair | $40,000 |

| Insurance Payout | ($100,000 / $200,000) × $40,000 - $250 | $19,750 |

| Out-of-Pocket Penalty | $40,000 - $19,750 | $20,250 |

Buying half the required coverage means collecting half the claim. That $20,250 gap comes directly out of the restaurant's pocket — on a loss that insurance should have fully covered.

Why This Is Particularly Risky for Restaurants

Equipment values can be substantial and change over time as new appliances are added. Many restaurant owners set their coverage limits at the time of opening and never revisit them. According to a 2025 Hiscox report, 77% of U.S. small businesses are underinsured, and 67% lack extended replacement cost coverage to account for inflation — a gap that hits restaurants especially hard as equipment costs rise.

Annual Check: Review your property valuation each year to confirm your coverage limit still meets your policy's coinsurance requirement — especially after adding equipment or renovating.

Factors That Affect Your Restaurant's Commercial Property Insurance Cost

Several factors influence restaurant commercial property insurance premiums. Understanding them helps you anticipate costs and identify where risk management can reduce what you pay.

Key rating factors include:

- Location: Urban areas with higher crime or fire risk cost more; coastal or flood-prone zones carry surcharges; proximity to fire stations affects rates

- Building characteristics: Older buildings and wood-frame construction carry higher premiums than fire-resistive concrete or steel; maintenance history matters

- Equipment and inventory value: High-value kitchen equipment, cooking method type, and inventory turnover all factor into your rate

- Claims history: Prior claims — especially frequent or high-severity losses — increase future premiums

Beyond physical risk factors, the coverage structure you choose has a direct impact on your premium.

How Coverage Choices Affect Cost

Industry data shows average annual costs:

- Business Owner's Policy (BOP): ~$3,010 (combines property and general liability)

- Standalone Commercial Property: ~$740 to $2,500

- General Liability: ~$900 to $1,691

Higher coverage limits and lower deductibles increase premiums, while opting for actual cash value instead of replacement cost lowers them (but increases out-of-pocket risk). Add-on endorsements like equipment breakdown, food spoilage, and ordinance/law coverage also affect total premium.

Risk Management Steps That Can Lower Premiums

- Install monitored fire suppression and alarm systems — NFPA data shows wet pipe sprinklers reduce direct property damage by 75%, and carriers typically offer 5%–15% premium discounts for fully compliant systems

- Maintain UL-300 compliant automatic fire extinguishing systems over hoods and deep fryers; most carriers require these, and failure to comply can result in policy cancellation or denied claims

- Document equipment maintenance on a regular schedule — detailed records help validate claims and reduce disputes with adjusters

- Follow proper food storage and inventory practices to lower spoilage risk and show operational controls to underwriters

- Train staff on safety procedures consistently to reduce accident frequency and claims severity

How to Make Sure Your Restaurant Is Properly Covered

No two restaurant insurance policies are identical—the right coverage depends on several factors specific to your operation:

- Whether you own or lease the building

- The type of cuisine and cooking methods used

- Equipment values and recent renovations

- Location and local risk factors

- Whether the restaurant is independently owned, a franchise, or part of a chain

Working with a specialist broker who understands restaurant-specific risks is critical to getting the right structure. Generic commercial brokers often lack the carrier relationships and underwriting expertise needed to properly place hospitality risks.

Restaurant owners should also review coverage limits regularly as their business grows. Adding equipment, expanding into outdoor dining, or renovating increases insurable property value and may require limit adjustments to stay compliant with coinsurance requirements (the minimum coverage ratio your policy mandates). Industry data suggests roughly 40% of insureds who completed renovations failed to update their insurance to reflect the new property value.

Soma works with restaurant owners across independent, franchise, and chain operations to place coverage through specialty carriers like Markel, Nationwide, and Liberty Mutual. Their hospitality program covers restaurant-specific exposures — food spoilage, equipment breakdown, liquor liability, and business interruption — and is structured to get restaurant owners quoted and covered without delays.

Frequently Asked Questions

What insurance do I need for my restaurant?

Restaurants typically need commercial property insurance, general liability, workers' compensation, and — depending on the operation — liquor liability, food spoilage, and business interruption coverage. Most of these are bundled in a Business Owner's Policy (BOP) designed for restaurants.

What is not typically covered by commercial property insurance?

Standard CPI typically excludes flood damage, sewer backup, gradual wear and tear, employee theft, liquor liability claims, and customer bodily injury. Covering any of these gaps requires a separate policy or a targeted endorsement added to your existing coverage.

What is the 80% rule in property insurance?

The 80% coinsurance rule requires restaurant owners to carry coverage equal to at least 80% of the property's full replacement cost. Failing to meet this threshold means the insurer may only pay a proportional share of any claim, even if the loss is smaller than the policy limit.

Does commercial property insurance cover food spoilage at a restaurant?

Food spoilage is not automatically included in a standard CPI policy—it typically requires a specific endorsement. When included, it covers inventory lost due to refrigeration equipment failure or power outages caused by a covered peril, often with a sub-limit between $10,000 and $25,000.

Do I need separate flood insurance for my restaurant?

Yes, standard commercial property policies exclude flood damage from rising water. Restaurants in flood-prone areas, near waterways, or in coastal zones should obtain a separate flood insurance policy through the NFIP or a private carrier.

What's the difference between replacement cost and actual cash value for restaurant equipment?

Replacement cost value (RCV) pays to replace damaged equipment with new comparable items, while actual cash value (ACV) deducts depreciation. For restaurants with older but high-value equipment, the depreciation deduction under ACV can leave a substantial coverage gap at claim time.