Daycare insurance costs vary significantly based on which policies you carry, your enrollment size, the age groups you serve, and where you operate. This article covers real cost ranges by coverage type, what each tier includes, the factors that push premiums up or down, and how to build a budget that actually protects your operation.

Key Takeaways

- A commercial daycare center typically pays between $3,000 and $15,000+ per year across all necessary coverage lines

- General liability is the foundation — but professional liability, abuse & molestation coverage, and workers' comp are non-negotiable additions

- Enrollment size, age groups served, location, and transportation services are the biggest cost drivers

- Underinsuring to cut costs is the most expensive mistake daycare operators make — a single uncovered claim can shut a center down

How Much Does Daycare Center Insurance Cost?

There's no single price for daycare center insurance. Total cost depends on how many coverage types you carry, how large your facility is, what services you offer, and which state you operate in.

Home-based daycare providers typically pay $1,000–$2,500 per year for a basic coverage package. Licensed commercial daycare centers generally pay $3,000–$15,000 or more annually once all necessary lines are in place — general liability, professional liability, abuse & molestation, workers' comp, and property.

The gap between those two figures isn't arbitrary. Commercial centers carry more children, employ more staff, operate under stricter licensing requirements, and face significantly higher claim severity across every exposure category.

The Cost of Getting It Wrong

Operators who purchase only general liability often discover this the hard way: professional negligence claims, abuse allegations, and employee injuries fall entirely outside GL coverage. Out-of-pocket legal defense costs alone can exceed six figures. For most centers, an uninsured six-figure defense bill means closing permanently.

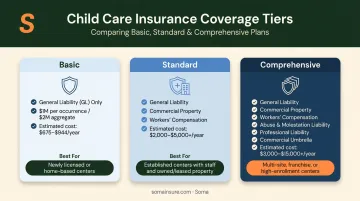

Coverage Package Tiers

| Package | What's Included | Typical Annual Cost | Best For |

|---|---|---|---|

| Basic | General liability only ($1M/$2M limits) | ~$675–$944/year* | Newly licensed centers meeting state minimums only |

| Standard | GL + commercial property + workers' comp | $2,000–$5,000+ | Centers with employees and a leased/owned facility |

| Comprehensive | GL + professional liability + workers' comp + property + abuse & molestation + optional auto, cyber, umbrella | $3,000–$15,000+ | Established centers with multiple staff, infants, or transportation |

*Mixed home/commercial daycare sample from NEXT Insurance's 2022 customer data. Commercial-center-only figures will vary.

Most licensed centers with employees and a physical facility should target the comprehensive tier. The coverage gaps in Basic and Standard packages only become apparent after a claim — at which point the out-of-pocket exposure is already locked in.

What Insurance Does a Daycare Center Need?

Daycare centers face a distinct set of risks that standard business policies aren't built for. Here's what a complete protection plan looks like.

General Liability Insurance

General liability (GL) is the foundation every daycare policy builds from. It covers:

- Third-party bodily injury (a child hurt on your premises)

- Property damage caused by your operations

- Reputational harm claims

Most states require a minimum GL limit as a condition of licensing — though those minimums vary. Tennessee, for example, requires $500,000 per occurrence / $500,000 aggregate. Texas sets its minimum at $100,000 per occurrence effective January 1, 2026. Neither matches the commonly referenced $1M/$2M standard, which remains an industry recommendation rather than a universal legal floor.

Professional Liability Insurance

Also called errors & omissions (E&O), professional liability covers allegations of negligence, inadequate supervision, or failure to meet professional care standards. These claims fall entirely outside general liability coverage.

This matters most for centers with structured curricula, infant care programs, or Montessori-style instruction — anywhere a parent could argue that a professional standard of care wasn't met. Budget roughly $99/month as a general reference point, though commercial center rates vary based on enrollment and services.

Abuse & Molestation Coverage

Most GL policies explicitly exclude abuse and molestation claims via standard exclusion endorsements like ISO form CG 21 46. Yet allegations of physical, emotional, or sexual misconduct represent one of the costliest exposures in childcare — both financially and reputationally.

This standalone coverage — or endorsement, depending on the carrier — pays legal defense costs and settlements regardless of whether a claim has merit. Even defending a false allegation can cost tens of thousands before a case resolves.

Selective Insurance, for instance, offers abuse & molestation limits up to $1M per occurrence / $3M policy life, though premiums vary by state and risk profile.

Workers' Compensation Insurance

Workers' comp is legally required in nearly every state for businesses with employees. Childcare work involves constant physical handling — lifting infants, repositioning toddlers — making it a frequent source of claims.

Premiums are calculated per $100 of payroll, and class codes make a significant difference. New York's 2025 loss costs show the range clearly:

| Class Code | Description | Loss Cost per $100 Payroll |

|---|---|---|

| 8869 | Child Day Care | $0.63 |

| 9059 | Day Care Center | $6.42 |

Final premiums depend on your state, carrier multipliers, and experience rating.

Additional Coverages Worth Considering

| Coverage | When You Need It | What It Covers |

|---|---|---|

| Commercial Property | Leased or owned facility | Building, equipment, supplies against fire, theft, damage |

| Commercial Auto | If you transport children | Owned vehicles used for pickups/dropoffs; often one of the costliest lines |

| Hired & Non-Owned Auto | Staff use personal vehicles | Liability when employees drive their own cars for center business |

| Cyber Liability | Any center storing health or payment data | Data breaches, ransomware, notification costs, regulatory defense |

| Commercial Umbrella | High enrollment, multiple sites | Excess liability above GL and professional liability limits |

| Crime/Employee Dishonesty | Centers with multiple staff | Theft or fraud by employees |

| Accident/Participant Medical | All centers | Medical costs for children injured during care |

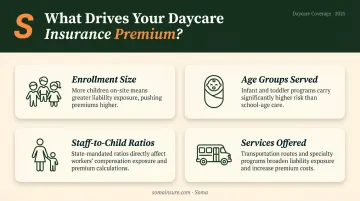

Key Factors That Affect Your Daycare Insurance Premium

Insurers evaluate a specific set of operational variables when pricing daycare coverage. Understanding what moves the needle helps you anticipate where your costs will land.

Location and State Requirements

State is one of the most impactful variables. Litigation environments, jury verdict trends, and local court costs vary significantly. A center in California or New York will generally pay more across every coverage line than an equivalent operation in a lower-litigation state. That's not just because claims cost more there — carriers set rates to account for local legal risk from the outset.

State licensing requirements add another layer. Some states mandate specific minimum liability limits as a condition of maintaining your daycare license, and those requirements differ considerably from state to state.

Enrollment Size, Age Groups, and Staff Ratios

More children means greater liability exposure and higher premiums. But age group matters as much as headcount:

- Infant and toddler programs carry higher premiums than school-age care — the supervision intensity and injury severity potential are both greater

- State-mandated staff-to-child ratios directly affect workers' comp costs by determining how many employees you're required to carry

- Enrollment growth should always trigger a policy review — coverage limits that were adequate at 30 children may be insufficient at 60

Services Offered

Each added service introduces a separately priced exposure:

- Transportation triggers commercial auto requirements — typically one of the costliest individual coverage lines

- Overnight care or field trips raise the risk profile across multiple policies

- Swimming programs add aquatic liability exposure that standard forms may not address

- Care for children with disabilities increases supervision complexity and professional liability exposure

Adding transportation to an otherwise standard daycare operation can meaningfully increase total annual premium — sometimes by several thousand dollars depending on fleet size and state requirements.

Claims History and Risk Management Practices

A single major claim — especially an abuse allegation — can raise premiums significantly at renewal or affect your ability to get coverage at all. Carriers review claims history not just at application but at every renewal.

Documented risk management practices can offset that exposure. Underwriters factor the following into their pricing decisions:

- Staff background check records

- Written supervision protocols

- Incident logs and response procedures

- Regular safety training documentation

Centers with clean multi-year histories and verifiable safety programs consistently receive better rates and more favorable policy terms. Carriers treat this documentation as evidence of reduced risk, which shows up directly in what you pay.

Full Cost Breakdown: What You're Actually Paying For

Daycare center insurance isn't a single annual bill. It's a stack of policies, each responding to a different category of risk.

| Coverage Line | Recurring or Conditional | Approximate Annual Range* | What It Covers |

|---|---|---|---|

| General Liability | Always required | ~$675–$944 (mixed sample) | Third-party bodily injury and property damage |

| Professional Liability | Recommended for all centers | ~$1,188/year average | Negligence and supervision failure claims |

| Abuse & Molestation | Required for licensed centers | Varies — obtain quotes | Allegations of physical, emotional, or sexual misconduct |

| Commercial Property | If you have a facility or equipment | ~$341–$740 (mixed sample) | Building, equipment, and supplies |

| Workers' Compensation | Required if you have employees | Payroll-based; varies by state | Employee injuries and lost wages |

| Commercial Auto | If you transport children | Varies significantly by state | Owned vehicles used to transport children |

| Cyber Liability | Recommended for all centers with digital records | Varies | Data breaches, ransomware, notification costs |

| Commercial Umbrella | Recommended for larger/multi-site centers | Varies | Excess coverage above GL/PL limits |

*Ranges from NEXT Insurance's 2022 customer data (mixed home/commercial daycare sample). Commercial-center-only figures will vary. Obtain quotes for your specific operation.

Bundling and Carrier Selection

Many insurers bundle GL and commercial property into a Business Owner's Policy (BOP), which can reduce total cost compared to purchasing them separately.

Carrier access matters just as much as bundling. Standard commercial markets frequently decline daycare accounts outright, which affects both pricing and your ability to secure the full coverage stack — particularly abuse & molestation coverage.

Soma places the complete daycare coverage stack — general liability, abuse & molestation, professional liability, workers' comp, commercial property, commercial auto, umbrella, crime, and participant medical — through a single application across its specialty childcare carrier network. One application generates bundled pricing from multiple carriers, so operators see actual rate comparisons rather than a single take-it-or-leave-it quote.

How to Budget Smartly and Avoid Common Insurance Mistakes

The most expensive mistake daycare operators make is treating general liability as the total insurance cost. GL covers bodily injury and property damage — not professional negligence, not abuse allegations, not employee injuries. A center budgeting only for GL is budgeting for one category of risk while leaving several others completely unaddressed.

A properly insured commercial daycare center should plan to spend $3,000–$15,000+ annually across all necessary lines. Operators who budget for a fraction of that are almost always carrying gaps they won't discover until a claim arrives.

Common Coverage Gaps to Avoid

- Skipping professional liability under the assumption that GL covers all claims — it doesn't

- Assuming abuse & molestation is included in the base GL policy — it usually isn't, or carries a sublimit too low to matter

- Failing to update coverage after adding staff, expanding to infant care, or introducing transportation services — all of these materially change your risk profile and require a policy review

How to Compare Quotes and Manage Costs

- Hold coverage limits constant across all quotes — the only way to compare pricing is to compare identical coverage

- Consider raising deductibles strategically if you have a clean multi-year claims history

- Ask about multi-policy discounts for bundling GL, property, and workers' comp with a single carrier

- Invest in documented risk management — safety protocols, background check records, and staff training documentation directly influence underwriting outcomes at renewal

The right insurance budget balances legal compliance, actual risk exposure, and long-term financial protection — premium price alone is a poor proxy for protection. Daycare insurance involves multiple coverage types with overlapping exclusions, and those interactions are easy to miss without a broker who places childcare coverage regularly.

Frequently Asked Questions

How much do daycares pay for insurance?

Home daycares typically pay $1,000–$2,500 per year for a basic coverage package. Commercial daycare centers generally pay $3,000–$15,000+ annually, depending on enrollment size, location, and which coverage types are carried.

What type of insurance do daycares need?

The core required and recommended policies include:

- General liability — required in most states for licensing

- Professional liability — covers errors in care and supervision

- Abuse & molestation coverage — essential for any childcare operation

- Workers' compensation — legally required once you have employees

- Commercial property insurance — protects your facility and equipment

Centers that transport children also need commercial auto coverage.

Does homeowners insurance cover an in-home daycare?

Standard homeowners insurance is not designed to cover commercial business activities, and most policies exclude home daycare operations. In-home providers need a separate business policy or a specific commercial endorsement — a homeowners policy alone will not respond to childcare liability claims.

Is workers' compensation required for daycare employees?

Workers' comp is legally required in nearly every state once you have employees. Texas and South Dakota are the notable exceptions where private employers may opt out, though coverage remains advisable in both states given the physical demands of childcare work.

What general liability limits does a daycare center need?

The industry standard recommendation is $1 million per occurrence and $2 million aggregate, though state-mandated minimums vary — Texas requires $100,000 per occurrence as of 2026, while Tennessee requires $500,000/$500,000. Higher limits typically cost only a few hundred dollars more annually, which is a reasonable tradeoff given the liability exposure in childcare.

How can a daycare center lower its insurance costs?

Compare quotes across multiple carriers using identical coverage limits, bundle policies where possible for multi-policy discounts, maintain a clean claims history, and document your safety and supervision protocols. Underwriters review these practices at renewal. Centers with strong safety records consistently receive better rates.