Costs vary based on the type of operation, the coverages selected, staff size, and state — and there's no single national average that applies cleanly across all three. What follows breaks down what daycare insurance actually costs, what drives those costs, and where most operators go wrong.

Key Takeaways

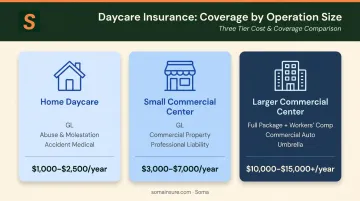

- Home daycares typically spend $1,000–$2,500 annually; commercial centers range from $3,000 to $15,000+ depending on size and coverage

- Full coverage typically combines five policy types: general liability, professional liability, property, workers' comp, and abuse & molestation

- Infant care and transportation programs are among the most expensive exposures to insure

- Homeowners insurance does not cover home daycare operations — a separate commercial policy is required

- Gaps in coverage — not premium costs — are the biggest financial risk daycare operators face

How Much Does Daycare Insurance Cost?

Daycare insurance doesn't carry a fixed price. The final premium reflects the type and scale of your operation, the coverages you select, and the state where you operate. Underwriters price each account based on distinct exposures — enrollment, payroll, property, transportation, and claims history all factor in.

The most common mistake operators make: underbudgeting on coverage, then discovering the gaps only when a claim arrives.

| Operation Type | Typical Coverages | Annual Cost Estimate |

|---|---|---|

| Home Daycare | GL, abuse & molestation, accident medical | $1,000–$2,500 |

| Small Commercial Center | GL, commercial property, professional liability | $3,000–$7,000 |

| Larger Commercial Center | Full package + workers' comp, commercial auto, umbrella | $10,000–$15,000+ |

Home Daycare

Home-based providers — sole operators caring for a small group of children — fall into the lowest cost tier. A basic program combining general liability, abuse and molestation coverage, and accident medical typically runs $1,000–$2,500 annually. Markel's in-home package, for reference, offers GL limits up to $1M per occurrence/$3M aggregate.

Small Commercial Daycare Center

Small centers with staff, moderate enrollment, and a leased or owned facility need more coverage than a home-based program. Adding commercial property and professional liability to the base GL program pushes costs higher.

A reasonable estimate for this tier runs $3,000–$7,000 annually, though final premiums depend heavily on building size, enrollment count, and state.

Larger Commercial Daycare Center

Larger centers with employees, a transportation program, and full coverage packages represent the highest cost tier. Workers' compensation alone scales with payroll. Add commercial auto, umbrella coverage, and higher liability limits, and total annual program costs can reach $10,000–$15,000 or more.

According to NAEYC's 2024 survey of 1,173 programs, 80% of childcare programs reported liability cost increases, with 13% of centers seeing increases of at least $10,000. Budget from current quotes and renewal history — not outdated averages.

Types of Daycare Insurance and Their Costs

A complete daycare insurance program is built from multiple policies, each addressing a different category of risk. Understanding what each covers — and roughly what it costs — helps you build the right package without paying for coverage you don't need.

General Liability Insurance

General liability (GL) is the foundation. It responds to third-party bodily injury and property damage claims — for example, a child injured on the premises, or a parent who slips in the parking lot.

- Home daycares: Typically included in the $1,000–$2,500 annual package

- Commercial centers: GL alone often runs $1,500–$3,500+ annually depending on enrollment and state

- Most states require GL as a condition of childcare licensing

Insureon's 2025 data for the human and social services sector reports a median GL cost of $91/month (~$1,092 annualized) — but this covers the broader sector, not daycares specifically. Use this as directional context, not a quote.

Professional Liability Insurance

Professional liability covers allegations of negligence, inadequate supervision, or failure to meet care standards. General liability explicitly excludes these claims. As operations grow and staff increases, the exposure for professional negligence grows with it.

Annual costs for the human/social services sector come in around $99/month (~$1,188 annualized) per Insureon's 2025 data. Daycare-specific pricing varies — expect higher premiums for infant care programs and centers with specialized services.

Property Insurance

Commercial property protects the building, equipment, supplies, and learning materials against fire, theft, or vandalism. Business income coverage can protect revenue lost during a covered shutdown.

Critical point for home-based providers: Standard homeowners insurance does not cover business activities. Texas Department of Insurance explicitly warns that losses related to a home daycare are not covered under homeowners policies. A separate commercial property policy — or at minimum a commercial endorsement — is necessary.

Commercial property costs vary significantly by building size, age, and location.

Workers' Compensation Insurance

Workers' comp covers employee medical expenses and lost wages from work-related injuries. The Bureau of Labor Statistics recorded 1.9 nonfatal injuries per 100 full-time-equivalent workers in child day care services in 2024 — a real and measurable exposure for an industry involving regular physical handling of children.

Pricing is payroll-based and state-specific. Workers' comp codes vary by state (New York uses class 8869; California uses 9059 for many daycare programs), and rates differ accordingly. Most states require coverage the moment a first employee is hired — California and New Jersey, for example, require it for any business with one or more employees.

Abuse and Molestation Insurance

Most daycare operators assume abuse and molestation (A&M) coverage is bundled into their GL policy. It isn't. Whether it's excluded from the GL form entirely, added as an endorsement, or placed as a separate scheduled coverage depends on the carrier and policy form.

The financial exposure is real even when allegations are unfounded — legal defense costs alone can far exceed what annual A&M coverage costs. Key things to know:

- Markel offers A&M via endorsement with separate per-person, per-occurrence, and aggregate limits

- Great American schedules A&M limits separately from both GL and professional liability

- Soma's daycare program lists A&M as a distinct coverage line — not an assumed GL inclusion

The more staff you add, the greater your exposure to a claim. Treating A&M as optional at that stage creates a coverage gap that other policies won't fill.

Additional Coverages to Consider

| Coverage | When You Need It | Approximate Annual Cost |

|---|---|---|

| Commercial Auto | If you own vehicles used to transport children | Varies by vehicle count and routes |

| Hired & Non-Owned Auto (HNOA) | Employees using personal vehicles for business purposes | Lower than commercial auto; carrier-specific |

| Commercial Umbrella | Excess liability above primary GL or auto limits | Typically $500–$2,000+ depending on underlying limits |

| Accident/Medical Coverage | Covers injury costs to children in care regardless of fault | Carrier-specific; varies by enrollment |

Key Factors That Affect Your Daycare Insurance Premium

Insurers price daycare coverage based on a specific mix of operational and location variables. Knowing which ones apply to your facility lets you anticipate your premium — and take steps to improve it before renewal.

Type of Operation and Facility

Home-based providers carry a very different risk profile than commercial centers — fewer employees, smaller premises, lower property values. Facility condition matters too. Aging infrastructure, missing fire suppression systems, unfenced play areas, and deferred maintenance all push property and GL premiums higher.

Number of Children and Age Groups Served

More enrolled children means more exposure — premiums reflect that directly. Age group is a significant underwriting variable:

- Infants and toddlers cost more to insure due to higher supervision intensity and injury severity potential

- School-age after-school programs typically carry lower premiums than infant rooms

- Standard carriers rate infant care among the hardest childcare segments to place — many decline it outright

Services Offered and Activities

Each additional service introduces a separate liability exposure:

- Transportation programs require commercial auto or HNOA coverage

- Swimming activities and field trips affect GL premiums

- Overnight care introduces extended supervision exposure

- Specialized programs for children with disabilities require careful underwriting

Carrier applications — including PHLY's public childcare submission — ask about all of these separately: enrollment by age group, operating hours, pools, transportation, and special-needs services. Each one is priced individually, which is why two centers with the same enrollment count can receive very different quotes.

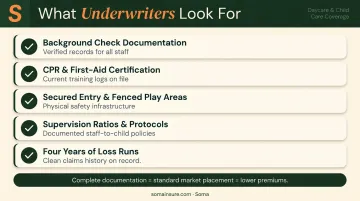

Claims History, Staff Practices, and Safety Measures

A clean claims record earns better rates over time. Underwriters also evaluate:

- Employee background check documentation

- CPR and first-aid certification for staff

- Secured entry systems and fenced play areas

- Documented supervision ratios and protocols

- Four years of loss runs (which PHLY requests in its childcare application)

Carriers use this documentation to distinguish lower-risk operations from higher-risk ones. Facilities with complete records — background checks, training logs, incident protocols — often qualify for standard market placement rather than surplus lines, which translates directly to lower premiums.

How to Lower Your Daycare Insurance Costs

Three practices consistently reduce what childcare operators pay — without cutting the protection they actually need.

Compare Quotes on Identical Coverage Limits

The widest price variation in childcare insurance shows up in professional liability and abuse and molestation (A&M) coverage, where carrier appetite differs significantly. Comparing a $1M A&M limit from one carrier against a $300K limit from another isn't comparing prices — it's comparing different products. Use identical limits across every quote, or the lowest number will always look cheapest.

Bundle Policies With One Carrier

Combining GL, property, and professional liability with one carrier often reduces total premium without changing the coverage structure. Soma's daycare insurance platform works from a single application with ratio- and enrollment-based underwriting, giving childcare operators access to specialty carriers across the market — without filing separate applications to each carrier.

Review Coverage at Every Renewal

Many operators overpay by carrying coverage built around past operations. Common examples:

- Paying for commercial auto after a transportation program ended

- Rated enrollment units that don't reflect current headcount

- Umbrella limits sized for a larger facility than you now operate

An annual coverage review against actual operations is the simplest way to eliminate unnecessary cost.

What Most Daycare Owners Get Wrong About Insurance Costs

Focusing only on the upfront premium. The cheapest policy typically comes with lower coverage limits, exclusions for abuse allegations, or deductibles that create serious out-of-pocket exposure when a claim hits. The cost difference between $300,000 and $1 million in liability coverage is usually a few hundred dollars annually — the protection gap is far larger.

Assuming homeowners insurance covers a home daycare. It doesn't — and Texas and Maryland regulators explicitly warn home-based providers not to rely on standard homeowners policies for paid childcare activities. Some carriers offer endorsements, but these carry low limits and leave critical risks, particularly abuse and molestation, entirely uncovered.

A separate commercial policy is necessary. Soma places commercial coverage specifically for in-home and family daycare operators, including providers who've been told the standard market won't write their risk.

Underestimating the cost of skipping abuse and molestation coverage. A&M is consistently excluded from — or separately limited in — standard GL policies, yet it represents one of the highest-cost exposures in childcare. A single allegation, regardless of merit, can generate legal fees that dwarf the annual premium for dedicated A&M coverage. Waiting until the operation grows to add it is a risk no daycare can afford to take.

Conclusion

Daycare insurance costs vary significantly based on operation type, coverages selected, children served, and state. Home-based providers and large commercial centers face fundamentally different cost structures — but both share the same core risk categories: liability, professional negligence, property, worker safety, and abuse exposure.

The right premium buys adequate protection across all five risk categories — not just the cheapest number on a quote sheet. Gaps in coverage tend to surface at the worst possible moment, and the cost of an uncovered claim will far exceed any premium saved.

Three practices keep daycare operators in control of cost without sacrificing protection:

- Understand each coverage component before comparing quotes — identical-sounding policies can carry very different exclusions

- Get quotes on equivalent terms so you're comparing actual coverage, not just price

- Review your program annually as enrollment, staff count, and state requirements change

Frequently Asked Questions

How much is daycare insurance?

Home daycares typically pay $1,000–$2,500 annually for a basic program including general liability and abuse and molestation coverage. Commercial daycare centers generally range from $3,000 to $15,000+ depending on enrollment, staff size, services offered, and state. The final premium depends on which coverage types are included and how the operation is structured.

What type of insurance do daycares need?

The core program includes general liability, professional liability, commercial property, workers' compensation, and abuse and molestation coverage. Commercial auto is required if children are transported, and a commercial umbrella adds excess liability protection above primary limits.

Does homeowners insurance cover a home daycare?

No. Standard homeowners policies explicitly exclude business activities, and regulators in multiple states — including Texas and Maryland — warn home-based providers not to rely on them. A separate commercial policy is almost always required, and even endorsements often carry limits too low for full-time providers.

What is the minimum liability coverage required for a daycare?

State requirements vary. Maine requires centers to carry $100,000 per person/$300,000 per occurrence; California family homes may carry $100,000 per occurrence/$300,000 aggregate or meet alternative requirements. A practical baseline is $1 million per occurrence and $2 million aggregate as a practical baseline.

How can I lower my daycare insurance premiums?

Compare quotes using identical limits and deductibles, bundle policies with one carrier, keep a clean claims record, and document safety practices like background checks and CPR certification. A specialty broker who accesses multiple carriers through one application can also find better rates.

Do I need daycare insurance if I only care for a few children?

Most states require coverage even for small home daycares caring for one or two unrelated children for payment, and the liability exposure from even a single incident makes basic coverage a necessary investment regardless of operation size. The premium for a small home daycare is low relative to the financial risk of operating without it.