Introduction

The average data breach now costs businesses $4.4 million globally, according to IBM's 2025 Cost of a Data Breach Report. For many businesses, that single incident is enough to force closure.

Most business owners assume their existing policies cover cyber incidents — they don't. Standard commercial liability policies commonly exclude electronic data losses, and property insurance requires physical damage to trigger a claim.

A ransomware attack that shuts down operations for a week? That's not covered.

This guide breaks down cyber liability insurance:

- What it is and how it differs from standard coverage

- What it covers (and what it doesn't)

- Who needs it and why

- What it costs and how to choose the right limits

Key Takeaways

- Standard business insurance policies exclude most cyber incidents — a separate policy is essential

- Covers your own recovery costs and third-party claims from affected customers

- 41% of small businesses experienced a cyberattack in 2023, making this a mainstream risk, not just a concern for large enterprises

- Small businesses pay a median of $129/month for coverage

- Common exclusions include acts of war, insider fraud, and pre-existing breaches — read the fine print

What Is Cyber Liability Insurance?

Cyber liability insurance — also called cybersecurity insurance — is a specialized policy that covers financial losses resulting from cyberattacks, data breaches, and related digital threats. The Insurance Information Institute defines it as "a policy that covers expenses and responsibilities arising from cyberattacks or computer incidents."

It exists because standard policies weren't built for digital risk. A commercial general liability policy typically contains electronic data exclusions. A property policy responds to physical loss — not a network outage caused by malware. Cyber liability steps in where those policies stop.

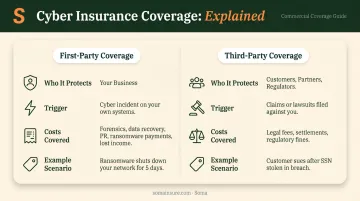

First-Party vs. Third-Party Coverage

All cyber liability policies fall into two broad categories:

- First-party coverage pays for your own recovery costs after an incident — think forensic investigation, data restoration, and lost income

- Third-party coverage protects you when customers or partners file claims or lawsuits because their data was compromised

Most standalone cyber policies include both. The balance between them — and the sublimits on each — is where policies differ meaningfully.

What Does Cyber Liability Insurance Cover?

Coverage varies by carrier, policy form, and endorsement. Here's what the major components look like in practice.

First-Party Coverage

This pays for expenses your business incurs directly after a cyber incident:

- Forensic investigation — identifying how the breach occurred and what was accessed

- Data recovery and restoration — rebuilding or recovering corrupted or stolen data

- Customer notification costs — legally required in most states after a breach involving personal data

- Crisis management and PR — managing reputational fallout

- Business interruption — lost income while systems are down following a covered event

- Ransomware/extortion payments — funds paid to attackers, plus negotiation costs

IBM's 2024 data puts average notification costs at $370,000 and detection and forensic escalation costs at $1.48 million per breach. Those figures alone can exceed what many small and mid-size businesses carry in reserves.

Third-Party Coverage

This protects you when others come after you following an incident:

- Legal defense fees if customers or partners sue

- Court judgments and settlements

- Regulatory investigation costs and fines (where insurable by law)

- Costs related to payment card industry (PCI) contractual liabilities

For businesses handling health data, look for policies that explicitly cover privacy liability tied to regulatory investigations — a key detail for HIPAA-regulated organizations that standard forms sometimes omit.

Additional Coverage Types

Many policies also include:

- Dependent business interruption — covers losses when a vendor's system failure cascades into your operations

- Privacy liability — addresses class-action exposure and regulatory penalties under state and federal privacy laws

- Media liability — covers intellectual property and advertising-related claims

- Errors and omissions — relevant for tech companies where a service failure leads to a client claim

- Cyber extortion — ransom negotiation costs beyond the payment itself

First-Party vs. Third-Party Coverage at a Glance

| First-Party | Third-Party | |

|---|---|---|

| Who it protects | Your business | Customers, partners, regulators |

| What triggers it | A cyber incident affecting your systems | Claims or lawsuits filed against you |

| Common costs covered | Forensics, data recovery, PR, ransom, lost income | Legal fees, settlements, regulatory fines |

| Example scenario | Ransomware shuts down your network for 5 days | A customer sues after their SSN is stolen in your breach |

What Cyber Liability Insurance Does NOT Cover

Knowing the exclusions is just as important as knowing what's included. Most policies exclude:

- Intentional or fraudulent acts by the business owner or employees

- Poor security hygiene — if a breach traces to known unpatched vulnerabilities, carriers may limit or deny coverage

- Insider theft — an employee deliberately stealing data is often excluded if a company executive had reason to know about the conduct

- Pre-existing events — incidents that occurred before the policy's retroactive date aren't covered

- Prior knowledge — if you knew about a breach or potential claim before binding the policy, it's excluded

- System upgrade costs — improving your infrastructure after an incident is generally not a covered expense

A "security failure" can simultaneously be a covered cause of loss under one provision and an excluded cost under another. Reed Smith's analysis of cyber policy exclusions notes that "failure to maintain security measures" clauses can limit coverage in ways that aren't obvious at first read — a distinction that often surfaces only after a claim is filed.

The practical step: review exclusions with a broker before binding. Some carriers offer endorsements — including prior acts coverage — that close common gaps. Ask specifically which exclusions apply to your industry and what it would cost to add back the coverage you need.

Who Needs Cyber Liability Insurance?

Any business that collects, stores, or transmits sensitive information should consider this coverage. That means customer names, Social Security numbers, credit card data, medical records, financial account details, and employee HR records — any of which can trigger regulatory liability if exposed.

High-Risk Industries

Some sectors face elevated exposure due to regulatory requirements or the volume of sensitive data they handle:

- Healthcare — HIPAA-regulated patient data; 710 breaches affected over 61 million individuals in 2025 alone

- Financial services — account data, investment records, PCI-DSS compliance requirements

- Technology — SaaS platforms, software developers, and IT consultants handling client systems and code

- Retail — payment card data, e-commerce customer information

- Professional services — law firms, accounting firms, and HR consultants managing confidential records

Small Businesses Are Not Off the Hook

Small businesses are just as exposed as large enterprises — often more so. According to the SBA, 41% of small businesses experienced a cyberattack in 2023. Attackers target smaller firms precisely because their security infrastructure tends to be thinner.

Contractual and Regulatory Triggers

Beyond risk management, some businesses are required to carry cyber liability coverage:

- Technology consultants may need a policy to sign a client contract

- Venture-backed startups are increasingly required by investors to carry cyber coverage before or shortly after funding closes

- Healthcare providers may face contractual requirements from payers or health system partners

If any of these triggers apply to your business, a broker with access to multiple carriers — including Chubb, Hiscox, Kinsale, Liberty Mutual, and Markel — can match your industry's specific exposure to the right policy form without requiring you to approach each carrier separately.

How Much Does Cyber Liability Insurance Cost?

What Drives the Premium

Insurers evaluate several factors when pricing a cyber liability policy:

- Type and volume of sensitive data stored or processed

- Industry — healthcare and financial services typically pay more due to regulatory exposure

- Revenue and business size

- Existing security controls — multi-factor authentication, encryption, employee training

- Claims history

- Coverage structure — standalone policy vs. BOP endorsement

What Small Businesses Actually Pay

Insureon's 2026 benchmark data puts the median cost for small businesses at $129 per month ($1,552 annually), based on policies purchased by more than 100,000 small-business customers. That figure covers a wide range — businesses with more data, higher revenue, or weaker security controls will pay more.

IBM's 2024 research puts the average cost per compromised record at $169. A business holding 50,000 customer records faces a potential breach exposure of over $8 million — before legal fees or regulatory fines enter the picture. A $1 million policy limit leaves a significant gap for that kind of exposure.

Standalone Policy vs. BOP Add-On

The Insurance Information Institute notes that some insurers include cyber coverage within a Business Owner's Policy, but BOP-based cyber typically addresses a narrower range of threats than a standalone policy. For businesses in regulated industries or those holding large volumes of sensitive data, a standalone policy is the better fit — it covers a broader threat landscape and offers higher, more flexible limits.

Getting Quotes Without the Runaround

Finding the right coverage at the right price requires comparing multiple carriers — their forms, sublimits, and exclusions differ in ways that matter. Soma's single-application process gives businesses access to competitive cyber liability quotes across hundreds of carrier partners — including Chubb, Liberty Mutual, Markel, and Nationwide — so you can compare options and move forward without the back-and-forth.

Frequently Asked Questions

What is cyber liability insurance?

Cyber liability insurance is a policy that covers financial losses from cyberattacks and data breaches, including costs like forensic investigations, data recovery, legal fees, and customer notifications. Standard business insurance policies typically exclude these expenses.

Is cyber liability insurance necessary?

For most businesses storing customer data, operating in regulated industries, or contractually required to carry it, cyber coverage is a practical necessity. A single breach can easily cost more than several years of premiums — and that's before factoring in legal exposure or regulatory fines.

What does cyber liability insurance cover?

Policies cover first-party costs (forensic investigation, data recovery, ransomware payments, business interruption, PR) and third-party costs (legal fees, settlements, regulatory fines) resulting from a covered cyber incident.

What is not covered by cyber liability insurance?

Most policies exclude intentional acts, incidents caused by known unpatched vulnerabilities, prior breaches, insider theft where executives had prior knowledge, and costs to upgrade technology systems after an incident.

What is the difference between first-party and third-party cyber coverage?

First-party coverage pays for your business's own recovery expenses after an attack. Third-party coverage pays legal costs and settlements when customers or partners bring claims against your business as a result of the incident.

How much does cyber liability insurance typically cost for small businesses?

The median is approximately $129 per month for small businesses, according to Insureon's 2026 data. Final premiums depend on your industry, revenue, data volume, security controls, and the coverage limits you select.