The gap is rarely obvious upfront. A certificate of insurance looks complete. Coverage appears active. The problem surfaces after a guard physically removes someone, a detention goes wrong, or a bystander is injured during a confrontation — and the carrier denies the claim under an assault and battery exclusion buried in the policy language.

This article covers what assault and battery insurance actually is, why standard GL policies frequently fail security companies, what A&B coverage includes and excludes, and how to confirm your policy responds when you need it.

TL;DR

- Most GL policies exclude A&B outright, leaving security companies with zero coverage for their most predictable claim type

- A&B coverage applies regardless of whether a guard was the aggressor, acted in self-defense, or failed to prevent violence

- Unarmed security companies face real A&B exposure — excessive force and wrongful detention claims don't require a weapon

- Client contracts for apartments, bars, events, and retail frequently require A&B coverage with specific limits and additional insured wording

- Verify A&B coverage is explicitly confirmed by a broker who specializes in security operations — not just assumed

What Is Assault and Battery Insurance?

Assault is an intentional act that causes someone to fear imminent harm. Battery is actual physical contact. Assault and battery insurance is a liability coverage that responds when claims arise from either — whether a guard initiated contact, acted defensively, or is alleged to have failed to stop violence from occurring.

A&B coverage doesn't just protect companies from "bad guard" scenarios. It also covers:

- Guards who used force and believed it was justified

- Allegations that a guard's actions escalated rather than resolved an incident

- Claims that the company's negligent hiring, training, or supervision enabled an altercation

- Failure-to-prevent claims where no guard action occurred at all

How A&B Coverage Is Structured

A&B coverage typically appears in one of three forms:

- Endorsement on a GL policy — Added to an existing general liability policy, often with a sublimit that caps how much the insurer will pay on A&B claims

- Standalone A&B policy — A dedicated policy that covers only assault and battery exposures, with its own limits and terms separate from GL

- Absent entirely — The GL policy carries a full A&B exclusion, and no separate coverage fills the gap — leaving the company exposed

The critical issue: a certificate of insurance won't tell you which situation applies. The full policy and endorsements must be reviewed. A security company can receive a COI showing active GL coverage and still have no A&B protection whatsoever.

A&B coverage exists in hospitality, retail, and property management — but those industries face physical confrontation as an occasional risk. For security companies, it's a foreseeable, recurring part of daily operations. That distinction shapes how carriers underwrite the coverage and why standard GL policies often exclude it by default for security firms.

Why Standard GL Policies Often Leave Security Companies Exposed

General liability insurance is built around accidental third-party bodily injury and property damage. Physical confrontation — even lawful physical confrontation — sits in different territory.

The ISO CGL endorsement CG 40 51 01 26 (2025) excludes bodily injury, property damage, and personal and advertising injury arising from actual, alleged, or threatened assault or battery. That exclusion covers anyone — not just the guard who threw a punch. It also reaches acts connected to the prevention or suppression of assault or battery, plus negligent hiring, training, supervision, and retention tied to excluded conduct. That's nearly every allegation a security company is likely to face.

Insurance Journal has reported that many commercial GL policies include explicit A&B exclusions, sometimes alongside separate firearms exclusions.

How the Exclusion Plays Out

In practice, here's what the exclusion means for a security company:

- A guard physically removes a trespasser → GL carrier may deny on A&B grounds

- A guard restrains an aggressive patron → same result

- A fight breaks out and someone alleges the guard failed to intervene → the negligent supervision language in the exclusion may apply

- Defense costs, settlements, and judgments land entirely on the security company

Some GL policies offer a middle option: A&B coverage with a sublimit — a lower cap that applies only to A&B claims. That sounds better than a full exclusion, but sublimits frequently don't reflect actual claim costs, particularly in litigation-heavy venues.

The Umbrella Gap Problem

Many security companies assume their umbrella or excess policy fills any gaps in the underlying GL. It often doesn't.

IRMI's analysis of follow-form coverage notes that umbrella and excess policies aren't automatically seamless. Follow-form drafting can incorporate unfavorable underlying exclusions, and some excess programs follow the most restrictive underlying provisions. If the GL excludes A&B, the umbrella may provide no additional A&B protection at all.

Multi-party lawsuits make this worse. Security companies are frequently named alongside:

- Property owners and venue operators

- Apartment managers and commercial landlords

- Other contracted parties on site

A coverage gap doesn't just expose the security company. It triggers indemnification disputes and contract breach allegations with the very clients who hired them.

The Security Industry's Unique Assault and Battery Exposure

Security companies aren't assigned to low-risk environments. Clients hire them because they already have a problem — trespassing, theft, crowd control, tenant disputes, or events where patron behavior is unpredictable. Guards are deployed into situations where physical confrontation is more likely than in almost any other industry.

Common Claim Types

The range of A&B claims that regularly target security companies includes:

- Excessive force during a removal or restraint

- Wrongful detention of a guest, customer, or tenant

- Failure to prevent an assault on the client's premises

- Escalation allegations — claims the guard made a situation worse

- Bystander injuries during a physical confrontation

ASIS has reported that if violence causes injury or death while a security company is on watch, recent cases show the company is likely to be named as a defendant. A 2018 Mercy Hospital shooting case involving security contractor SDI Security, Inc. settled for $20 million in January 2024 — a number that illustrates what inadequate coverage can mean for a business.

High-Risk Venue Categories

ASIS specifically identifies healthcare facilities, event venues, and retailers as facility types where security contractors face heightened litigation exposure. Nearly 80% of U.S. retailers reported rising store violence and organized retail crime. Bars, nightclubs, apartment complexes, and parking facilities generate similar exposure — alcohol-fueled incidents, tenant-guard confrontations, and shoplifter detention claims follow the same pattern.

Employer Liability Follows the Business

Across all of these environments, the same legal principle applies: security companies are generally held responsible for their guards' actions, even when a guard acted outside assigned duties or violated company policy. The guard may face personal liability, but the financial weight of a lawsuit lands on the business entity.

Failure-to-prevent claims carry the same exposure as excessive force allegations. The argument in those cases isn't that a guard did something wrong — it's that the threat was foreseeable and no intervention occurred. Courts treat that distinction as a liability, not a defense.

What Assault and Battery Insurance Covers (and What It Excludes)

Core Protections

A well-structured A&B policy for a security company typically covers:

- Legal defense costs — attorney fees and court costs

- Settlements and judgments paid to claimants

- Third-party bodily injury from altercations, including bystanders

- Claims arising from intentional acts within professional duty

- Negligent hiring, training, or supervision allegations tied to an A&B incident

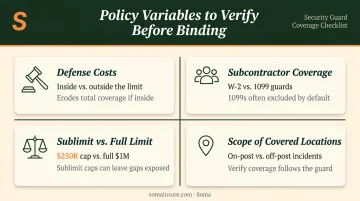

Critical Policy Variables to Verify

Not all A&B policies are built the same. Before binding coverage, security companies should confirm these four variables:

- Defense costs inside vs. outside the limit: Legal fees that count against your policy limit can quietly drain coverage before a judgment is even reached — a serious problem in states like California, Florida, and New York where A&B claims routinely go to trial

- Subcontractor coverage: Many policies cover only W-2 employees. If your agency uses 1099 or contract guards, verify they're explicitly included — or you may be uninsured on your highest-risk workers

- Sublimit vs. full limit: Some policies bury A&B under a lower sublimit (say, $250K) within a $1M GL policy. A single serious claim can exceed that sublimit fast

- Scope of covered locations: Confirm whether coverage follows the guard or the post. Incidents off assigned post orders are a common exclusion that surfaces only at claims time

Common Exclusions to Watch For

A&B policies frequently exclude:

- Firearm discharge: Armed security typically requires a separate endorsement or a policy written specifically for armed operations. Standard A&B does not automatically cover shooting incidents

- Sexual misconduct: Treated as a distinct coverage line in most programs — not bundled into A&B

- Off-post incidents: If a guard intervenes in a situation outside their assigned zone, the resulting claim may fall entirely outside policy coverage

The Umbrella Gap Most Agencies Miss

One exclusion compounds all the others: the umbrella policy. If your underlying GL excludes A&B, your umbrella may exclude it too — because most umbrellas "follow form," meaning they mirror whatever the primary policy covers or excludes.

Before assuming your umbrella provides a backstop for large A&B claims, confirm in writing whether the umbrella independently covers A&B or whether the GL exclusion flows straight through. Many security agencies discover this gap only after a verdict exceeds their primary limits.

Armed vs. Unarmed Guards: Does Coverage Change?

Armed Security

Carriers underwriting armed security operations want documentation before they quote. Standard requirements typically include:

- Firearm training records for each guard

- Individual guard licensing documentation

- Written use-of-force procedures

- Weapon storage protocols

Firearm-related incidents produce severe claims, so underwriting scrutiny is higher and coverage is priced accordingly.

Policies written for unarmed operations may explicitly exclude armed guard activities. Any security company that deploys even occasional armed personnel needs to confirm their policy covers those operations — not assume it does.

Unarmed Security

Unarmed companies should not assume their A&B exposure is minimal. Guest removals, trespasser confrontations, retail detentions, and parking lot disputes all produce use-of-force and wrongful detention claims without a weapon involved.

The key difference comes down to underwriting layers: armed operations carry firearm-specific documentation requirements on top of standard A&B coverage, while unarmed operations need the same core protection without those added steps.

How to Secure the Right Assault and Battery Coverage

Questions to Ask Before Buying or Renewing

Before signing any policy, security companies should confirm:

- Is A&B included, excluded, or sublimited on this policy?

- Does it apply to armed guards, unarmed guards, or both?

- Does coverage extend to the venue types you serve — bars, apartments, events, retail?

- Are defense costs inside or outside the policy limit?

- Are subcontracted guards covered or excluded?

- Can the policy satisfy additional insured, primary and noncontributory, and waiver of subrogation requirements in client contracts?

Reviewing Contracts Before Signing Them

This review needs to happen before a client contract is signed — not after. Contract requirements vary significantly. As one example, a 2022 Invest Atlanta security services RFP required GL with no exclusion for assault and battery, $2M per occurrence limits, additional insured status, waiver of subrogation, primary and noncontributory wording, and follow-form umbrella language. Security companies without conforming coverage would fail that requirement entirely.

Apartments, HOAs, bars, and event venues increasingly include specific A&B requirements with defined limits. Meeting those requirements requires knowing what your policy says before you commit.

Why Specialized Placement Matters

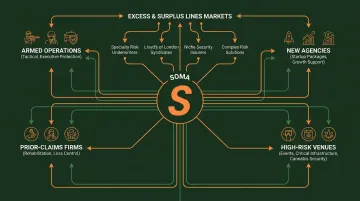

A&B coverage for security companies often falls outside what standard admitted markets will write. Carriers that will cover a general contractor or retail store may decline security operations outright — particularly armed guards, new agencies, or firms with prior claims.

That's where access to excess and surplus lines markets can open up carrier options that standard markets won't provide. Soma places coverage for security agencies across these scenarios:

- Armed guard operations that admitted carriers routinely decline

- New agencies without an established loss history

- Firms with prior A&B claims needing coverage that doesn't exclude the exposure

- Operations serving high-risk venues like bars, nightclubs, and large events

With hundreds of carrier partners and fast quote turnaround, the focus is on confirming A&B coverage is explicitly in the policy — not buried in an exclusion.

Frequently Asked Questions

What insurance do I need for my security company?

Security companies typically need general liability (with A&B coverage confirmed, not assumed), workers' compensation, commercial auto if vehicles are used, professional liability/E&O, and umbrella liability. A&B is not automatic under standard GL forms — the policy language must be reviewed to confirm it's included.

Can a security guard be charged with assault?

Yes. Guards can face criminal charges and civil liability claims when force exceeds what's legally justified. Use-of-force training reduces the likelihood of incidents; A&B coverage responds when claims arise even after proper conduct.

What are the requirements for a security company?

Requirements vary by state and generally include business licensing, guard licenses, background checks, training certifications, and proof of insurance. Both client contracts and some state regulators specifically require GL coverage with A&B confirmed as included.

Does general liability insurance cover assault and battery for security companies?

Many GL policies exclude or sublimit A&B coverage, so coverage cannot be assumed. The policy language and endorsements must be reviewed to confirm whether A&B is included — the certificate of insurance alone won't show whether an exclusion applies.

How much does assault and battery insurance cost for a security company?

Cost depends on armed vs. unarmed operations, total payroll, venue types served, prior claims history, guard training standards, and requested limits. Pricing varies too much across operations for a single average to be useful — get a quote based on your specific setup.

Is assault and battery coverage required by client contracts?

Yes, frequently. Contracts for apartments, HOAs, bars, nightclubs, events, and retail centers often require A&B coverage with defined limits, additional insured endorsements, and primary/noncontributory wording — companies without conforming coverage risk losing contracts or facing disputes after a claim.