This scenario plays out constantly for bar owners, roofing contractors, security agencies, and dozens of other business types. The problem isn't that coverage doesn't exist. It's that the path to finding it runs through a completely different market than most business owners know about.

This guide covers why businesses get flagged as hard to place, how the surplus lines market fills that gap, and the practical steps to securing coverage — even after multiple declines.

TL;DR

- "Hard to place" means standard carriers declined your risk, not that coverage is unavailable

- The Excess & Surplus (E&S) lines market exists specifically for these situations, and it now represents $130.9 billion in annual U.S. premiums

- High-risk industry classification, prior claims, and coverage lapses are the most common triggers for placement difficulty

- E&S policies cost more and carry broader exclusions than standard market coverage, so knowing the trade-offs matters before you bind

- Specialist brokers with direct E&S access, like Soma, can often place coverage in days with a complete submission

What Is Hard-to-Place General Liability Insurance?

Standard commercial general liability (CGL) insurance covers four core exposures:

- Bodily injury and property damage arising from your operations (Coverage A)

- Personal and advertising injury — defamation, wrongful eviction, copyright infringement (Coverage B)

- Legal defense costs when covered claims are filed against you

- Premises liability for injuries occurring on your property

Most small businesses can get this coverage through admitted (state-licensed) carriers at predictable rates. But admitted carriers file their rates and forms with state regulators, which limits their flexibility. When a risk falls outside their pre-approved appetite: too many prior claims, an unusual operation, or too much severity potential — they decline.

The surplus lines market exists for exactly these situations. As WSIA describes it, surplus lines function as the insurance industry's "safety valve" for risks that are hard to place, unique, or high-capacity. Non-admitted (surplus lines) carriers aren't bound by state rate and form regulations, giving them the flexibility to price and structure coverage for risks admitted carriers won't accept.

A declination from standard carriers simply means your business requires a different placement path — one that runs through surplus lines markets and a broker with access to them.

Why Your Business May Be Considered Hard to Place

Underwriters evaluate every submission against two dimensions: how often claims occur (frequency) and how expensive those claims are when they do (severity). Verisk's five-year GL analysis found an overall loss ratio of 67% and average severity of $78,224 — with bodily injury accounting for two-thirds of total losses. Anything that pushes those numbers higher triggers underwriting scrutiny.

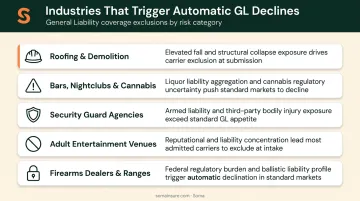

High-Risk Industry Classification

Certain industries trigger automatic declines from admitted carriers regardless of an individual business's track record. Common examples include:

- Roofing and demolition contractors

- Bars, nightclubs, and cannabis businesses

- Security guard agencies

- Adult entertainment venues

- Firearms dealers and shooting ranges

These industries share high public interaction, physical harm potential, or regulatory complexity — all of which create claim exposure that standard carriers aren't priced to absorb.

Poor or Frequent Claims History

A single large claim might be explainable. A pattern of smaller, frequent claims signals something structural about how a business operates. High frequency — even with low per-claim costs — often disqualifies a business from the standard market faster than one large isolated loss.

Unusual or Mixed Operations

A restaurant that hosts ticketed live events with a full bar presents overlapping exposures: food service liability, entertainment liability, and liquor liability. Standard underwriters work from pre-approved class codes. Operations that span multiple codes create ambiguity they'd rather avoid.

New Businesses and Lack of Track Record

Startups and businesses with no operating history give underwriters nothing to evaluate. Without loss runs, revenue history, or a demonstrated safety record, carriers have no basis for pricing the risk — so many simply decline.

Prior Cancellations or Coverage Lapses

Insureon notes that businesses with prior cancellations or coverage gaps face higher premiums and difficulty securing coverage when they return to market. A history of non-payment cancellations signals financial instability. A lapse in coverage, even an unintentional one, raises questions about how seriously a business takes risk management.

Industries That Commonly Face Hard-to-Place GL Challenges

General liability accounts for 36.9% of premium written through surplus lines stamping offices — which tells you something about how many GL risks the standard market simply won't write.

These industries land in the E&S market most frequently:

| Industry | Primary GL Concern |

|---|---|

| Bars & nightclubs | Assault and battery, liquor liability, late-night incidents |

| Security guard companies | Use of force, wrongful detention, armed guard exposure |

| Roofing contractors | Fall injuries, property damage, subcontractor liability |

| Demolition contractors | Structural collapse, debris hazards, third-party property damage |

| Cannabis businesses | Regulatory complexity, product liability, premises exposure |

| Adult entertainment venues | Assault claims, liquor service, reputational liability |

| Fireworks retailers | Product ignition, storage hazards, third-party injury |

| Amusement parks | Ride-related injuries (standard policies often exclude roller coasters and trampoline parks entirely) |

| Firearms dealers | Product liability, theft-related third-party claims |

Industry type isn't the only factor. Geography matters too. California, Texas, and Florida together represented 43.2% of all U.S. surplus lines premium in 2024, according to NAIC data. Operating in a high-volume E&S state often means your risk profile carries additional scrutiny regardless of your specific industry.

Even businesses in traditionally low-risk categories can become hard to place. Two common examples:

- A retail store that adds fitness classes introduces premises liability and instructor liability simultaneously

- A tech company handling regulated health data triggers coverage complexity that standard GL forms weren't designed to address

Soma places hard-to-insure GL coverage across several of these categories, including bars and nightclubs, security agencies, hospitality operations, and construction contractors. The brokerage works with carriers like Markel, Kinsale, and Liberty Mutual specifically for risks that standard market brokers turn away.

How the Excess & Surplus Lines Market Fills the Gap

The U.S. E&S market grew 12.2% in 2024 to $130.9 billion in direct premiums written — roughly 12% of the entire U.S. property and casualty market. The driver is simple: admitted carriers keep tightening their appetite, and more businesses end up needing an alternative path to coverage.

How E&S Carriers Operate

Non-admitted carriers are still licensed by state surplus lines regulators. They operate legally — just without the rate and form restrictions that bind admitted carriers. That flexibility lets them:

- Write higher-hazard risks at market-reflective pricing

- Add manuscript endorsements tailored to specific operations

- Structure retentions and limits based on individual risk profiles

Carriers like Kinsale Capital, Markel, and James River specialize in this space. They build underwriting expertise around the exact industries that admitted carriers avoid.

The Role of the Surplus Lines Broker

Standard retail brokers have appointments with admitted carriers only. To access the E&S market, a broker needs surplus lines licensing and established relationships with E&S carriers or wholesale intermediaries.

A business declined by its existing broker isn't necessarily uninsurable. In many cases, the broker simply lacks access to the right markets.

The Diligent Search Requirement

In most states, a broker must document that a risk was declined by admitted carriers before placing it in the surplus lines market. State requirements vary:

- Federal/WSIA standard: Three admitted carrier declinations

- California & New York: Three documented declinations required

- Florida: Diligent effort requirement repealed entirely

Important Trade-offs to Understand

E&S policies aren't identical to admitted policies with a higher price tag. Key differences include:

- No state guaranty fund protection — if the E&S carrier becomes insolvent, policyholders don't have the backstop that admitted policyholders do

- Broader exclusions — liquor liability, assault and battery, and professional liability are often carved out and require separate policies

- Higher retentions — self-insured retentions (SIRs) are common, where the insured bears all defense and indemnity costs below the retention threshold before the insurer's obligations begin

- Non-standard policy forms — manuscript endorsements may narrow or expand coverage in ways that require careful review before finalizing coverage

How to Secure Hard-to-Place General Liability Insurance

Getting placed in the E&S market isn't complicated, but incomplete submissions are the most common reason businesses face delays or inflated pricing. Here's the process.

Step 1 — Document Your Risk Thoroughly

E&S underwriters need more than a completed ACORD form. Prepare:

- Five years of loss runs (from all prior carriers, including years with zero claims)

- Full business description covering all operations, including any secondary revenue streams

- Safety protocols — written procedures, employee training records, incident response policies

- Financial statements if required for larger accounts

- Any prior declination letters from admitted carriers

Incomplete submissions either get declined outright or come back with inflated premiums that reflect the underwriter's uncertainty.

Step 2 — Work with a Broker Who Specializes in Complex Placements

Broker selection matters more here than in standard placements. A broker without E&S market access will either tell you the risk can't be placed or refer you elsewhere — costing time you may not have if your current coverage is about to lapse.

Soma works hard-to-place GL accounts by submitting simultaneously across multiple surplus lines markets, drawing on relationships with hundreds of carrier partners. For a business that's already received declinations from standard carriers, that breadth of market access is often what gets a policy bound.

Step 3 — Implement Risk Mitigation Before Applying

Underwriters price what they see, not what you intend to do. Documented improvements made before submission — installing security cameras, implementing a written safety program, completing relevant certifications — can directly affect how a risk is priced.

For bars and nightclubs, documented security staff training and ID-checking procedures directly impact liquor liability pricing. For contractors, written fall protection programs affect GL rates. These aren't cosmetic changes — they shift the underwriting conversation.

Step 4 — Submit a Professional Risk Narrative

A bare application tells an underwriter what happened (prior claims, revenue, operations). A well-crafted narrative explains the context: what changed, what controls are in place now, and why the historical loss experience doesn't represent current risk. Submissions that tell a coherent story about risk management tend to produce better pricing than bare applications from comparable businesses.

Step 5 — Review Policy Terms Before Binding

Before signing off, confirm:

- Per-occurrence vs. aggregate limits — what's the maximum per claim vs. the total annual cap

- Exclusions — is liquor liability excluded? Assault and battery? Professional services?

- SIR vs. deductible mechanics — an SIR means you bear defense costs before the carrier steps in; a deductible typically reimburses after

- Manuscript endorsements — any non-standard language that restricts or expands the base form

What to Expect: Costs, Limits, and Policy Terms

Premium Benchmarks

Standard GL for a typical small business runs a median of $45/month, with 85% of small businesses choosing $1M per occurrence / $2M aggregate limits.

Businesses in high-hazard categories pay significantly more:

| Business Type | Median Monthly GL Premium |

|---|---|

| Standard small business | $45/month (~$540/year) |

| Bar or tavern | $218/month (~$2,621/year) |

| Roofing contractor | $267/month (~$3,200/year) |

Insureon notes that E&S policies from non-admitted carriers almost always cost more than comparable standard-market policies. For the highest-hazard classes — demolition, nightclubs, security agencies — premiums can run well above these benchmarks.

Policy Structure Differences

Hard-to-place GL policies frequently include:

- Higher deductibles or SIRs, sometimes requiring collateral

- Carved-out exclusions that require separate policies (liquor liability, assault and battery, professional liability)

- Coverage triggers that are narrower than standard CGL forms

- Annual re-underwriting at renewal — each renewal is essentially a new submission

Managing Renewals

E&S underwriters treat each renewal as a fresh evaluation, so how you manage your account year-round directly affects pricing. Three things make the biggest difference:

- Keep loss records clean and document any claims proactively

- Record operational improvements (safety programs, new equipment, reduced headcount in hazardous roles)

- Notify your broker of any changes to operations or revenue before renewal — not after

Frequently Asked Questions

What is the alternative to general liability insurance?

There's no direct substitute. Businesses unable to obtain GL coverage may consider self-insurance (setting aside capital reserves), captive insurance programs, or risk retention groups — but these options require significant capital and are generally only viable for larger, well-funded organizations.

What makes a business hard to place for general liability insurance?

The main triggers are high-risk industry classification, a pattern of prior GL claims, unusual or mixed business operations, lack of operating history for new businesses, and prior policy cancellations or coverage gaps.

Can a business be denied general liability insurance entirely?

Standard carriers may decline, but very few risks are genuinely uninsurable. The E&S/surplus lines market exists specifically to cover risks that admitted carriers won't write. The coverage may cost more and carry different terms, but it's typically available.

What is the difference between admitted and non-admitted carriers?

Admitted carriers are state-licensed with rate and form oversight, and their policyholders are protected by state guaranty funds. Non-admitted (surplus lines) carriers have more pricing and form flexibility but aren't backed by state guaranty funds — policyholders bear that insolvency risk.

How much more expensive is hard-to-place general liability insurance?

It varies significantly by industry and risk profile. E&S placements almost always cost more than standard admitted policies — according to Insureon, bars and roofing contractors already pay four to seven times the median small-business GL premium.

How long does it take to get hard-to-place general liability coverage?

With a specialized broker who has direct E&S market access and a complete submission, coverage can often be placed within days. The most common delay is an incomplete initial submission that triggers multiple follow-up rounds with underwriters.