Many cyber insurance policies include a media liability provision to address exactly these exposures. But the scope of that coverage varies dramatically across carriers, and most buyers don't know what they actually have until a claim surfaces.

This article breaks down what media liability coverage looks like inside a cyber policy, what it typically covers and excludes, how policies differ, and how to determine whether your current coverage is adequate.

TL;DR

- Cyber media liability covers content-related claims — defamation, copyright infringement, and privacy violations — from digital publishing.

- Common policy labels include "Multimedia Liability," "Media Content Liability," and "Online Media Liability."

- Coverage depth varies widely: some policies offer minimal protection; others approach standalone policy breadth.

- Key limitations include digital-only scope, claims-made triggers, and exclusions for intentional conduct and patent infringement.

- Content-heavy businesses should confirm whether cyber policy media liability provisions are adequate or if standalone coverage is needed.

What Is Media Liability Coverage in a Cyber Insurance Policy?

Any organization that publishes content online carries media liability risk — the legal exposure that arises from creating, distributing, or hosting content that harms someone. This isn't limited to news outlets or publishers. A retail brand's product comparison page, a healthcare company's patient blog, a SaaS company's LinkedIn campaign — all of these are publishing activities that can trigger a claim.

Where It Lives Inside a Cyber Policy

Media liability coverage typically appears as a named insuring agreement or endorsement within a broader cyber policy, not as a standalone product. Carriers label it differently:

- Multimedia Liability (Hiscox)

- Media Liability (Beazley)

- Online Media Liability (Chubb UK)

The label matters less than the actual insuring agreement language — two policies using the same label can offer meaningfully different protection.

Why Cyber and Media Risk Intersect

Consider two scenarios. A hacker compromises a company's social media account and posts defamatory content about a competitor. An employee accidentally publishes private client data on the company's website. Both scenarios qualify as cyber claims and media claims simultaneously — which is exactly why media liability coverage belongs inside a cyber policy.

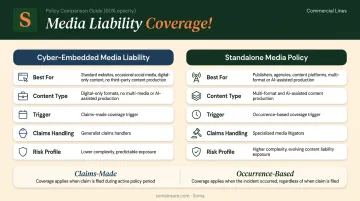

Cyber-embedded media liability is narrower than a standalone media policy, focusing on digital content risks. For most businesses, that scope is sufficient; for companies with significant publishing activity, the difference is worth evaluating.

What Does Cyber Media Liability Coverage Typically Include?

Most cyber media liability insuring agreements cover the following categories of wrongful acts — all triggered by publishing or disseminating content through digital channels.

Defamation

Coverage for claims that published content — blog posts, social media, marketing materials — made false or harmful statements about a person or business. This includes:

- Libel (written statements)

- Slander (spoken or recorded statements)

- Product disparagement — for example, a blog post comparing competitors in a misleading way

Copyright and Trademark Infringement

Protects against unintentional use of another party's protected work in online content: images, copy, video, music, or branding. Federal copyright filings jumped 23% in the 12 months ending March 31, 2024, and nearly 40% of small copyright claims involve photographs. That makes website and marketing asset clearance a genuine exposure for most businesses.

Note: Patent infringement is explicitly excluded from virtually all cyber media liability provisions.

Privacy and Publicity Rights

Covers invasion of privacy, misappropriation of likeness, and violation of the right of publicity. Examples:

- A healthcare company sharing a patient story with identifying details

- A marketing team using someone's image in a digital ad without consent

Channel Scope

Most cyber media liability provisions apply to content distributed through:

- Websites and blogs

- Social media platforms

- Email communications

- Online advertising

- Other electronic formats

Coverage applies to unintentional wrongful acts. Deliberate or knowing violations are typically excluded.

Key Limitations and Exclusions in Cyber Media Liability Coverage

Digital-Only Restriction

The most consequential limitation: most cyber policies restrict media liability to internet or electronic content, excluding print, physical broadcast, or offline formats unless specifically endorsed. A company distributing both a digital newsletter and a printed catalog may find its print materials completely unprotected under the cyber policy's media liability provision.

The Claims-Made Problem for Media Risk

Cyber policies are typically written on a claims-made and reported basis — coverage only responds if the claim is filed and reported during the active policy period.

Media claims are often long-tail. Content published today may not generate a lawsuit for 18 months. If the policy lapses, isn't renewed, or is replaced without an extended reporting period, that gap can be costly. That's why retroactive dates and prior publication exclusions both deserve close review before binding or renewing coverage.

Intentional Conduct Exclusions

Most cyber policies exclude claims arising from intentional acts. This creates a specific problem for media-related lawsuits:

- Defamation is classified as an intentional tort in many jurisdictions

- Willful copyright infringement allegations are common in content disputes

- Punitive damages — often pursued in these cases — may be uninsurable in certain states

Standalone media liability policies are specifically designed to handle these scenarios. A cyber policy's intentional-act exclusion can quietly eliminate coverage for your most likely media claim — without any warning until you're already in litigation.

Software and Source Code Copyright Carve-Out

Beazley's cyber policy, for example, explicitly excludes patent and software copyright from covered loss — and it's not alone. Many carriers carve out copyright claims tied to software, source code, or software licenses from the media liability insuring agreement entirely.

For technology companies, SaaS businesses, and any firm that produces both software and content, this is a gap that typically surfaces only after a claim is denied.

Coverage Variations: How Cyber Policies Differ on Media Liability

Not all cyber policies treat media liability the same way. The range runs from a few lines addressing only internet defamation to near-comprehensive coverage approaching what a standalone media policy provides.

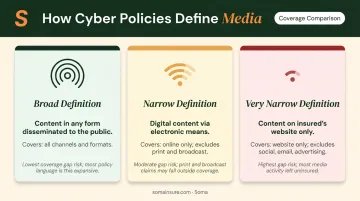

The Definition of "Media" Is Everything

How the policy defines "Media" determines how much of your actual publishing activity is protected:

| Definition Type | Example Language | What It Covers |

|---|---|---|

| Broad | "Content in any form disseminated to the public" | Wider channel and format scope |

| Narrow | "Digital content disseminated via electronic means" | Online only; print and broadcast excluded |

| Very narrow | "Content published on the insured's website" | Excludes social, email, and advertising |

A narrow definition can exclude a substantial portion of a business's actual publishing activity.

Endorsements That Can Expand Coverage

Some carriers offer endorsements or carve-backs that broaden the baseline media liability provision. Options worth asking about:

- Coverage for print content or non-digital advertising

- Subpoena response costs

- Declaratory relief expense coverage

- First Amendment restraint coverage (more common in standalone policies)

When evaluating cyber policies, these additions are worth requesting and comparing — they won't appear in the standard form.

Policy language varies significantly across carriers. Comparing the actual insuring agreement wording — not just the product name — is what surfaces meaningful differences. Soma places cyber coverage with carriers including Chubb, Hiscox, Kinsale, and Liberty Mutual, and can run that comparison across options for your specific business.

Cyber Media Liability vs. Standalone: Which Do You Need?

When Cyber Coverage Is Sufficient

Cyber-embedded media liability is likely adequate for businesses that:

- Maintain a standard website and post occasionally on social media

- Run digital ad campaigns without sensitive or comparative claims

- Don't produce content for third-party clients

- Have no significant volume of health, financial, or legal content

When Standalone Coverage Makes More Sense

A standalone media liability policy is the stronger choice for:

- Publishers, media companies, and content platforms

- Marketing agencies and PR firms producing content for clients

- Any business where content creation is a primary commercial activity

- Companies with high-volume, AI-assisted, or influencer-driven content operations

According to Skyward Specialty, standalone media liability can be written on an occurrence basis — meaning coverage responds to any incident that occurred during the policy period, even if the claim comes years later. That structure is fundamentally better suited to long-tail publication risks. Beyond policy structure, standalone carriers maintain relationships with specialized media litigators — something cyber claims handlers, who are generalists, typically don't offer. Media claims often require counsel with First Amendment and IP litigation experience.

Four Questions to Guide the Decision

- How much content do you publish? Occasional posts and daily production carry very different risk profiles.

- Is it digital-only, or does it span print and broadcast? Cyber-only coverage leaves a gap if you're in multi-format territory.

- Does your content touch sensitive topics — health, finance, legal, or regulatory subject matter?

- Do you produce content for third-party clients? Agency-style exposure typically warrants standalone coverage.

How to Evaluate Your Cyber Policy's Media Liability Coverage

Five Questions to Ask When Reviewing a Policy

- Does the policy cover both electronic and print media, or only digital content?

- How does the policy define "wrongful act" under the media liability insuring agreement? Confirm it includes defamation, copyright, trademark, privacy, and publicity rights.

- Are intentional acts excluded? If so, understand what that means for defamation and willful infringement claims.

- Is there a software copyright carve-out? Critical for technology companies and SaaS businesses.

- Is coverage claims-made or occurrence-based? And what is the retroactive date?

When to Trigger a Review

Policy review shouldn't happen only at renewal. Media liability provisions should be re-evaluated whenever a business:

- Launches a new content channel or platform

- Hires a content agency or begins influencer marketing

- Starts using AI-assisted content production tools

- Expands into new advertising formats or regulated industries

CMI research found that 81% of B2B marketing teams now use generative AI tools — a shift that introduces new unintentional copyright exposure that standard cyber media provisions may not clearly address.

The Broker's Role

That AI-driven copyright exposure is exactly where policy language differences start to matter. Because media liability wording varies so widely across carriers, the clearest way to assess this is working with a broker who compares actual policy forms, not just product summaries.

Soma's access to hundreds of carrier partners makes it possible to run a side-by-side comparison of cyber policies with varying media liability provisions — including placements through Chubb, Hiscox, Kinsale, and Liberty Mutual — and identify which form matches a business's actual content footprint.

Frequently Asked Questions

What types of claims does media liability in cyber insurance typically cover?

Cyber media liability provisions typically cover defamation (libel and slander), copyright and trademark infringement (excluding patents), invasion of privacy, and misappropriation of likeness — all arising from content published through digital channels such as websites, social media, and online advertising.

Is media liability the same as errors and omissions (E&O) insurance?

No. E&O protects against mistakes or failures in delivering professional services, while media liability protects against harm caused by published content. Some cyber policies bundle both, but the scope of each should be evaluated separately.

Does every cyber insurance policy include media liability coverage?

No. Media liability is not a standard feature of all cyber policies. Some include it as a named insuring agreement; others omit it entirely or offer it only as an optional endorsement. Buyers should review the actual policy language, not just the marketing description.

Does cyber media liability coverage apply to AI-generated content?

Most cyber media liability provisions respond to claims from AI-generated content the same way they would any digital content, but intentional infringement is excluded. AI-generated content carries elevated risk of unintentional copyright issues — confirm your policy covers unintentional infringement before publishing AI-assisted material at scale.

What is the difference between "claims-made" and "occurrence-based" coverage for media liability?

Claims-made coverage (common in cyber policies) only responds if a claim is filed during the active policy period. Occurrence-based coverage (common in standalone media policies) covers any incident that occurred during the policy period, even if the claim surfaces years later. For content that circulates for years — a published article, a campaign asset, an archived post — occurrence-based coverage offers meaningful protection that claims-made policies do not.

When should a business consider a standalone media liability policy instead of relying on cyber coverage?

Businesses whose core activities involve content creation, publishing, or producing media for clients — such as agencies, publishers, or platforms — typically need standalone coverage. The broader scope, occurrence-based trigger, and access to specialized media litigation defense make standalone policies the more appropriate fit for high-volume content operations.