These aren't edge cases. They're early signals of a claims environment that's widening fast.

Most businesses assume their existing coverage handles these scenarios. Many are wrong. The gaps are real, and discovering them after a claim is filed creates a very different conversation than discovering them at renewal.

TLDR

- Tech E&O is the primary policy line covering AI output errors, product failures, and service negligence claims

- Cyber insurance addresses AI-related data breaches and network security events but often leaves economic loss gaps

- "Silent AI" describes coverage that's neither explicitly included nor excluded — leaving dangerous gaps in CGL, EPLI, and professional indemnity policies

- Conduct a policy audit before your next renewal — don't wait for a claim to find the gaps

What AI Exposures Are Actually Putting Businesses at Risk

Most commercial AI liability doesn't start with a data breach. It starts with a wrong answer, a biased algorithm, or a generated image — and standard policies often treat these four exposure categories inconsistently.

Professional and Output Errors

When an AI tool produces a wrong answer that a client relies on, professional liability follows. Air Canada learned this firsthand. Attorneys in Mata v. Avianca discovered it when sanctioned for submitting AI-generated fake case citations. Any business using AI to deliver professional advice, research, or recommendations faces this exposure — and it doesn't require a security event to trigger a claim.

Copyright and IP Infringement

Generative AI produces outputs trained on third-party content. When a business uses that output commercially, copyright exposure travels downstream from the AI developer to the business deploying the tool. Alcon Entertainment sued Tesla and Warner Bros. over AI-generated promotional images that resembled Blade Runner 2049 after Alcon refused permission to use the film's imagery.

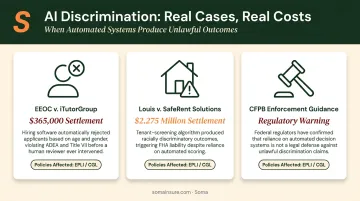

Algorithmic Discrimination

Bias embedded in AI systems creates real legal exposure under employment and consumer protection law:

- EEOC vs. iTutorGroup — settled for $365,000 after hiring software automatically rejected female applicants over 55 and male applicants over 60

- Louis v. SafeRent Solutions — a $2.275 million settlement after a tenant-screening algorithm allegedly harmed Black and Latinx applicants

- The CFPB has confirmed explicitly that automated systems are not an excuse for unlawful discrimination in financial services, housing, or employment

Finance, healthcare, and HR tech businesses draw the most attention from the EEOC and CFPB — the two regulators most active in this space.

Bodily Injury and Property Damage

Tech E&O policies typically exclude bodily injury and property damage — which creates a direct coverage gap for AI deployed in manufacturing automation, autonomous vehicles, or medical devices. The Cruise autonomous vehicle case resulted in a $500,000 DOJ fine after a vehicle struck and dragged a pedestrian. Without a standalone product liability or commercial auto policy, that gap falls on the business.

How Tech E&O Insurance Covers AI-Related Claims

What Tech E&O Actually Does

Technology Errors and Omissions insurance covers third-party claims arising from a wrongful act, error, or omission in the performance of technology services — or the failure of a tech product to perform as intended. Unlike cyber insurance, Tech E&O typically covers breach of contract claims, which matters significantly for businesses that make performance commitments around AI outputs.

A Tech E&O claim triggers when:

- An AI model underperforms against contractual specifications

- An automated system generates incorrect outputs causing client financial loss

- A software product fails to deliver promised functionality

Coverage generally includes defense costs, settlements, and judgments for negligence or product failure claims — including scenarios where a client sues over faulty AI outputs or service delivery failures.

The Exclusions That Create Gaps

Most Tech E&O policies carry two exclusions that matter for AI-deploying businesses:

- Bodily injury and property damage — excluded in most forms, meaning AI deployed in physical environments may not be covered

- Contractual liability — some policies exclude this, meaning businesses that indemnify clients for AI failures via contract may be exposed even when the underlying loss would otherwise trigger coverage

What Underwriters Are Now Asking

The application process has shifted noticeably. Philadelphia Insurance's integrated Tech E&O and Cyber application now specifically asks applicants to identify revenue from AI software and services, and asks about generative AI use in producing original content.

Expect underwriting discussions to cover topics like:

- Governance frameworks and human oversight of AI systems

- Reliance on AI outputs and disclosure practices

- Technical due diligence and expected model error rates

- Ongoing monitoring procedures post-deployment

Aon and Munich Re both flag these as coverage-relevant factors in AI risk assessment. Businesses without documented governance practices will face harder questions — and likely higher premiums or narrower terms.

Where Cyber Insurance Fits Into the AI Risk Picture

Cyber insurance currently handles more AI-related claims than any other policy line, largely because AI risk and data risk overlap substantially. Most cyber policies already cover:

- Data breaches triggered by AI vulnerabilities

- AI-enabled social engineering and deepfake fraud

- Regulatory investigations tied to data privacy violations

Coalition's affirmative AI endorsement, added in March 2024, explicitly clarifies coverage under its cyber policies for AI-related scenarios. Beazley documented a $6 million deepfake scam in which a CFO received a video call that appeared to be from the CEO — the kind of loss that pushed carriers to create AI-specific endorsements in the first place.

Real-world losses like these reveal a structural problem: cyber policies are built around security events, not service failures or professional misjudgments. That creates meaningful gaps.

Where Cyber Falls Short

Specific scenarios that commonly fall outside standard cyber coverage:

- AI output errors — an incorrect AI recommendation that causes client financial loss may not trigger cyber coverage if no breach or network incident occurred

- Contract disputes — cyber policies typically exclude breach of contract claims, even when an AI service failure is the root cause

- Professional liability — cyber doesn't cover this; negligent professional judgment, even AI-assisted, falls outside cyber's scope

The emerging market response is endorsements: carriers are adding deepfake response, AI regulatory defense, and affirmative AI coverage as policy add-ons. These aren't standard yet. Businesses relying on existing cyber coverage should verify explicitly whether AI scenarios are included — or work with a broker to identify the gaps before a claim surfaces.

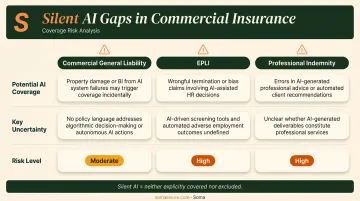

The "Silent AI" Problem: Coverage Gaps Businesses Need to Understand

Swiss Re has described silent AI by direct analogy to silent cyber: AI risks that are neither explicitly mentioned, limited, nor excluded in policy language — creating unintended insurance impacts across multiple lines. The silent cyber problem cost the industry significantly before Lloyd's Market Bulletin Y5258 in 2019 forced explicit cyber treatment across all Lloyd's policies. Silent AI is following the same trajectory.

Where the Gaps Appear

| Policy | Potential AI Coverage | The Uncertainty |

|---|---|---|

| Commercial General Liability | May cover advertising injury from AI-generated content | Excludes professional liability; AI output errors sit in a gray zone |

| EPLI | Could respond to AI discrimination claims | Most policies have no explicit AI language |

| Professional Indemnity | May cover AI-assisted professional decisions | Ambiguity when the AI made the decision, not the professional |

The Contractual Liability Trap

Many businesses sign vendor contracts with AI indemnity clauses, accepting responsibility for client losses caused by AI failures. If their Tech E&O or cyber policy excludes contractual liability, that obligation goes uncovered — even when the underlying loss itself would have triggered a payout. The gap isn't in the loss; it's in who agreed to pay for it.

The Direction This Is Heading

ISO has already introduced generative-AI exclusions in Commercial General Liability policies, and Verisk has developed new GL endorsements to exclude generative-AI exposures. Businesses waiting to address silent AI during their next renewal may find coverage narrowing rather than expanding. Waiting until renewal means negotiating from a weaker position — after carriers have already drafted the exclusions.

How to Prepare Your Business for AI Insurance Reviews

Three Steps Before Your Next Renewal

Build an AI use inventory — document every AI tool deployed, whether built internally or through a third-party vendor. Include the vendor name, the use case, the data involved, and who reviews outputs before they reach clients.

Review existing policies for AI exclusions or silence — look specifically at your Tech E&O, cyber, CGL, EPLI, and any professional indemnity policies. Flag any policy that neither explicitly covers nor explicitly excludes AI-related claims.

Identify contractual indemnity obligations — pull any vendor or client contracts that include AI indemnity or warranty clauses and share them with your broker before renewal.

What Underwriters Will Ask

Be prepared to answer questions across these areas:

- What percentage of revenue comes from AI-related products or services?

- How are AI models tested and validated before deployment?

- What data sources are used to train or fine-tune models?

- What human oversight exists for AI-generated outputs?

- What industries do your AI systems serve?

- Have you had any prior AI-related incidents or claims?

Getting the Coverage Stack Right

Businesses deploying AI in healthcare, financial services, or manufacturing often need coverage layered across Tech E&O, cyber, EPLI, and general liability. No single policy closes all the gaps. Getting those lines to work together — with consistent definitions and no overlapping exclusions — requires a broker who actively manages the coverage stack, not just individual policies.

Soma places complex technology and professional liability coverage across carriers including Chubb, Hiscox, Kinsale, and Markel. For businesses navigating AI-related exposure across multiple policy lines, Soma's risk management team can assess current gaps and turn around quotes quickly — without the delays that typically come with hard-to-place risks.

Frequently Asked Questions

Frequently Asked Questions

What does technology E&O insurance cover?

Tech E&O covers third-party claims for errors, omissions, or failures in technology products or services, including AI output failures, negligent service delivery, and breach of professional duty. Key exclusions include bodily injury, property damage, and (in some policies) contractual liability.

Is there a "30% rule" for AI decision-making oversight?

There is no universal percentage threshold. Insurers and regulators expect documented human oversight processes, but no fixed standard applies. NIST's AI Risk Management Framework and the EU AI Act both address oversight requirements without specifying a percentage.

Does my existing cyber insurance cover AI-related claims?

Cyber policies cover AI risks when they overlap with data privacy or network security events: data breaches, deepfake fraud, and AI-enabled social engineering typically qualify. Gaps appear for AI output errors that cause economic harm without a security event, and for breach of contract or professional liability claims.

What types of AI risks does Tech E&O insurance NOT cover?

The primary exclusions are bodily injury, property damage, and (in some policies) contractual liability. Businesses in healthcare, manufacturing, or autonomous systems — and those signing AI indemnity contracts — will likely need additional coverage layers beyond Tech E&O alone.

Do I need a standalone AI insurance policy?

Most businesses don't need one yet. Properly endorsed Tech E&O and cyber policies cover the majority of AI exposures. The priority is auditing current coverage for silent AI gaps and ensuring endorsements are in place for the specific AI scenarios your business faces.