For more than a decade, soft market conditions kept premiums relatively stable and coverage widely available. That's shifting. According to the AMA's 2026 Policy Research Perspective, medical liability premiums rose for the seventh consecutive year in 2025 — and carriers are posting underwriting losses that are prompting them to reprice risk more aggressively.

For healthcare organizations, the window to act before conditions fully tighten is narrowing. This report breaks down the four major trends reshaping HCPL in 2026, what's driving them, and what providers should do now.

TL;DR

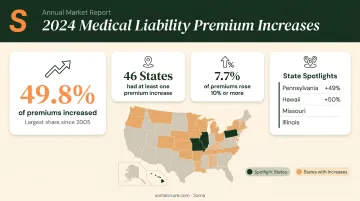

- Medical liability premiums rose for seven straight years; 49.8% of all reported premiums increased in 2024 alone

- Nuclear verdicts ($10M+) are up roughly 67% from 2013 to 2023, with the top 50 verdicts averaging $56M in 2024

- AI and telehealth are creating liability gaps that many current HCPL policies leave unresolved

- The TPLF market hit $15.2B in 2024, incentivizing larger claims and longer litigation timelines

- 82% of physicians are now employed by hospitals or corporate entities, increasing per-claim exposure at the system level

- Organizations that review coverage before a full hard market hits will find more carrier options and stronger policy terms available to them

Trend 1: Premiums Are Rising and a Hard Market Is Forming

What "Hardening" Means for HCPL Buyers

A hard market means premiums rise, underwriting standards tighten, carriers reduce capacity or exit the space, and more exclusions appear in policy language. For over 12 years, HCPL buyers enjoyed the opposite — soft conditions where competition among carriers kept prices low and terms favorable.

That dynamic is reversing. The AMA's 2026 premium analysis confirms:

- 49.8% of reported medical liability premiums increased in 2024 — the highest share since 2005

- 46 states had at least one premium increase in 2024

- 7.7% of all reported premiums increased by 10% or more, across 16 states

- In 2024 alone, Pennsylvania saw 49% of its reported premiums increase by 10%+; Hawaii saw 50%; Missouri and Illinois also posted double-digit spikes

For context on how far this could go: in the early-2000s hard market peak, 82.1% of all reported premiums increased in 2004. The current environment — while serious — hasn't reached those levels yet. That gap means buyers still have a window to lock in coverage before conditions tighten further.

Why Hard Markets Follow Soft Ones

The mechanics are predictable. During soft markets, carriers compete aggressively on price, often underpricing risk. HCPL is a "long-tail" line — claims from an occurrence today may not close for 3–5 years, masking true loss development until the damage is already done.

The numbers reflect that dynamic. AM Best reported the U.S. medical professional liability composite posted its 10th consecutive underwriting loss in 2024 — a $586M underwriting loss, up from $395M the prior year. When actuaries and rating agencies respond to accumulating losses, carriers pull back capacity or reprice aggressively.

Geographic Concentration

Not all states feel this equally. Jurisdictions without noneconomic damage caps — or where caps have been raised — face sharper increases. A 2025 Health Economics study found that repeal of noneconomic damage caps was associated with premium increases of 23.12% for OB-GYN in Illinois and 21.17% in Georgia.

The premium gap between states tells the same story. Miami-Dade OB-GYN premiums reached $243,988 in 2025, while Los Angeles/Orange County came in at $49,804 for the same specialty — a near-5x difference explained largely by California's tort caps.

| Market | OB-GYN Premium (2025) | Damage Cap Status |

|---|---|---|

| Miami-Dade, FL | $243,988 | No noneconomic cap |

| Los Angeles/Orange County, CA | $49,804 | Capped |

The practical consequence: fewer carrier options, more restrictive terms, and particular difficulty for organizations in high-litigation states or high-risk specialties.

Trend 2: Claim Severity Is Escalating — Nuclear Verdicts Are the New Normal

Trend 2: Claim Severity Is Escalating, and Nuclear Verdicts Are Reshaping Exposure

Social Inflation Is Driving Verdict Size

"Social inflation" describes the gap between general economic inflation and the rising cost of litigation — driven by plaintiff-friendly strategies, growing jury skepticism of large healthcare systems, and shifting expectations around what compensation should look like. In HCPL, this shows up most visibly in nuclear verdicts.

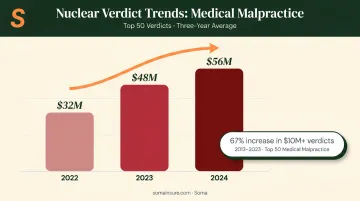

The AMA defines nuclear verdicts as awards of $10M or more (with "thermonuclear" verdicts exceeding $100M). According to The Doctors Company, medical malpractice verdicts at that threshold increased roughly 67% from 2013 to 2023 — and in 2023, more than half of those verdicts reached $25M or higher.

The trajectory continues upward:

| Year | Average of Top 50 Verdicts |

|---|---|

| 2022 | $32M |

| 2023 | $48M |

| 2024 | $56M |

The Long-Tail Problem for Reserves

Milliman's actuarial data shows claims in the $5M–$10M range take an average of 4.3 years from report to close, and $10M+ claims average 3.4 years. This lag means today's rising severity isn't fully visible in current loss ratios. Carriers are repricing now based on directional trends, not fully realized losses.

Milliman also selected annual severity trends of 5.0% on an unlimited basis in 2025, up from 4.5% two years prior. Unlimited severity is growing faster than severity capped at $5M — large outlier claims are pulling averages up, and that trend isn't slowing.

Specialty and Structural Exposure

Certain specialties and organizational structures consistently produce the highest-severity outcomes:

- Obstetrics, surgery, and anesthesiology generate the largest claims by volume and verdict size

- Hospitals and employed physician groups carry higher coverage limits, expanding the potential recovery available in a judgment

- Group and health system structures face compounded exposure because a single incident can implicate multiple insured parties

- Coverage limit selection becomes a direct factor in verdict targeting — higher limits increase plaintiff incentive to pursue large awards

Underwriters evaluate both specialty risk and entity structure when pricing HCPL coverage, and the combination of the two can move premiums significantly.

Trend 3: AI, Telehealth, and Digital Health Are Rewriting Liability Boundaries

Where the Coverage Gaps Are

The rapid expansion of telehealth and AI-assisted clinical tools has outpaced the underwriting frameworks designed to evaluate them. ONC data shows 71% of hospitals used predictive AI integrated with the EHR in 2024, up from 66% in 2023. Yet most HCPL policies were written before these tools became standard practice.

Key liability questions that remain unresolved in many policies:

- When an AI tool produces an incorrect recommendation and a patient is harmed, who is liable — the provider, the software vendor, or the EHR platform?

- Does using an FDA-cleared AI tool satisfy the standard of care, or does it establish a new, higher one?

- If a patient refuses conversion to an in-person exam and is harmed, is the telehealth provider exposed?

- Physicians must generally be licensed in the state where the patient is located during a virtual visit, creating a compliance gap that opens direct liability exposure

What This Means for Coverage

The Doctors Company notes that the standard of care for telehealth patients is the same as for in-person care. Remote clinical tools and limited physical examination make that standard difficult to consistently meet. Gallagher's telehealth liability analysis flags cross-border licensure, prescribing protocols, patient consent, and standard-of-care ambiguity as the primary risk areas.

AI-specific exposure adds another layer. When something goes wrong, the provider's HCPL policy typically gets called on first — even when the Milbank Quarterly notes that product-liability claims may ultimately implicate the AI manufacturer or vendor. Both claims can be filed simultaneously, leaving providers holding initial defense costs regardless of final liability.

Healthcare organizations using AI-assisted diagnostic tools or operating telehealth programs should ask their broker three specific questions:

- Does the current HCPL policy explicitly cover AI-assisted care decisions?

- Are telehealth services covered, and under what conditions?

- Is a separate technology errors and omissions (E&O) or cyber liability policy needed alongside HCPL?

Trend 4: Third-Party Litigation Funding and Healthcare Consolidation Are Compounding Exposure

Third-Party Litigation Funding (TPLF) Is Changing the Claims Landscape

Third-party litigation funding — where outside investors finance plaintiff lawsuits in exchange for a share of the settlement or verdict — has grown substantially in medical malpractice. The TPLF market reached an estimated $15.2B as of 2024, with U.S. TPLF growing 44% between 2019 and 2022 according to Milliman.

The structural effect on claims is straightforward: when a third party profits from a larger verdict, plaintiffs have less incentive to settle early and more reason to push cases to trial. Swiss Re has documented TPLF as a contributor to social inflation, noting it encourages plaintiffs to initiate and prolong lawsuits.

In an already high-severity HCPL environment, that dynamic directly compounds claim costs.

Healthcare Consolidation Is Increasing Per-Claim Exposure

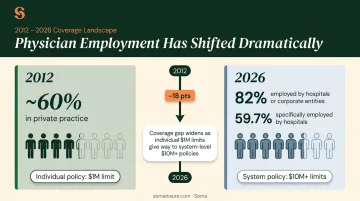

Physician employment has shifted dramatically. Key data points illustrate the scale of the shift:

- 82% of physicians were employed by hospitals or corporate entities as of January 2026, including 59.7% by hospitals (PAI/Avalere, 2026)

- Only 42.2% of physicians remained in private practice in 2024 — down 18 percentage points from 2012 (AMA)

What this means for coverage: a physician who once carried a $1M individual policy is now an employee of a system carrying $10M+ limits. The coverage obligation is larger. The potential verdict target is larger. Organizations that have grown through acquisition or employ large physician groups should audit their current HCPL limits against their actual exposure profile — the gap between the two is often wider than it appears.

What Healthcare Organizations Should Do to Prepare

The Convergence of Pressures

Several forces are hitting simultaneously in 2026:

- Claim frequency rising in high-risk specialties and plaintiff-friendly jurisdictions

- Social inflation driving jury expectations well above historical baselines

- Technology disruption outpacing underwriting models for AI and telehealth

- Workforce strain — a JAMA Internal Medicine meta-analysis found physician burnout associated with roughly 2-fold increased odds of patient safety incidents, which correlates with claim exposure

- Legislative shifts — Colorado's HB24-1472 raised noneconomic damage caps to $875,000 with future inflation adjustments, a signal that other states may follow

Operational and Financial Impact

Tighter HCPL conditions are already visible in the renewal process:

- Longer underwriting timelines with more detailed questionnaires

- Requests for loss runs going back 5+ years

- Specific questions about AI and telehealth usage

- Some organizations moving to surplus lines markets as admitted carriers tighten appetite

Smaller practices and rural providers have less negotiating leverage than large systems, making the cost pressure disproportionate. Maryland's insurance administration reported total statewide medical malpractice premiums of $339.5M in 2024 — a 3.34% single-year increase across the entire market.

Scenarios for 2026 and Beyond

Those Maryland figures reflect a market still in transition. If conditions continue hardening, healthcare organizations can expect:

- 10–20%+ renewal increases, particularly in high-litigation states

- Coverage concentration in fewer carriers, limiting competitive options

- Growing reliance on captives — the Cayman Islands had 136 registered captive companies for medical malpractice as of Q3 2024, accounting for $3.2B in premiums, and large health systems increasingly retain claims up to $50M–$100M through these structures

The organizations best positioned are those reviewing their programs now, before conditions fully harden. That means conducting a genuine risk assessment, identifying technology and consolidation-driven exposure changes, and working across multiple markets to secure competitive terms.

Soma places medical malpractice and professional liability coverage for outpatient clinics, inpatient facilities, ambulatory providers, and allied health professionals through carrier partners including CRC Group, Chubb, and Kinsale. For healthcare organizations navigating this market, working with a brokerage that understands healthcare exposure profiles and has access to multiple carriers often determines both coverage quality and final renewal terms.

Frequently Asked Questions

What is healthcare professional liability insurance and who needs it?

HCPL — also called medical malpractice insurance — protects physicians, nurses, hospitals, and healthcare organizations against claims of negligence, errors, or inadequate patient care. Any licensed provider or facility delivering patient care needs it. In many states and credentialing arrangements, carrying it is a legal or contractual requirement.

Are HCPL insurance premiums expected to keep rising through 2026?

All current indicators point to continued upward pressure. Nearly half of all reported premiums increased in 2024, and the market is tracking toward hard market conditions. The pace will vary significantly by state and specialty, with high-litigation jurisdictions like Pennsylvania, Illinois, and Florida facing the sharpest increases.

What does a "hard market" mean for healthcare providers buying HCPL insurance?

In a hard market, premiums rise, underwriting standards tighten, some carriers reduce their appetite or exit entirely, and coverage at desired limits becomes harder to obtain. Renewing early and working with a broker who has access to multiple carriers becomes especially important when market conditions tighten.

How does third-party litigation funding affect medical malpractice claims?

TPLF enables outside investors to finance plaintiff lawsuits in exchange for a share of the award. This pushes plaintiffs toward larger verdicts rather than early settlements, driving up average claim sizes and prompting carriers to price risk more conservatively.

Does using AI tools or telehealth increase a healthcare organization's liability exposure?

Yes — both introduce liability questions that many current HCPL policies don't clearly address, including who is responsible for a technology-driven error and whether the standard of care was met in a virtual-only visit. Healthcare organizations using these tools should verify their coverage explicitly includes these scenarios.

What coverage limits should a healthcare organization carry for professional liability?

Limits vary based on specialty, state, organization size, and claims history — and healthcare consolidation has raised the stakes considerably. Physicians and health systems should review whether current limits reflect actual exposure, especially after acquisitions or the addition of high-risk service lines.