Introduction

The numbers are hard to ignore. Even cautious, well-documented clinicians are facing claims they never anticipated — and the financial scale of those claims keeps climbing.

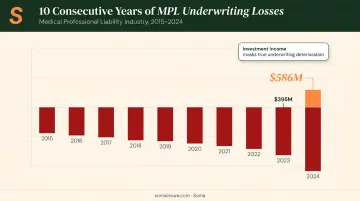

According to data cited by CNA, 57 U.S. medical malpractice verdicts exceeded $10 million in 2023, and 50% of those nuclear verdicts surpassed $25 million. AM Best reported the MPL composite recorded its 10th consecutive underwriting loss in 2024, with losses worsening to $586 million from $395 million the prior year.

The professional liability insurance market for healthcare is responding. Premiums are rising, capacity is tightening in higher layers, and the forces driving that shift are more structural than cyclical.

This article covers:

- What's actually happening in the market right now

- Which trends are pushing claim costs higher

- Which specialties carry the most exposure

- What healthcare providers can do before the next renewal

TL;DR

- Nuclear verdicts (defined as $10M+) hit 57 in 2023 — half exceeded $25M

- The MPL market recorded a $586M underwriting loss in 2024, signaling sustained pricing pressure

- Claim costs are rising structurally — driven by social inflation, third-party litigation funding, and weakening tort reform protections

- High-risk specialties include OB/GYN, neurosurgery, emergency medicine, and general surgery

- Emerging risks — AI liability and post-Dobbs criminal exposure — create uninsured gaps that standard MPL policies don't cover

- Healthcare providers who review coverage now — before a claim — are better positioned to avoid catastrophic out-of-pocket exposure

What Is Professional Liability Insurance in Healthcare?

Medical professional liability (MPL) insurance protects licensed healthcare professionals and facilities against claims of negligence, errors, or omissions that result in patient harm. It's distinct from general liability insurance, which covers physical risks like slip-and-fall injuries or property damage — neither of which touches the clinical decisions driving most healthcare claims.

Policy Structures: Claims-Made vs. Occurrence

Two primary structures define how MPL policies respond to claims:

- Claims-made: The most common MPL structure — covers claims filed while the policy is active. Requires a tail endorsement (extended reporting period) when a policy is canceled or a carrier changes, to preserve coverage for incidents that occurred during the active period but are reported later.

- Occurrence-based: Covers any incident that happened during the policy period, regardless of when the claim is filed. No tail needed, but these policies are less commonly available in today's market.

Claims-made with tail protection is the structure most providers carry today. Overlook tail coverage when switching jobs, retiring, or changing carriers — and you're personally exposed to claims filed long after your policy lapsed.

Who Needs MPL Coverage?

Any licensed professional or facility delivering direct patient care needs MPL coverage. That includes:

- Physicians, surgeons, and specialists

- Nurses and advanced practice clinicians

- Allied health professionals (physical therapists, radiologists, etc.)

- Outpatient clinics and ambulatory care centers

- Hospitals and inpatient facilities

- Telehealth providers delivering direct clinical care

The State of the Healthcare Professional Liability Market Right Now

The MPL market spent roughly a decade in a soft phase — stable or declining premiums, broad capacity, and competitive pricing. That phase is over.

Underwriting Losses Are Driving Structural Change

AM Best's 2024 report shows that loss and loss adjustment expenses (LAE) growth outpaced premium growth, producing a $586 million underwriting loss — the 10th consecutive year of underwriting losses for the MPL composite. Carriers that remained profitable did so largely through investment income, not underwriting results. Investment income can mask underwriting problems for only so long — and carriers are now repricing to reflect actual loss experience.

Primary layers (ground-up coverage to $1M–$2M) have remained relatively stable with available capacity. Excess and reinsurance layers are where the hardening is most pronounced — reinsurers are raising premiums, requiring higher retentions, and becoming more selective about which risks they'll take on.

Milliman's 2025 MPL update selected hospital professional liability severity trends of 5.0% unlimited and 4.5% capped at $5M — both half a point higher than their 2023 estimates. That upward revision reflects the reality that claim severity is outrunning earlier projections.

Hospital Consolidation Is Amplifying Exposure

When a physician practicing under a $1M individual policy joins a large health system, the coverage structure changes — and so does the verdict exposure. Claims against that physician no longer carry a $1M practical ceiling. Plaintiffs' attorneys recognize the shift in defendant resources, and settlements and verdicts scale to match.

Key exposure shifts that come with consolidation:

- Policy limits become irrelevant — health system assets create de facto deeper pockets regardless of individual coverage caps

- Verdict expectations rise — juries and plaintiffs adjust valuations when the defendant is a large institution rather than a solo practitioner

- Coverage structure gaps emerge — individual policies written before consolidation may not align with a system's master program terms

Reinsurer Behavior and AI Coverage Questions

Reinsurers are raising retention requirements and asking harder questions about emerging exposures — particularly around AI-assisted diagnostics and clinical decision support tools. Whether AI-related claims fall within traditional MPL policy language is an open question that carriers and reinsurers are actively debating.

Providers integrating AI tools should review their current policy language for three specific gaps:

- Whether AI-assisted decisions qualify as covered "professional services"

- How liability is allocated when a clinical decision support tool contributes to a misdiagnosis

- Whether the carrier has issued any AI-specific endorsements or exclusions since the policy was written

Key Trends Driving Rising Claims Costs and Severity

Social Inflation and Shifting Jury Dynamics

Swiss Re defines social inflation as increased claims severity beyond what economic factors alone explain — and reports that U.S. liability claims costs rose 57% over the past decade, with a peak annual rate of 7% in 2023.

In healthcare, several forces are converging:

- Eroding institutional trust: A 2024 JAMA Network Open study found adults reporting high trust in physicians and hospitals dropped from 71.5% in April 2020 to 40.1% by January 2024. Jurors don't arrive at trial neutral — they arrive with opinions shaped by years of news and personal experience.

- Younger jury pools: Financially stretched younger jurors often view large healthcare organizations as corporate defendants with resources to absorb large verdicts — and sometimes as institutions that failed them personally.

- Plaintiff litigation strategy: Attorneys increasingly name only the corporate healthcare entity as defendant rather than individual physicians. This exploits institutional distrust and can still expose physicians later through contribution claims, even if they were never formally named in the lawsuit.

Nuclear Verdicts and Litigation Funding

Nuclear verdicts — jury awards of $10 million or more — are no longer outliers. In 2023, 57 medical malpractice verdicts exceeded $10 million, and the 50 largest verdicts that year had a higher average award than any prior year on record.

Third-party litigation financing (TPLF) is amplifying this trend. Outside investors fund plaintiff lawsuits in exchange for a share of any recovery. The practical effects:

- Lowers the financial barrier for filing claims, including weaker ones

- Allows plaintiffs to reject early settlement offers that would otherwise end cases

- Prolongs litigation, increasing defense costs for providers and insurers

- Introduces a party whose financial interests are served by maximum recovery, not reasonable resolution

Swiss Re estimated global TPLF investment at $17 billion in 2020, with the U.S. accounting for roughly 52% of that activity. The market has grown since, and remains largely unregulated.

Tort Reform Erosion

Damages caps have historically constrained MPL claim costs in states that enacted them. That constraint is weakening.

California's MICRA — long considered a model tort reform — capped noneconomic damages at $250,000 for decades. AB 35, effective January 1, 2023, raised that cap to $350,000 for non-death injury claims and $500,000 for wrongful death cases.

Both figures are scheduled to increase annually, ultimately reaching $750,000 and $1 million respectively, then adjusting for inflation.

That change effectively raises the floor for settlements and verdicts in California, and signals to other states that once-settled caps can be revisited. New York is among 17 states with no damages cap at all, and there's limited political appetite in those states for implementing one.

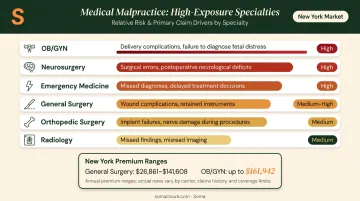

Which Healthcare Specialties Face the Highest Exposure?

Surgical specialties consistently generate the highest malpractice frequency and total claim costs — CRICO's national data confirms this. But certain specialties attract disproportionate attention from plaintiff attorneys for reasons that go beyond surgical volume.

High-Exposure Specialties and Why They're Targeted

| Specialty | Primary Claim Driver |

|---|---|

| OB/GYN | Birth injury verdicts with high emotional weight |

| Neurosurgery | Permanent injury; large damages calculations |

| Emergency medicine | Stroke/MI cases argued in hindsight |

| General surgery | High procedure volume; complications leading to death or reoperation |

| Orthopedic surgery | Implant failures with long-term functional consequences |

| Radiology | Missed or delayed cancer diagnoses; heavy hindsight bias |

Radiology and emergency medicine share a common vulnerability: attorneys reconstruct what a "reasonable" clinician would have caught from the same images or patient presentation — after the outcome is already known. Coverys data shows office-based settings account for 34% of diagnosis-related events and 38% of indemnity paid nationally, meaning the diagnostic accuracy problem reaches well beyond the emergency department.

That risk exposure translates directly into premium costs. In New York, for example, general surgery premiums range from roughly $26,861 in Rochester to $141,608 on Long Island, with OB/GYN major surgery premiums reaching $161,942 in certain territories. State, limits, and claims history all factor in heavily.

Emerging Risks Adding New Layers of Complexity

Criminalization of Medicine

Post-Dobbs, healthcare providers in certain states now face criminal liability risk for procedures that were standard of care until recently. The Marquette Law Review documented in 2024 that providers have begun requesting professional liability coverage that addresses criminal exposure — not just civil malpractice claims.

Standard MPL policies have historically excluded criminal defense costs. A specialty product is now available to address this: Physicians Insurance introduced a criminal defense reimbursement endorsement in 2022, priced at $150/year for solo policies and up to $4,000 for hospital liability policies. This coverage gap is worth examining for any provider operating in states where the legal environment around certain procedures has changed.

AI and Digital Health Liability

As AI-assisted diagnostics, clinical decision support tools, and automated triage systems move into routine clinical workflows, a core question remains unanswered by most current policy language: when an AI tool contributes to a harmful outcome, who bears the liability — the provider, the hospital, or the vendor?

Reinsurers are already asking this question, and the answer matters for how claims get allocated. Providers adopting these tools should take concrete steps to assess their exposure:

- Review current MPL policy language for AI-related exclusions or gaps

- Confirm whether the AI vendor's product liability coverage overlaps with or excludes clinical harm claims

- Work with their broker to document how new technology is being used, so coverage can be structured appropriately

Settlement Behavior Under Pressure

When the cost of a single adverse verdict can reach $25 million or more, the calculus around defending cases changes. Some organizations are moving toward earlier settlement on defensible cases to avoid that exposure.

The risk runs deeper than a single payout. If earlier settlement becomes the default, it signals to plaintiff attorneys that filing claims (even weak ones) carries a higher probability of recovery. That dynamic can increase both filing frequency and severity over time — a pattern carriers are actively monitoring in their pricing models.

Takeaway for risk managers: Track your organization's settlement patterns and evaluate whether early resolution on defensible cases is creating downstream exposure in your loss history.

How Healthcare Providers Should Respond

Conduct a Proactive Coverage Review

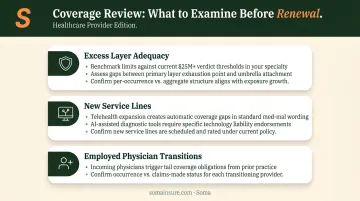

Don't wait for renewal. The gap between what a policy provides and what a current verdict environment demands may be larger than it appears. Specific areas to examine:

- Excess layer adequacy — Is your coverage tower structured to absorb a $25M+ verdict, or does it top out well below that?

- New service lines — Telehealth, AI-assisted tools, and new outpatient locations may not be automatically covered under existing policies

- Employed physicians — When independent practitioners join your organization, confirm their coverage transitions properly and that tail obligations from prior claims-made policies are addressed

Understand the Policy Structure Details

In a hardening excess market, the nuances in policy structure carry real financial weight:

- Retention levels — Are self-insured retention amounts appropriate for your organization's cash flow?

- Tail coverage — Claims-made policies require this when the policy ends or the provider changes carriers. Overlooking it is one of the most costly coverage mistakes in healthcare

- Contribution claims and criminal defense — Confirm whether your policy responds to contribution claims from co-defendants and whether any criminal defense coverage exists or needs to be added by endorsement

Select Carriers on More Than Price

A carrier that settles defensible cases quickly may reduce short-term costs while quietly inviting more claims. In a market where insurer appetites vary widely, carrier financial strength and claims philosophy matter alongside price.

AM Best ratings and loss reserves provide one measure of financial stability. Equally important is whether a carrier will actually defend a case vigorously when the facts support it — or whether their default is early settlement to manage expenses.

Work with a Broker Who Knows This Market

Healthcare professional liability — especially for hard-to-place risks, high-risk specialties, or excess layers — requires a broker with genuine access to specialty markets and experience structuring these programs.

That's where Soma comes in. Soma builds healthcare insurance programs for outpatient clinics, inpatient facilities, ambulatory providers, and allied health professionals through specialty markets including CRC Group, Chubb, and Kinsale. For providers whose risk profile doesn't fit standard admitted markets, access to surplus lines and specialty carriers can be the difference between solid coverage and a gap that surfaces the moment a claim is filed.

Frequently Asked Questions

What is professional liability insurance in healthcare?

It's a specialized policy protecting licensed healthcare professionals and facilities against negligence, errors, or omissions claims resulting in patient harm. Unlike general liability insurance — which covers physical risks like property damage — MPL insurance specifically addresses clinical care decisions and professional services.

What are the 4 C's of malpractice?

The 4 C's — Caring, Communication, Competence, and Charting — form the standard risk management framework for reducing malpractice exposure. Each addresses a distinct layer: patient rapport, clear documentation, clinical standards, and accurate recordkeeping.

What is the difference between claims-made and occurrence-based coverage?

Claims-made policies cover claims filed while the policy is active; occurrence policies cover any incident that happened during the policy period regardless of when the claim is filed. Providers switching or canceling a claims-made policy typically need a tail endorsement to preserve coverage for incidents from the active policy period.

Which medical specialties pay the most for malpractice insurance?

Neurosurgeons, OB/GYNs, and cardiac surgeons consistently face the highest premiums due to the severity of potential outcomes and elevated litigation rates. Premiums vary substantially by state and practice location — New York OB/GYN major surgery premiums, for example, can exceed $160,000 annually in certain territories.

How do nuclear verdicts affect my healthcare liability insurance premiums?

Nuclear verdicts raise insurers' loss projections, putting upward pressure on premiums, particularly in excess layers. They can also prompt carriers to reduce capacity or exit the market entirely, making high-limit coverage more expensive and harder to place at renewal.