This article is for business owners across construction, hospitality, healthcare, manufacturing, and other complex industries who need a clear-eyed view of what's driving CGL costs in 2025, where the genuine coverage gaps are, and what steps actually move the needle at renewal.

TLDR

- CGL rate increases moderated to the 4%–5% range in mid-2024, but hard market conditions persist for high-risk industries

- Nuclear verdicts (jury awards exceeding $10M) hit a record 135 in 2024 — the biggest driver of insurer caution today

- Standard CGL policies increasingly exclude biometric data, PFAS claims, and violent incidents, leaving coverage gaps most businesses haven't identified or addressed

- Documented risk management programs now directly affect underwriting decisions — and can improve your rate

- Businesses in construction, hospitality, healthcare, and retail face the toughest market conditions heading into 2025

The 2025 CGL Market at a Glance

Stabilization, Not Softening

MarketScout's quarterly data shows General Liability increases running in the 3.25%–4.7% range across 2024 — a meaningful step down from the 6.7% GL increases seen in Q4 2022 and broader casualty pressures in prior years. Into early 2025, primary GL held at roughly 2.3%–3.7% per quarter.

That moderation is real, but it doesn't mean underwriters are relaxing. What changed is the rate of increase — not the scrutiny applied to each submission.

Carriers are now evaluating businesses more granularly before quoting:

- Industry class — appetite varies sharply by sector; some classes face limited carrier options even in a moderating market

- Loss history — one large claim can move a business out of standard markets entirely, often within a single renewal cycle

- Operational risk profile — underwriters are mapping specific third-party exposures, not just reviewing SIC codes

- Risk management maturity — documented safety programs and incident logs can meaningfully improve terms, not just signal good intent

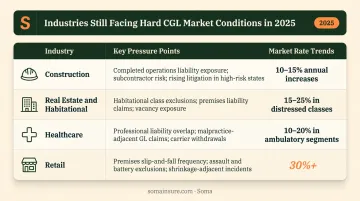

Where the Hard Market Persists

Tighter underwriting standards tell only part of the story. For certain sectors, rate pressure hasn't eased — it's intensified. Not every business saw relief. Several sectors remain in genuinely difficult conditions:

| Industry | Key Pressure Points |

|---|---|

| Construction | Completed operations claims, subcontractor liability, frame residential |

| Real estate / habitational | Deteriorating loss activity; Amwins projected 10%–15% primary GL increases for underperforming accounts |

| Healthcare | Excess casualty constraints; umbrella increases of 30%+ for facilities with adverse experience |

| Retail | Double-digit primary rate increases expected in 2025 for many accounts |

Businesses in these sectors cannot assume that headline rate moderation applies to their renewal.

Litigation and Social Inflation: The Biggest Cost Driver in CGL

What Social Inflation Actually Means

Social inflation describes claim severity growing faster than economic drivers — more lawsuits, larger verdicts, and legal strategies specifically designed to maximize payouts. Swiss Re estimates US social inflation ran at 5.4% annually from 2017–2022, compared to 3.7% general economic inflation over the same period. That gap compounds quickly across a book of CGL claims.

For businesses, this means two things: claims that once settled informally are going to trial, and trial outcomes are increasingly unpredictable.

Third-Party Litigation Funding

Third-Party Litigation Funding (TPLF) is a structural accelerant: hedge funds and investment firms finance plaintiff lawsuits in exchange for a share of the settlement. Swiss Re estimated global TPLF investment at $17 billion in 2020, with the US accounting for 52% of all activity — and projected the market reaching $31 billion by 2028.

When external financing removes a plaintiff's pressure to settle early, cases that once resolved quietly now go to trial. Defense costs rise. Settlement floors rise with them.

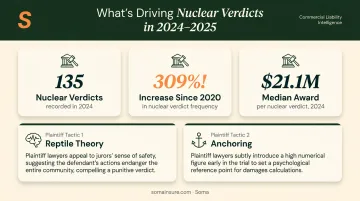

Nuclear and Thermonuclear Verdicts

The Insurance Institute for Legal Reform analyzed 1,288 nuclear verdicts ($10M+) from 2013–2022, with a median award of $21.1 million and a mean of $89 million. Marathon Strategies recorded 135 nuclear verdicts in 2024 alone — the highest in their dataset — with frequency up 309% since 2020.

Plaintiff attorneys use two well-documented tactics to reach these figures:

- Reptile theory — framing defendants as a danger to community safety, triggering emotional rather than rational jury responses

- Anchoring — requesting an exorbitant damages number to establish a psychological reference point, even when the actual award comes in lower

Coverage limits set three or four years ago may leave serious gaps against today's verdict landscape — worth revisiting before renewal.

Attorney Advertising Amplifies the Pipeline

Plaintiffs' firms now spend approximately $1 billion annually on TV advertising, with broadcast legal-services spend up 44% in Los Angeles and 137% in New Orleans between 2012 and 2019. That advertising is generating more claimants — particularly for slip-and-fall, premises liability, and products claims that fall squarely within CGL.

Taken together, these forces — TPLF financing, nuclear verdicts, and aggressive plaintiff marketing — are reshaping what adequate CGL limits look like. Businesses in high-exposure industries should treat limit adequacy as an annual question, not a set-it-and-forget-it decision.

Emerging Operational Risks Creating New CGL Exposure

Biometric Data Liability

Businesses using facial recognition, fingerprint scanners, or iris-based access systems for employee time-tracking or security are accumulating biometric data liability — often without realizing their CGL policy may not cover it.

State-level biometric privacy laws are expanding rapidly. Key developments to know:

- Illinois, Texas, and Washington have enacted private-sector biometric privacy statutes

- The Illinois Supreme Court (West Bend v. Krishna) found BIPA claims can trigger CGL personal and advertising injury coverage

- ISO filed updated exclusions in March 2023 specifically targeting biometric information — meaning many standard policies now explicitly exclude what businesses assumed was covered

What to do: If your business collects biometric data in any form, review your CGL policy exclusions carefully. Cyber liability coverage may fill part of this gap, but the overlap is policy-specific and requires a broker review.

Biometric exposure is one piece of a larger picture. Emerging environmental risks are generating equally complex coverage questions.

PFAS ("Forever Chemical") Liability

PFAS are synthetic chemicals used in packaging, textiles, cookware, and firefighting agents. They accumulate in the environment and the human body without breaking down — which is why the litigation wave is so complex for CGL purposes.

The scale of exposure is significant: 3M's PFAS settlement with public water suppliers reached up to $10.3 billion, approved in March 2024. DuPont, Chemours, and Corteva agreed to a separate $1.185 billion water district settlement fund.

The CGL coverage problem runs on two tracks:

- PFAS exposure accumulates over years or decades, meaning claims surface long after the exposure period

- ISO published PFAS-specific exclusion endorsements in June 2023, and courts in Georgia and New York have upheld total pollution exclusions to deny PFAS defense obligations

Manufacturers, packaging companies, and businesses using PFAS-containing materials should review their current policy language and explore whether specialty environmental coverage closes that coverage gap.

Physical and chemical risks aside, the liability landscape also includes a threat that's harder to plan for: workplace violence.

Active Assailant Exposure

The FBI recorded 229 active shooter incidents from 2019–2023 — an 89% increase over the prior five-year period. For businesses, the consequences extend well beyond the immediate tragedy: negligent security lawsuits, business interruption losses, and reputational damage all follow.

Standard CGL policies frequently exclude claims tied to violent acts, mental anguish, or emotional trauma. Businesses in hospitality, retail, healthcare, and entertainment venues should evaluate whether standalone active assailant coverage or specific endorsements are appropriate — carriers offer dedicated limits up to $100 million.

Industries Under the Most Pressure in 2025

Each high-risk sector faces distinct pressures that standard CGL markets are pricing carefully:

Construction — Completed operations claims can surface years after project completion. Subcontractor risk, bodily injury frequency on job sites, and jurisdictional severity (particularly in New York) keep this class firmly in hard market territory. Amwins cited 5%–10% renewal increases for New York construction GL in recent guidance.

Hospitality — Active assailant exposure, liquor liability, slip-and-fall litigation, and premises liability combine to create limited carrier appetite, particularly for late-night venues, high-occupancy event spaces, and mixed-use properties. Mainstream brokers routinely decline these placements.

Healthcare — Excess casualty markets remain constrained, with umbrella increases of 30%+ reported for facilities with adverse loss experience. Patient data exposure adds biometric and cyber liability dimensions that intersect with CGL personal and advertising injury provisions.

Retail and Manufacturing — Retailers face double-digit primary rate increases in some accounts. Manufacturers dealing with PFAS-containing products face the compound problem of pollution exclusions and long-tail claim exposure.

For businesses in these sectors that face non-renewals or carrier declinations, surplus lines and specialty markets become the critical access point. The excess and surplus lines market processed $81 billion in premium through stamping offices in 2024, up 12.1% year-over-year — a direct reflection of this shift away from standard carriers.

Soma places CGL across all of these categories — construction, hospitality, healthcare, and manufacturing — working with carrier partners including Chubb, Markel, Kinsale, and Liberty Mutual to find capacity where standard markets won't go.

What Businesses Should Do Before Their Next CGL Renewal

Document Your Risk Management Programs

Carriers reward businesses that can demonstrate formal, written risk management. Strong documentation works on two fronts: it supports better underwriting rates and serves as evidence of reasonable care if a claim goes to litigation.

Specific materials that support CGL underwriting today:

- Written active assailant response plans and employee training logs

- Biometric data handling and consent policies

- PFAS inventory and mitigation documentation for relevant operations

- Incident response records and claim history narratives

Underwriters notice the difference between a business that can produce organized documentation and one that can't — and so does pricing.

Review Your Limits Honestly

Given the current verdict environment — 135 nuclear verdicts in 2024, median award of $21.1 million — limits that made sense three years ago may be inadequate today. Work with an advisor to benchmark your current limits against recent verdict data. Key areas to review:

- Bodily injury limits relative to nuclear verdict trends in your industry

- Personal and advertising injury limits, especially if your operations involve digital marketing or content

- Products/completed operations limits benchmarked against your geography's jury award history

Evaluate Coverage for Emerging Risks

Standard CGL now has documented exclusions for three significant exposure categories:

- Biometric data — ISO exclusion filed March 2023

- PFAS — ISO exclusion endorsements published June 2023

- Violent acts — standard exclusions often bar active assailant claims

Discuss with your broker which endorsements address these gaps, whether cyber liability addresses the biometric data exposure, and whether active assailant coverage makes sense for your specific operations.

Work With a Broker Who Knows the Hard-to-Place Market

For businesses in high-risk industries — or those who've received non-renewal notices from standard carriers — carrier access matters as much as the coverage terms themselves. Soma places CGL for complex, hard-to-insure businesses across hundreds of carrier partners. The direct placement process is built for speed — no waiting weeks for quotes or chasing responses from brokers unfamiliar with your industry.

Frequently Asked Questions

What does a standard commercial general liability policy cover?

A standard CGL policy covers third-party bodily injury, property damage, personal and advertising injury, products and completed operations liability, and medical payments to injured parties. It does not cover professional errors, employee injuries, intentional acts, or — increasingly — biometric data and PFAS-related claims where specific exclusions apply.

What triggers coverage on a commercial general liability policy?

Most CGL policies are occurrence-based: coverage triggers when the injury or property damage actually happens during the policy period — not when the claim is filed. This matters most for slow-developing exposures like PFAS contamination, where claims surface years after the actual exposure ended.

Which industries face the hardest CGL market conditions in 2025?

Construction, real estate/habitational, healthcare, hospitality, retail, and manufacturing are all facing elevated scrutiny, higher premiums, or limited standard carrier availability. The common thread is claim frequency, litigation exposure, and operational complexity that pushes these risks toward specialty markets.

How does social inflation affect my CGL premiums?

Social inflation raises claim costs through larger jury awards and more frequent lawsuits. Insurers price for industry-wide trends, so a business with a clean record can still see premium increases based on what's happening across similar operations.

Are PFAS-related claims covered under a standard CGL policy?

Many standard CGL policies include absolute pollution exclusions that carriers apply to deny PFAS claims. ISO published specific PFAS exclusion endorsements in 2023, so businesses that handle PFAS-containing products should review their policy language and consider specialty environmental coverage.

What can I do to lower my CGL premiums in today's market?

Documented risk management is the strongest underwriting lever available: safety training records, incident logs, compliance protocols, and written response plans all demonstrate lower risk to carriers. Working with a broker who has access to multiple specialty markets produces better pricing than staying with a single carrier relationship.