Without the right coverage, those costs come directly out of your pocket.

Commercial general liability (CGL) insurance is the foundational policy that protects businesses from exactly these scenarios. This guide covers what CGL is, what it covers, what it excludes, who needs it, what it costs, and how to get the right policy for your business.

One important note upfront: CGL is one of the most commonly required coverages in business. Clients demand proof before signing contracts. Landlords require it before handing over keys. Government contracts mandate it. If you're running a business without it, you're likely already out of compliance with at least one agreement.

TL;DR

- CGL protects businesses from third-party claims involving bodily injury, property damage, personal injury, and advertising injury.

- It covers legal defense costs, medical expenses, and settlements, including costs before any court judgment is reached.

- Standard limits are typically $1 million per occurrence / $2 million aggregate, though requirements vary by industry and contract.

- CGL does not cover professional errors, employee injuries, or damage to your own property.

- Premiums vary by industry, revenue, location, and claims history — high-risk businesses should work with a specialized broker to find the right fit.

What Is Commercial General Liability (CGL) Insurance?

CGL insurance is a commercial policy that protects a business from financial loss when a third party — a customer, vendor, or bystander — suffers bodily injury, property damage, or certain non-physical harms as a result of the business's operations, premises, or products.

It's distinct from personal liability coverage on a homeowners or renters policy. Personal policies are designed for individual risks. CGL addresses the distinct exposures that come with running a business: customer interactions, products you sell, and advertising you publish.

Occurrence vs. Claims-Made Policies

Most CGL policies are written on an occurrence basis — meaning the policy covers any incident that happens during the policy period, regardless of when the claim is actually filed. A customer injured in your store in October could file a lawsuit two years later, and your October policy still responds.

A claims-made policy works differently: coverage triggers when the claim is filed, not when the incident occurred. If your policy has lapsed by then, you're unprotected — unless you've purchased tail coverage (an extended reporting period).

Claims-made structures are more common in professional liability, but ISO offers claims-made CGL forms and some specialty markets use them. Know which form you're buying before you sign.

How a Standard CGL Policy Is Structured

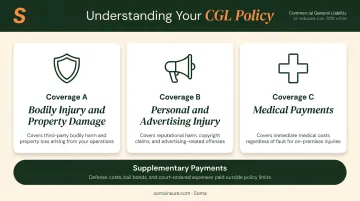

Per the ISO CG 00 01 coverage form, a standard CGL policy is organized into three main coverage parts:

- Coverage A : Bodily Injury and Property Damage Liability

- Coverage B : Personal and Advertising Injury Liability

- Coverage C : Medical Payments

The policy also includes Supplementary Payments provisions that cover items like appeal bond premiums, first aid costs, and investigation expenses — generally paid in addition to policy limits, so they don't erode your coverage.

What Does Commercial General Liability Insurance Cover?

Coverage A – Bodily Injury and Property Damage

This is the core of the policy. Coverage A pays damages the insured is legally obligated to pay when someone (other than an employee) is physically injured or their property is damaged due to the business's operations, premises, or products.

Practical examples:

- A customer slips on a wet floor in a retail store

- A contractor's crew damages a client's hardwood floors during a renovation

- A product causes injury after it's sold and leaves the business's control

Coverage B – Personal and Advertising Injury

This covers non-physical harms: libel, slander, copyright infringement in advertising, wrongful eviction, and malicious prosecution. It's most relevant for businesses that publish content, run ad campaigns, or operate in real estate or media — where a poorly worded ad or disputed content can generate serious legal exposure.

Coverage C – Medical Payments

Coverage C pays the immediate medical expenses of someone injured on your premises or by your operations, regardless of fault, up to a sublimit on the declarations page. IRMI identifies $5,000 per person as a typical figure for premises medical payments, though amounts vary by policy.

Paying a minor claim quickly reduces the chance it escalates into a lawsuit — which is the real value of this coverage.

Defense Costs and Legal Fees

One of CGL's most valuable features is that it funds your legal defense — attorney fees, court costs, expert witnesses — even if the claim against you is ultimately unfounded.

How defense costs are structured matters significantly for your actual protection:

| Defense Cost Structure | What It Means |

|---|---|

| Outside the limit | Attorney fees and defense expenses don't reduce your coverage limits |

| Inside the limit | Every dollar spent on legal defense erodes the amount available for settlements or judgments |

IRMI notes that standard CGL policies treat defense as outside the limits — but this varies by policy form, so confirm it before binding coverage.

Coverage Limits: Per-Occurrence and Aggregate

Understanding how defense costs are structured leads directly to the next question: how much coverage do you actually have? CGL policies set limits in two ways:

- Per-occurrence limit — the maximum paid for any single incident

- Aggregate limit — the total maximum paid across all claims in a policy period

The most common benchmark is $1M per occurrence / $2M aggregate, which The Hartford and Insureon both identify as standard for small businesses. Higher limits — $2M/$4M or excess layers through a commercial umbrella — are common in construction, manufacturing, and hospitality.

What CGL Insurance Does Not Cover

Understanding what CGL excludes matters as much as knowing what it covers. Several common business risks fall completely outside the policy — each requiring its own separate coverage.

Professional errors and omissions — CGL doesn't cover claims tied to professional advice or service failures. An accountant who gives incorrect tax guidance — or a consultant whose recommendation costs a client money — needs a separate Professional Liability (E&O) policy for those claims.

Employee injuries — Bodily injury to employees is explicitly excluded from CGL. That exposure belongs to workers' compensation insurance. Separately, claims involving wrongful termination or discrimination require Employment Practices Liability (EPL) coverage.

Your own business property — Damage to your building, equipment, or inventory isn't covered by CGL. That falls under commercial property insurance. For many small to mid-size businesses, a Business Owner's Policy (BOP) bundles CGL with property coverage in a single, typically discounted package.

Other standard exclusions, per the ISO form and the Texas Department of Insurance, include:

- Auto liability (owned, rented, or operated vehicles)

- Intentional acts

- Liquor liability (in some forms)

- Contractual liability (with exceptions)

- Pollution liability

- Damage to property in the insured's care, custody, or control

Every exclusion on this list has a corresponding coverage product designed to fill it. Knowing the gaps upfront makes it easier to build a complete coverage stack rather than discover a hole after a claim.

Who Needs Commercial General Liability Insurance?

Nearly every business needs CGL — specifically any operation that interacts with the public, works on client premises, manufactures or sells products, or runs any form of advertising.

According to NEXT Insurance's 2025 report, **62% of small firms carry general liability insurance** — up from 51% in 2023. That still leaves a meaningful portion of businesses exposed. And carrying some coverage isn't the same as carrying enough: Hiscox's 2025 Underinsurance report found that 77% of U.S. small businesses are underinsured.

Industry-by-Industry Breakdown

| Industry | Why CGL Matters |

|---|---|

| Construction & Contractors | High physical risk; often contractually or legally required. Tennessee, for example, mandates proof of general liability for contractor license renewal. |

| Retail & Hospitality | Customer-facing premises create constant slip-and-fall and property damage exposure. |

| Healthcare | Patient interaction creates bodily injury risk; facilities often required to carry coverage. |

| Technology & Consulting | Lower physical risk, but Coverage B (advertising injury, copyright infringement) is genuinely relevant. |

| Manufacturing | Products liability exposure — injury or damage caused by goods after they leave your facility. |

| Security Agencies | State licensing boards in many states require proof of insurance and surety bonds before issuing or renewing a security company license. |

Who Else Gets Left Exposed

Home-based businesses and sole proprietors aren't automatically protected. Most homeowners policies specifically exclude business liabilities, and the Insurance Information Institute notes that typical homeowners coverage for business equipment caps at $2,500 — with only $250 applying off-premises. CGL fills that gap directly.

Businesses renting commercial space face a different but equally firm requirement. Hiscox reports that most commercial leases require tenants to carry at least $1M per occurrence and $2M aggregate, with landlords typically requiring to be named as an additional insured.

How Much Does Commercial General Liability Insurance Cost?

CGL premiums vary widely based on your business's risk profile, but real benchmarks give you a reasonable starting point.

Insureon's data puts the average small business premium at $45/month ($538/year), with a range of roughly $250 to over $3,000 annually. The Hartford's portfolio average is approximately $810/year. Both figures reflect the diversity of risks insured.

Industry Cost Benchmarks (Insureon Data)

| Industry | Median Monthly Cost | Median Annual Cost |

|---|---|---|

| Consulting | $29 | ~$350 |

| Food & Beverage | $44 | ~$525 |

| Restaurants | $141 | ~$1,691 |

| General Contractors | $142 | ~$1,700 |

The gap between consulting and contracting shows how much industry type drives pricing. A contractor on a job site with heavy equipment faces exposure that a freelance consultant working from an office simply doesn't.

Key Rating Factors

Insurers evaluate several variables when calculating your premium:

- Industry and type of work — the largest single factor; high-risk trades pay multiples of what professional services pay

- Annual revenue and payroll — larger operations generate more touchpoints with clients and the public, which raises exposure

- Number of employees — more people, more potential for incidents

- Geographic location — states with higher litigation rates push premiums up

- Prior claims history — a clean history typically yields better rates

- Coverage limits selected — higher limits cost more; higher deductibles lower premiums but increase out-of-pocket exposure per claim

Cost-Saving Strategies

- Bundle with a BOP — combining CGL with commercial property in a Business Owner's Policy is typically less expensive than buying each separately

- Document safety protocols — formal risk management procedures can demonstrate lower exposure to underwriters

- Maintain a clean claims history — The Hartford notes this directly influences pricing

- Work with a broker who accesses multiple carriers — carrier pricing for the same risk can vary significantly; shopping the market matters

Soma places CGL coverage across industries through carriers including Chubb, Markel, Liberty Mutual, and Kinsale — including businesses that standard markets decline.

For complex operations in construction, manufacturing, hospitality, or security, carrier willingness to quote (and at what price) varies significantly. The broker you use determines what options are even on the table.

How to Get the Right CGL Coverage for Your Business

Step 1: Assess Your Risks and Requirements

Before applying for coverage, clarify two things:

- What are your actual operational exposures? (Premises, products, work performed off-site, advertising)

- What are your contractual requirements? (Client contracts, lease terms, licensing requirements)

These determine both the coverage structure you need and the minimum limits you must carry.

Step 2: Gather Your Application Information

Most CGL quotes require:

- Annual revenue and payroll

- Number of employees

- Detailed description of business operations

- Prior claims history (typically 3–5 years)

- Desired coverage limits and deductibles

Step 3: Understand Your Options — Direct vs. Broker

Buying directly from a single carrier limits you to that carrier's pricing, appetite, and available forms. If your business falls outside their preferred risk profile, you may get declined — or receive a quote that doesn't accurately reflect your exposure.

An independent broker shops multiple carriers simultaneously and can access specialty markets for risks that standard carriers won't touch. For businesses in construction, hospitality, healthcare, or security — where carrier appetite varies significantly — that access can be the difference between adequate coverage and a policy full of gaps.

Soma places CGL and related coverages for complex and hard-to-insure businesses, including operations that standard markets routinely decline. Working with carrier partners across admitted and surplus lines markets (including Kinsale and CRC Group), Soma's Risk Management Team evaluates your exposures and places coverage without the back-and-forth typical of traditional brokers.

Frequently Asked Questions

How much is commercial general liability insurance?

Premiums vary by industry, business size, location, and limits. Insureon's data shows an average of $45/month, with annual costs ranging from around $250 to over $3,000. High-risk industries like construction pay considerably more than lower-risk businesses like consulting. Getting a quote from a licensed broker is the most accurate way to know your actual cost.

What is included in commercial general liability insurance?

CGL covers three parts: bodily injury and property damage (Coverage A), personal and advertising injury such as libel or copyright infringement (Coverage B), and medical payments for minor on-premises injuries (Coverage C). Legal defense costs are also included, typically outside policy limits.

What does commercial general liability insurance not cover?

CGL excludes professional errors and omissions, employee injuries (covered under workers' compensation), damage to your own property, auto liability, intentional acts, and certain contractual liabilities. Each gap has a corresponding separate policy.

Do I need CGL if I'm a sole proprietor or home-based business?

Yes. Sole proprietors and home-based businesses face the same third-party liability risks as any other business, and homeowners policies specifically exclude business liabilities. CGL provides the protection that personal policies don't cover for business-related claims.

What's the difference between a CGL policy and a BOP?

A Business Owner's Policy (BOP) bundles CGL with commercial property coverage at a lower combined cost than buying each separately. A standalone CGL covers liability only. BOPs work well for most small to mid-size businesses; larger or higher-risk operations typically need individually structured policies.

What's the difference between an occurrence and a claims-made CGL policy?

An occurrence policy covers incidents during the policy period regardless of when the claim is filed. A claims-made policy only covers claims filed while the policy is active — if it lapses, past incidents go unprotected unless you add tail coverage (an extended reporting period).