Introduction

Most business owners assume their Commercial General Liability (CGL) policy covers the claims that matter most. Then a denial letter arrives. The standard ISO form CG 00 01 04 13 uses broad insuring agreement language — covering bodily injury, property damage, and personal and advertising injury to third parties — but that breadth has limits most policyholders never see until it's too late.

Buried after the insuring agreement are exclusions that carve out entire categories of loss: employee injuries, professional errors, pollution events, vehicle accidents, and more. Each exclusion exists for a legitimate underwriting reason. Collectively, they can leave significant gaps in a business's protection — gaps that only become visible after a claim is filed.

This guide breaks down how CGL exclusions work, what the most common ones actually say, how they affect specific industries, and — critically — how to address the gaps they create.

TL;DR

- CGL covers third-party bodily injury, property damage, and advertising injury — but 17 exclusions narrow that coverage significantly

- Employee injuries, vehicle accidents, professional errors, and pollution events are all excluded from standard CGL

- Construction, manufacturing, hospitality, and technology businesses face the biggest coverage gaps from exclusions

- Many exclusions can be addressed through endorsements or standalone policies — but only if you identify them first

- A coverage gap analysis with a knowledgeable broker is the most reliable way to find uninsured exposures before a claim reveals them

What Does a CGL Policy Actually Cover?

The ISO CG 00 01 insuring agreement states: "We will pay those sums that the insured becomes legally obligated to pay as damages because of 'bodily injury' or 'property damage' to which this insurance applies."

Two definitions drive the coverage:

- Bodily injury — physical harm, sickness, or death sustained by a third party

- Property damage — physical injury to tangible property belonging to others, including loss of use (note: electronic data is explicitly not tangible property under the ISO form)

Beyond Coverage A, a standard CGL also includes:

- Personal and advertising injury (Coverage B) — libel, slander, copyright infringement in ads

- Premises and operations — incidents occurring at your location or during ongoing work

- Products and completed operations — claims arising from your product or finished work

The insuring agreement is deliberately broad — but broad language doesn't mean limitless coverage. Carriers use exclusions to carve out specific risks they're unwilling to carry, and those carve-outs are where most coverage disputes originate.

How CGL Exclusions Work

The structure of a CGL policy follows a simple formula: insuring agreement minus exclusions = actual coverage.

The ISO CG 00 01 04 13 form contains 17 exclusions under Coverage A alone, labeled a through q. They cover everything from intentional acts and employee injuries to pollution, vehicles, and electronic data.

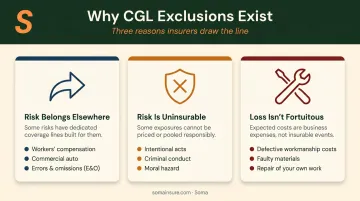

With 17 exclusions in a single coverage part, none of them are accidental. Each exists for one of three reasons:

- The risk belongs elsewhere — workers' comp covers employees; commercial auto covers vehicles; E&O covers professional advice

- The risk is uninsurable — intentional acts and criminal conduct create moral hazard

- The loss isn't fortuitous — fixing your own defective work is a business cost, not an insurable accident

Knowing which category an exclusion falls into tells you exactly where to look — a separate policy, an endorsement, or simply a different line of coverage.

The Most Common CGL Insurance Exclusions, Grouped by Type

Intentional and Criminal Acts

Exclusion a — Expected or Intended Injury — bars coverage for bodily injury or property damage that the insured deliberately caused or that was a foreseeable outcome of an intentional act. If a business owner knowingly destroys a customer's property during a dispute, there's no CGL coverage. One narrow exception: reasonable force used in self-defense is not excluded.

Criminal acts and knowing statutory violations follow the same logic. Coverage cannot extend to illegal conduct without creating perverse incentives for bad behavior.

Business Risk and "Your Work" Exclusions

This cluster of exclusions addresses a core insurance principle: CGL covers harm your work causes to others, not the cost of redoing the work itself.

What's excluded:

- The cost to repair or replace your own defective product or completed work

- Impaired property — third-party property that can't be used because it incorporates your defective component

- Recall costs — inspection, removal, or replacement of a product you recalled

What may still be covered:

- Consequential damages to third-party property caused by your defective work (courts have treated this as an "occurrence" in cases like Cypress Point Condominium Ass'n v. Adria Towers)

A concrete example: a plumber installs a faulty fitting. When it fails and floods a client's building, the CGL won't pay to replace the fitting — but it may cover damage to the building itself.

Employment-Related Exclusions

This is one of the most misunderstood pairs of exclusions in the CGL form.

- Exclusion d bars coverage for obligations under workers' compensation laws

- Exclusion e bars bodily injury claims by employees arising out of their employment

A customer who slips and falls in your store is a GL claim. An employee who slips in the same spot is not — that's a workers' comp claim. The average workers' compensation claim costs $47,316 for accidents occurring in 2022–2023, which underscores why carrying the right policy for the right risk matters.

Employer's liability exposure — lawsuits from employees or their families related to on-the-job injuries — also falls outside CGL and typically requires employer's liability coverage bundled with workers' comp.

Specialized and Categorical Risk Exclusions

Auto, aircraft, and watercraft: Any liability from owned, rented, or borrowed vehicles is excluded and requires a commercial auto policy. Mobile equipment (forklifts, tractors) is treated differently and may retain some CGL protection.

Businesses without a vehicle fleet — but whose employees occasionally use personal or rented cars for work — can close this gap with a hired and non-owned auto (HNOA) endorsement, typically without a full commercial auto policy.

Pollution: The ISO policy excludes bodily injury or property damage from the "discharge, dispersal, seepage, migration, release or escape" of any "solid, liquid, gaseous or thermal irritant or contaminant." That definition is broad — capturing smoke, fumes, chemicals, and waste. Courts have split on its scope: carbon monoxide was treated as a pollutant in some jurisdictions (Bernhardt) but not in others (Clendenin, involving welding fumes).

For construction, manufacturing, transportation, and HVAC businesses, that ambiguity is a real exposure. Pollution liability insurance fills this gap.

Liquor liability: This exclusion applies only to businesses in the business of manufacturing, distributing, selling, serving, or furnishing alcohol. A construction company that serves beer at a company BBQ is not subject to it. A bar, restaurant, or event venue is. Dram shop liability laws allow injured parties to sue alcohol servers directly, and most states have some version of these statutes on the books.

Electronic data and cyber: The ISO form is explicit: "electronic data is not tangible property." Data loss, ransomware, and system failures fall entirely outside standard CGL. According to IBM's 2025 Cost of a Data Breach Report, the average U.S. cost of a data breach reached $10.22 million in 2025 — an exposure standard CGL leaves completely unaddressed. Standalone cyber liability coverage is the only way to close it.

Contractual liability: Assuming another party's liability through a contract or hold-harmless agreement is excluded — unless the insured would have been liable regardless of the contract, or the agreement qualifies as an "insured contract" under the policy. Many commercial leases and vendor agreements trigger this exclusion, so it's worth reviewing before signing.

Industry-Specific CGL Exclusions to Watch Out For

Construction and Contracting

The "your work" and completed operations exclusions hit contractors harder than most. Construction defect claims are often reported years after a project wraps — Milliman reports defect claims can surface up to 10 years after home completion. A structural defect discovered five years later generates exactly the kind of claim that CGL's completed-operations exclusion was designed to carve out.

Subcontractor work creates an additional gap. Damage caused by a subcontractor working under your supervision isn't automatically covered — they need to be added as an additional insured on your CGL. Contractors who regularly use subs should verify additional insured endorsements (ISO form CG 20 10) are confirmed before work begins — not after a claim surfaces.

Many contractors also need a specific endorsement to restore completed operations coverage that the base policy excludes. If your current program doesn't include it, that gap is worth closing before your next project wraps.

Manufacturing and Product-Based Businesses

Manufacturers face a compounding exclusion risk: the damage-to-your-product exclusion, the recall exclusion, and the pollution exclusion can all activate at once.

- A defective component that shuts down a buyer's production line → impaired property exclusion applies

- A product that triggers a recall → recall exclusion applies

- A manufacturing process that releases contaminants → pollution exclusion applies

The Consumer Product Safety Commission completed 333 product recalls in FY2024, and the product liability market underscores this exposure — Triple-I reports $4.53 billion in net product liability premiums written in 2024. Product recall insurance and product liability endorsements address these gaps. Soma places manufacturing programs through Chubb, Nationwide, and Markel, with product recall included in the program structure.

Hospitality: Restaurants, Bars, and Event Venues

The liquor liability exclusion is the defining gap for this sector. Most states have dram shop statutes allowing injured third parties — or their families — to sue the establishment that served the intoxicated person. Standard CGL excludes this exposure entirely for businesses in the alcohol trade.

Standalone liquor liability insurance (dram shop coverage) is the solution. Specialty markets — including Markel, Nationwide, and Liberty Mutual — cover mixed-use venues, late-night bars, and high-occupancy event spaces that standard brokers routinely decline. Soma places these risks directly with those markets.

Technology and Professional Services

Tech companies and professional service firms face a coverage gap on two fronts that standard CGL barely touches:

- Professional liability gap — CGL excludes claims arising from errors, omissions, or professional advice. Any client who claims your software caused financial harm or your consulting recommendation failed needs to be covered by E&O/tech professional liability insurance, not CGL.

- Cyber and data gap — electronic data is explicitly not tangible property under the CGL form, leaving data breaches, ransomware, and system failures entirely uninsured.

IRMI distinguishes tech E&O (protecting the technology provider) from cyber insurance (protecting consumers of technology services) — most tech firms need both. Soma coordinates CGL, tech E&O, and cyber liability into a single program through carriers including Chubb, Hiscox, Kinsale, and Liberty Mutual — so coverage gaps between policies don't become claims gaps.

How to Fill the Gaps Left by CGL Exclusions

Endorsements: The First Line of Defense

Some exclusions can be narrowed or bought back through policy endorsements — additions attached to the CGL itself. These are typically more cost-effective than separate policies.

Common CGL endorsements include:

- Liquor liability endorsement — for businesses with incidental alcohol exposure

- Hired and non-owned auto (HNOA) — for employees who use personal or rented vehicles for work

- Electronic data liability endorsement — provides limited coverage for data-related claims

- Additional insured endorsements (CG 20 10) — extends coverage to subcontractors, owners, or lessees

Standalone Policies for Fundamental Gaps

Some exclusions reflect risks too significant to address with an endorsement — they need their own policy:

| Gap | Policy That Fills It |

|---|---|

| Employee injuries | Workers' compensation |

| Vehicle liability | Commercial auto |

| Professional errors / advice | Professional liability (E&O) |

| Data breaches / ransomware | Cyber liability insurance |

| Pollution events | Pollution/environmental liability |

| Physical business assets | Commercial property insurance |

Umbrella/Excess Liability

A commercial umbrella policy doesn't remove CGL exclusions. What it does is extend the limits of your underlying liability policies. For businesses with catastrophic loss exposure, umbrella coverage adds substantial protection above the CGL limit without restructuring the base policy.

Work With a Broker Who Conducts a Gap Analysis

The most reliable way to identify uninsured exposures is a formal coverage gap review — comparing your current CGL exclusions against your actual operations and pinpointing where supplemental coverage is needed.

Soma works with businesses in construction, manufacturing, hospitality, technology, and other industries where multiple CGL exclusions can activate at once. As an independent brokerage, Soma places complex multi-policy programs across hundreds of carrier partners — including markets that handle accounts standard carriers decline.

Structuring the right program from the outset means you find out what isn't covered before a claim, not after.

Frequently Asked Questions

What is covered under commercial general liability insurance?

CGL covers third-party bodily injury, property damage, and personal and advertising injury (libel, slander, copyright infringement) arising from your premises, operations, products, and completed work. The policy pays defense costs, settlements, and judgments up to policy limits.

Can CGL exclusions be removed or overridden?

Some exclusions can be narrowed through endorsements — liquor liability, hired auto, and electronic data are common examples. Others, like intentional acts and employee injuries, are fundamental and require entirely separate policies to address.

Does CGL insurance cover subcontractors working for my business?

Damage caused by a subcontractor is generally excluded unless they are added as an additional insured on your CGL policy. Confirm this endorsement is in place before subcontractors begin any work on your behalf.

What is the difference between CGL and professional liability insurance?

CGL covers physical risks — bodily injury and property damage to third parties. Professional liability (E&O) covers financial harm caused by professional errors, omissions, or advice. Most businesses with client-facing operations need both policies to avoid significant coverage gaps.

Does a CGL policy cover employee injuries?

No. Employee injuries are explicitly excluded from CGL and covered under workers' compensation insurance, which is legally required for most employers across the U.S. (Texas is the primary exception, where it remains optional for most private employers).

What should I do if a claim is denied due to a CGL exclusion?

Review the specific exclusion language with a licensed insurance professional to understand why coverage was denied. Then determine whether a separate policy or endorsement should have been in place, and run a coverage gap review to avoid the same outcome on future claims.