That's exactly what public liability insurance exists to address.

Many U.S. business owners encounter the term "public liability insurance" when reviewing contracts, reading about competitors, or searching for coverage. The concept is straightforward, but the terminology creates confusion — because in the U.S., public liability protection is no longer sold as a standalone product. It's built into commercial general liability (CGL) insurance, and understanding that distinction could save you from buying inadequate coverage.

This guide covers what public liability insurance means, what it covers, who needs it, how much it costs, and how to get it.

TL;DR: Key Takeaways

- Public liability insurance protects businesses from third-party claims — bodily injury, property damage, and related legal costs

- In the U.S., this protection lives inside commercial general liability (CGL) policies, not as a standalone product

- It does not cover your own employees — workers' comp handles that

- It also does not cover your own business property — that's what commercial property insurance is for

- General liability costs average $42/month for many small businesses, though prices vary significantly by industry and risk level

- Most businesses that interact with clients or the public need this coverage, and many contracts require it

What Is Public Liability Insurance?

Public liability insurance protects a business from financial claims made by third parties (customers, vendors, delivery personnel, passersby) who suffer bodily injury or property damage connected to the business's operations.

The term has older roots. When ISO introduced the commercial general liability (CGL) policy in 1986, it replaced the older "comprehensive" general liability policy. Over time, "public liability" became a descriptor for the narrower, third-party-focused protection that the CGL policy now includes as a core component.

Today, U.S. insurers don't typically offer public liability insurance as a standalone product. The coverage is simply folded into a standard general liability policy.

Who qualifies as "the public" here? Current or potential customers, vendors, contractors visiting your site, neighbors, and anyone else outside your business. Your own employees are explicitly excluded and are covered under workers' compensation.

Two terms often confused with public liability:

- Premises liability — covers accidents specifically on your business property (a subset of general liability)

- Product liability — covers harm caused by products you sell (also typically included in a CGL policy)

Is Public Liability Insurance the Same as General Liability Insurance?

In casual conversation, the terms are often used interchangeably. Technically, they're not the same : public liability is a subset of general liability.

A standard CGL policy is broader. Beyond traditional public liability protections (bodily injury, third-party property damage), it also covers:

- Personal and advertising injury (libel, slander, copyright infringement)

- Completed operations (claims arising after work is finished)

- Medical payments to injured third parties

When a U.S. business owner searches for "public liability insurance" today, they'll almost always end up purchasing a CGL policy, which is actually better coverage than the older standalone product ever provided.

What Does Public Liability Insurance Cover?

A commercial general liability policy covers four main areas relevant to public liability claims:

Bodily Injury to Third Parties

The policy pays medical costs, rehabilitation expenses, and related legal damages if a third party is injured due to your business operations. Classic examples: a customer slipping on a wet floor, or a visitor tripping over an unsecured cable at your office.

Third-Party Property Damage

This covers accidental damage your business or employees cause to someone else's property. Common scenarios include:

- A contractor breaking a client's window during a renovation

- A cleaner spilling solution on a customer's laptop

- An employee damaging a vendor's equipment on-site

Coverage extends to real property (structures, land) and personal property (movable items).

Legal Defense Costs

The insurer has the right and duty to defend you against any covered lawsuit, paying attorney fees, court costs, and settlement payments even if the claim is ultimately unfounded. Defense costs alone can reach tens of thousands of dollars before a case is resolved, making this coverage valuable independent of any payout.

Completed Operations

Claims that arise after work is finished are also covered. If a structure shows a defect weeks after a contractor completes work, the general liability policy typically responds. For example, a plumber whose pipe fitting fails two months after installation would still have coverage for resulting water damage claims. Keep in mind that occurrence-based policies cover incidents that happen during the policy period, regardless of when the claim is filed.

What Public Liability Insurance Does NOT Cover

Understanding the exclusions is just as important as knowing what's covered:

| What's NOT covered | What covers it instead |

|---|---|

| Employee injuries on the job | Workers' compensation insurance |

| Damage to your own business property | Commercial property insurance or a BOP |

| Professional errors and bad advice | Professional liability / E&O insurance |

| Vehicle accidents while driving for work | Commercial auto insurance |

| Data breaches and cyber incidents | Cyber liability insurance |

| Intentional acts | Not insurable |

Note on workers' comp: in every U.S. state except Texas, workers' compensation is mandatory for nearly all employers with staff on payroll.

Public Liability vs. General Liability: Key Differences

Here's a practical side-by-side comparison:

| Coverage Area | Traditional Public Liability | Modern CGL Policy |

|---|---|---|

| Bodily injury to third parties | ✅ | ✅ |

| Third-party property damage | ✅ | ✅ |

| Personal and advertising injury | ❌ | ✅ |

| Product liability | ❌ | ✅ |

| Completed operations | ❌ | ✅ |

| Legal defense costs | Limited | ✅ Full |

A business with only traditional "public liability" coverage could be exposed to an advertising injury claim — a competitor alleging you used their trademarked images without permission, for example. For retail, e-commerce, and manufacturing businesses, that gap is real and costly.

The phrase "comprehensive general public liability insurance" simply describes a full CGL policy that bundles all liability protections — bodily injury, property damage, personal and advertising injury — into one package. It's a descriptor, not a distinct product.

A Business Owner's Policy (BOP) bundles general liability with commercial property insurance in one package — at a lower combined cost than purchasing each separately. For most small to mid-sized businesses, it's the most cost-efficient starting point, and the liability coverage inside a BOP is identical to a standalone general liability policy.

Who Needs Public Liability Insurance?

Any business that regularly interacts with customers, clients, vendors, or the general public should carry this coverage. Some industries carry substantially higher exposure than others.

High-exposure industries include:

- Retail stores and restaurants

- Hotels and hospitality venues

- Construction contractors

- Healthcare providers

- Salons and personal care services

- Landscapers and property maintenance

- Event-based businesses

According to The Hartford's 2025 small-business claims analysis, slip, fall, or customer injury claims averaged $45,000 each — a cost most businesses can't absorb out of pocket.

Contractual and regulatory triggers add another layer. Common requirements include:

- Commercial leases routinely require tenants to carry general liability coverage

- Federal contracts under FAR 28.307-2 require at least $500,000 per occurrence

- Florida contractor licenses require $100,000–$300,000 depending on license category

A Certificate of Insurance (COI) is typically required as proof before work begins.

Even lower-contact businesses benefit from coverage. Home-based businesses, freelancers, and online retailers still interact with the public when receiving deliveries, visiting client sites, or attending trade events — and standard homeowners insurance specifically excludes business-related liability claims.

Soma places coverage for businesses across these industries, including those that standard markets decline, and works directly with carriers to find policies that fit each operation's specific risk profile.

How Much Does Public Liability Insurance Cost?

Public liability protection in the US is covered under general liability (CGL) insurance, so pricing follows CGL benchmarks. Here's what small businesses typically pay across key industries:

| Business Type | Median Monthly Cost | Median Annual Cost |

|---|---|---|

| Healthcare professionals | $31/month | $376/year |

| Retail stores | $42/month | ~$500/year |

| Construction businesses | $82/month | $981/year |

| Average across industries | ~$42/month | ~$500/year |

For businesses with under $1M in annual revenue, NerdWallet reports general liability costs ranging from $700 to $3,000 per year depending on industry and coverage selected.

What Drives Your Premium

- Industry and risk level: construction and healthcare pay significantly more than consulting or retail

- Business size — revenue, payroll, and employee count all factor in

- Geographic location, since some states carry higher litigation exposure

- Coverage limits selected — higher limits mean higher premiums

- Prior claims history, which can increase your rate at renewal

Understanding Coverage Limits

About 85% of small businesses choose $1 million per occurrence / $2 million aggregate as their starting point, according to Insureon. Higher-risk operations, government contracts, or businesses with larger revenue typically need higher limits — and a commercial umbrella policy can extend coverage beyond standard CGL limits as operations grow.

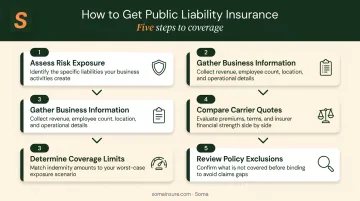

How to Get Public Liability Insurance

Getting covered doesn't require weeks of back-and-forth. Here's a practical approach:

- Assess your risk exposure — consider your industry, the number of people who visit or interact with your business, and any contractual requirements you're subject to

- Gather basic business information — industry classification, annual revenue, number of employees, business location, and any prior claims history

- Determine your coverage limits — start at $1 million per occurrence / $2 million aggregate and adjust upward based on contract requirements or risk level

- Compare quotes from multiple carriers — don't accept the first offer; premiums for the same coverage can vary significantly between insurers

- Review the policy exclusions — confirm what's not covered so you can identify any gaps needing separate policies

These steps are straightforward in theory, but sourcing the right carrier can be the hardest part — especially in complex or hard-to-insure industries where standard markets frequently decline coverage. Working with a specialized brokerage like Soma streamlines that process. One application reaches hundreds of carrier partners, including Chubb, Markel, Liberty Mutual, Kinsale, and Nationwide, so you get competitive quotes without chasing multiple brokers.

Frequently Asked Questions

How much is public liability and property damage insurance?

Since both coverages are components of a general liability policy, pricing depends on your industry, business size, location, and limits. Most small businesses pay between $31 and $82 per month. A BOP — which bundles general liability with property coverage — is often the more affordable combined option.

Is public liability and property damage insurance the same as general liability insurance?

In the U.S., yes — public liability and property damage are core components of a commercial general liability (CGL) policy, not separate products. CGL also adds personal and advertising injury coverage, making it broader than traditional public liability alone.

What is comprehensive general public liability insurance?

This phrase describes a full CGL policy that covers bodily injury, third-party property damage, and personal/advertising injury claims in one package. The term isn't a distinct product category — just a descriptor for a complete, well-structured general liability policy.

Do I need public liability insurance if I work from home?

Yes, if clients visit your home, you work at client locations, or your business receives deliveries. Standard homeowners insurance excludes business-related liability claims, leaving you exposed without a separate policy.

What are typical coverage limits for public liability insurance?

The standard starting point is $1 million per occurrence and $2 million aggregate. Businesses in higher-risk industries or those holding government or commercial contracts may need higher limits — a commercial umbrella policy can extend coverage beyond standard limits when required.

What industries are required to have public liability insurance?

No federal law mandates it universally, but construction, healthcare, food service, and businesses with commercial leases or government contracts commonly face contractual or state-level requirements. Most clients will request a Certificate of Insurance (COI) before work begins.