Here's what catches many business owners off guard: these two events require two different types of insurance coverage. The break-in is a property claim. The slip-and-fall is a liability claim. Assuming one policy handles both is one of the most expensive mistakes a business can make.

A 2025 Hiscox report found that 74% of small-business owners misunderstood what general liability covers — with many expecting it to cover fire or flood damage to their own property. That's a dangerous knowledge gap.

This guide breaks down exactly how commercial property and liability insurance differ, what each covers, and how to figure out what your business actually needs.

Key Takeaways

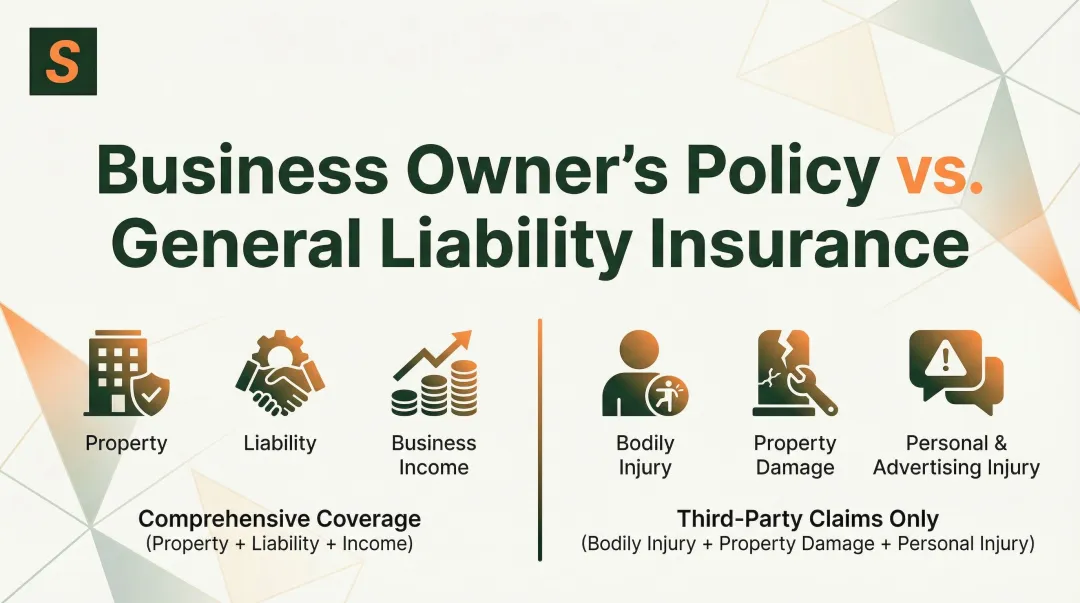

- Commercial property insurance protects your physical assets (building, equipment, inventory) from damage, theft, or destruction.

- Commercial liability insurance protects your business from third-party claims of bodily injury, property damage, or advertising harm — including legal costs and settlements.

- The core distinction: property is first-party coverage (pays you), liability is third-party coverage (pays others on your behalf).

- Most businesses need both; a Business Owner's Policy (BOP) bundles them together at a lower combined cost.

- Neither policy covers the other's gaps — knowing your exclusions is just as important as knowing your coverage.

Commercial Property vs. Liability Insurance: At a Glance

| Commercial Property Insurance | Commercial Liability Insurance | |

|---|---|---|

| What it protects | Your physical business assets | Your business against third-party claims |

| Who it pays | You (the policyholder) | The claimant + your legal defense |

| Common covered events | Fire, theft, vandalism, certain weather | Bodily injury, property damage, advertising harm |

| Triggered by | A physical loss event | A claim or lawsuit from a third party |

| Who needs it most | Businesses with buildings, equipment, inventory | Any business that interacts with the public |

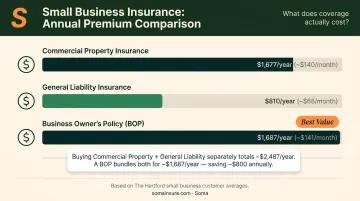

| Typical annual cost* | ~$1,677/year | ~$810/year |

Based on The Hartford customer averages (2023).

What Is Commercial Property Insurance?

Commercial property insurance covers physical business assets (owned or leased buildings, furniture, equipment, computers, inventory, and supplies) against loss or damage from covered perils.

Named Perils vs. Open Perils

Coverage breadth depends on the form you purchase:

- Named perils (basic/broad form): Only covers specific listed events like fire, lightning, windstorm, and hail. If the cause isn't named, it's not covered.

- Open perils (special form): Covers all causes of loss except those specifically excluded. This is the broadest and most common choice for businesses with significant assets.

A named-perils policy that doesn't list "water damage from a burst pipe" leaves you exposed to a loss that an open-perils policy would cover automatically — and that gap shows up at the worst possible time: during a claim.

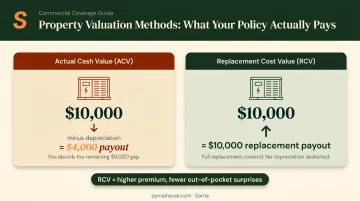

ACV vs. Replacement Cost: The Valuation Gap

Claim time is when valuation method stops being abstract. Here's what each approach actually means:

- Actual Cash Value (ACV): Replacement cost minus depreciation. A five-year-old piece of equipment worth $10,000 new might only pay out $4,000 under ACV.

- Replacement Cost Value (RCV): What it costs to replace the damaged property with a new equivalent — no depreciation deducted.

For most businesses, RCV is worth the higher premium. After a fire or theft, rebuilding with ACV payouts often means coming out of pocket for the depreciation gap.

Common Coverage Extensions

Endorsements extend standard property policies to cover specific exposures:

- Business interruption: Replaces lost income if operations halt after a covered event. Payroll, rent, and fixed costs keep running even when your business can't.

- Inland marine: Covers property in transit or temporarily off-site (critical for contractors with tools on job sites or manufacturers shipping goods).

- Equipment breakdown: Covers mechanical or electrical failure of equipment, separate from physical damage perils.

Despite its value, only 30–40% of small-business owners carry business interruption coverage, according to NAIC — a significant gap given how quickly fixed costs pile up after an unexpected shutdown.

What Commercial Property Insurance Does NOT Cover

These exclusions catch businesses off guard:

- Flood and earthquake (require separate policies)

- General wear and tear or gradual deterioration

- Vehicle damage (covered under commercial auto)

- Employee theft (property policies exclude employee dishonesty without a crime endorsement)

- Property in transit without an inland marine endorsement

What Is Commercial Liability Insurance?

Commercial general liability (CGL) insurance protects businesses from third-party claims — meaning people outside the business, such as customers, vendors, and bystanders. It covers bodily injury, property damage, personal injury (libel/slander), and advertising injury (copyright infringement). Employees are not covered under CGL; that's what workers' compensation handles.

The Three Core Coverage Sections of a CGL Policy

Premises and operations liability covers injury or damage at your business location or during ongoing work. A customer slipping on a wet restaurant floor is the textbook claim — The Hartford puts the average small-business slip-and-fall cost at $45,000.

Products and completed operations liability covers claims arising from your products or finished work after the fact — a manufacturer whose product injures a consumer, or a contractor whose completed renovation causes water damage.

Personal and advertising injury covers libel, slander, wrongful eviction, privacy violations, and copyright infringement in marketing materials. Reputational harm claims average $35,000 for small businesses, per The Hartford.

Beyond CGL: The Broader Liability Ecosystem

General liability is the foundation, but many businesses need additional coverage layers:

- Professional liability/E&O: For service-based businesses — tech consultants, financial advisors, healthcare providers — covering claims of negligence or failure to perform professional services

- Cyber liability: For any business handling customer data, covering breaches, ransomware, notification costs, and regulatory defense

- Employment practices liability (EPLI): Covers wrongful termination, discrimination, and harassment claims from employees

- Commercial umbrella: Extends limits beyond your primary policies for catastrophic claims

For complex industries, these coverages work together as a single strategy — not separate purchases. A healthcare provider needs facility liability, professional liability, and cyber coverage aligned. Gaps between policies create exposure that no single policy addresses on its own.

What Commercial Liability Insurance Does NOT Cover

- Damage to your own property

- Employee injuries (workers' compensation)

- Intentional or criminal acts

- Auto accidents involving business vehicles (commercial auto)

- Professional errors without a separate E&O policy

Understanding these exclusions is part of what makes the property vs. liability distinction so important — each policy type fills a gap the other leaves open. And the stakes are real: the U.S. Chamber Institute for Legal Reform found that small businesses shouldered $160 billion in tort costs in 2021 — 48% of total U.S. commercial liability tort costs — despite generating only 20% of revenue.

Key Differences That Matter for Your Business

First-Party vs. Third-Party: The Fundamental Split

This single distinction explains most of the confusion between the two policies:

- Property insurance pays YOU when your business suffers a loss

- Liability insurance pays on your behalf when your business causes a loss to someone else

Same event, two different claims: a fire breaks out in a café. The fire damages the building and equipment — that's a property claim. A customer burns their hand trying to escape — that's a liability claim. One event, two separate policies responding.

What Triggers Each Policy

| Commercial Property | Commercial Liability | |

|---|---|---|

| Trigger | Physical loss event (fire, theft, storm) | Third-party claim or lawsuit |

| When reported | Typically immediate, at time of loss | Can surface months or years after the event |

| Who initiates | The business owner | A third party (customer, vendor, bystander) |

The claims timeline difference matters operationally. A fire is reported the day it happens. A products liability claim for an injury caused by something you sold two years ago can arrive long after you've forgotten the transaction.

What Each Policy Costs

Premium drivers differ between the two coverage types:

Property premium factors:

- Value and replacement cost of insured assets

- Location (catastrophe exposure, crime rates)

- Building construction type and age

- Covered perils selected

Liability premium factors:

- Industry risk classification

- Annual revenue and number of employees

- Claims history

- Coverage limits selected

For context: The Hartford's small business data shows customers paid an average of $1,677/year (~$140/month) for commercial property insurance and $810/year (~$68/month) for general liability. A Business Owner's Policy bundling both averaged $1,687/year (~$141/month), often less than purchasing the two separately.

The Exclusions Gap

Neither policy covers the other's territory. Property insurance won't pay a lawsuit judgment. Liability insurance won't replace your damaged equipment. This isn't a flaw — it's by design. The gap is the entire reason most businesses need both.

Do You Need One, the Other, or Both?

Situational Guidance

| Your situation | Coverage you need |

|---|---|

| You own or lease a physical location | Commercial property |

| You have equipment, inventory, or furnishings at risk | Commercial property |

| Customers, vendors, or the public visit your business | General liability |

| You sell products or provide services | General liability |

| You have a commercial lease | General liability (most leases require it) |

| You pull construction permits | General liability (many jurisdictions mandate it) |

| You fit all of the above | Both |

Most businesses fit every row of that table — which is exactly why bundled options exist.

The BOP Option for Small Businesses

A Business Owner's Policy (BOP) bundles commercial property and general liability into a single policy, typically at a lower combined cost than buying each standalone. The III notes BOPs are generally designed for businesses with fewer than 100 employees and under approximately $5 million in revenue.

What a standard BOP does NOT include:

- Commercial auto

- Workers' compensation

- Professional liability

A BOP works well for lower-risk small businesses — a retail shop, a small office, a service company with a physical location. For businesses with more complex exposures, it often falls short.

When a BOP Isn't Enough

Standard BOPs may be unavailable or inadequate for high-risk or complex industries. Restaurants, construction firms, security agencies, trucking operations, and healthcare facilities often face exposures that exceed BOP limits or fall outside BOP eligibility entirely.

For these businesses, industry-specific program policies — not cookie-cutter BOP packages — provide the right coverage architecture. A security guard agency, for example, needs general liability plus assault and battery coverage, professional liability, commercial auto for patrol vehicles, and crime coverage. No standard BOP addresses that exposure stack.

Soma works with hundreds of carrier partners (including Chubb, Markel, Kinsale, Liberty Mutual, and Nationwide) to place exactly these kinds of complex, multi-coverage programs.

For businesses in construction, manufacturing, hospitality, healthcare, and other hard-to-insure categories, Soma's Risk Management Team analyzes each operation's specific exposures and builds coverage that fits — often processed through a single application.

Frequently Asked Questions

What is the difference between commercial property insurance and general liability insurance?

Commercial property insurance covers damage to your own physical assets — building, equipment, inventory. General liability covers claims made by third parties for injuries or damages your business causes to them. One is first-party (pays you); the other is third-party (pays others on your behalf).

Does my business need both commercial property and liability insurance?

Most businesses need both. Property insurance protects your assets after a fire, theft, or storm. Liability insurance protects against lawsuits from customers or vendors. A BOP bundles both affordably, though complex or high-risk businesses typically need standalone policies with broader limits.

What does commercial property insurance not cover?

Common exclusions include floods, earthquakes, employee theft (without a crime endorsement), normal wear and tear, vehicle damage, and property in transit. Flood and earthquake coverage require separate policies; inland marine covers property off-site or in transit.

Can liability insurance cover damage to my own business property?

No. General liability only covers third-party claims. Damage to your own property requires a commercial property policy — or a BOP that includes property coverage.

What is a Business Owner's Policy (BOP) and does it replace both policies?

A BOP bundles general liability and commercial property into one package, often at a lower combined cost. It's designed for small, lower-risk businesses with under 100 employees and under $5 million in annual revenue. High-risk or complex businesses typically need standalone or program policies instead.

How are commercial property and liability insurance premiums calculated?

Property premiums depend on asset value, location, construction type, and selected perils. Liability premiums are based on industry classification, annual revenue, employee count, and claims history. Both can be adjusted with different coverage limits and deductibles to fit your budget and risk tolerance.