Introduction

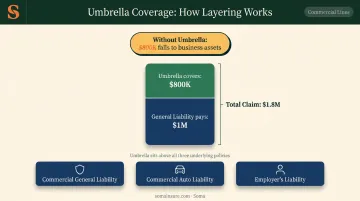

A customer slips on a wet floor in your retail store, suffers a serious injury, and sues for $1.8 million. Your general liability policy covers up to $1 million per occurrence. Where does the remaining $800,000 come from?

If you don't have umbrella coverage, the answer is your business's bank account.

Many business owners assume their GL policy is enough — and for routine claims, it usually is. But verdict severity is climbing fast. Marsh data shows average nuclear verdicts rose from $64 million in 2015 to $214 million in 2019, and Verisk found plaintiff win rates increased from 53% to 64% between 2012 and 2019. Standard policy limits don't always keep pace.

That gap between what your GL covers and what a serious claim costs is exactly where businesses get hurt. This guide breaks down how GL and umbrella insurance differ, which businesses need both, and how to set coverage limits that reflect your actual risk.

TL;DR

- General liability is a standalone primary policy — it pays first on covered third-party claims.

- Umbrella insurance is secondary — it only activates after underlying policy limits are exhausted.

- Umbrella policies extend limits across multiple underlying policies (GL, auto, employer's liability); excess liability only stacks onto one.

- You can have GL without umbrella, but umbrella cannot exist without an underlying policy.

- GL is the baseline for most businesses; high-risk industries — construction, security, trucking — typically need both.

General Liability vs. Umbrella Insurance: Quick Comparison

| Feature | General Liability | Commercial Umbrella |

|---|---|---|

| Policy Type | Primary (standalone) | Secondary (requires underlying policies) |

| What It Covers | Third-party bodily injury, property damage, advertising injury | Excess limits above GL, commercial auto, employer's liability |

| Typical Limits | $1M per occurrence / $2M aggregate | $1M–$5M (small business); up to $15M available |

| Standalone Purchase | Yes | No |

| Who Needs It | Nearly all businesses | High-risk, high-asset, or contractually required businesses |

| Approximate Cost | ~$45/month (small business average) | ~$40/month per $1M of additional coverage |

Cost data sourced from Insureon's general liability and umbrella cost benchmarks. Actual premiums vary by industry, revenue, claims history, and location.

Umbrella and excess liability coverage are often confused, but they work differently. Excess liability only adds limits on top of one specific policy and mirrors that policy's terms exactly. A commercial umbrella can sit above multiple underlying policies simultaneously and may fill certain gaps those policies don't address — making it the stronger choice for businesses managing exposure across several coverage lines.

What Is General Liability Insurance?

Commercial general liability (CGL) insurance is the foundational policy most businesses purchase first. It protects against third-party claims that arise from everyday operations — the injuries, property damage, and advertising disputes that any customer-facing or client-serving business can face.

The Three Core Coverage Areas

- Third-party bodily injury — A customer slips and falls in your store. GL covers their medical bills and any resulting lawsuit.

- Third-party property damage — A technician accidentally damages a client's equipment on-site. GL covers repair or replacement costs.

- Personal and advertising injury — Covers copyright infringement, libel, and slander claims — for example, if a competitor alleges you copied their marketing material.

Many GL policies also include product liability, covering injuries or damages caused by products your business manufactures, sells, or distributes. For smaller operations, GL can also be bundled into a Business Owner's Policy (BOP) alongside commercial property coverage — a cost-effective way to consolidate core coverage.

Understanding Policy Limits

GL policies are structured around two key limits:

- Per-occurrence limit — the maximum paid for a single claim

- General aggregate limit — the maximum paid across all claims in a policy period

The most common structure for small businesses is $1M per occurrence / $2M aggregate. Higher-risk industries or businesses with larger contracts often opt for $2M/$4M.

The right limits depend on your industry, revenue, and contractual requirements. Commercial leases, for example, typically require at least $1M/$2M before a tenant can take occupancy.

Who Needs GL

Most businesses need GL coverage — specifically any operation that:

- Has physical premises open to customers or vendors

- Works at client sites (contractors, technicians, consultants)

- Signs vendor, client, or lease agreements requiring proof of coverage

- Creates, distributes, or sells products

Industries where GL is especially critical include construction, retail, hospitality, healthcare, and manufacturing.

What Is Commercial Umbrella Insurance?

Commercial umbrella insurance is a secondary liability policy. It doesn't replace your GL or other primary policies — it sits above them and activates only after the underlying limits are fully exhausted. For businesses facing large verdicts or multi-party claims, that layered structure is what prevents a single lawsuit from wiping out business assets.

How the Layering Mechanism Works

Here's a concrete example:

- Your GL policy has a $1M per-occurrence limit

- A lawsuit from a serious slip-and-fall settles for $1.8M

- GL pays the first $1M

- Your $800K umbrella covers the remaining balance

Without umbrella, that $800,000 gap comes out of your business assets directly. And umbrella doesn't just protect one policy — it applies across multiple underlying policies simultaneously. Common underlying policies include:

- Commercial general liability

- Commercial auto liability

- Employer's liability (from a workers' compensation policy)

This is the key distinction from excess liability. Excess liability extends just one underlying policy's limits and mirrors its terms exactly. Umbrella covers multiple policies at once — and can sometimes respond to gaps not addressed by any underlying policy, though a self-insured retention (SIR) typically applies to those uncovered gaps.

What Umbrella Does NOT Cover

This is where many businesses get caught off guard. Umbrella does not extend to:

- Professional errors or negligence — requires separate E&O/professional liability coverage

- Employee injuries — covered by workers' compensation, not umbrella

- Intentional acts — excluded across virtually all liability policies

- Commercial property damage — umbrella doesn't cover your own equipment or premises

- Cyber incidents — requires dedicated cyber liability coverage

Use Cases for Commercial Umbrella

Umbrella makes the most sense when one or more of these risk signals apply to your business:

- High volume of public foot traffic (retail, hospitality, events)

- Employees who drive company or personal vehicles for work

- Handling of expensive third-party equipment or property

- Contracts requiring limits above standard GL (construction projects, government bids)

- Business assets that significantly exceed your current GL limit

For construction contractors, umbrella coverage is often non-negotiable. UNLV's contract guidelines require a $10M excess or umbrella policy for projects over $5 million. NY OGS guidelines reference umbrella requirements up to $5M for certain public contracts. If you're bidding on institutional or government work, the coverage isn't discretionary — it's written into the contract terms.

General Liability vs. Umbrella Insurance: Key Differences That Matter

Difference 1 — Role in the Coverage Stack

GL is your first line of defense. Umbrella is what protects you when the first line isn't enough.

GL pays on covered claims up to its limits. Once those limits are exhausted — by one large claim or by multiple smaller claims depleting the aggregate — umbrella activates.

Umbrella coverage requires at least one active underlying policy to function. Without a current GL, commercial auto, or employer's liability policy in force, umbrella cannot be purchased or triggered.

Difference 2 — Scope of Coverage

GL covers specific named perils: bodily injury, property damage, and personal/advertising injury — fixed categories that cover most everyday exposures but don't expand beyond them.

Key GL perils at a glance:

- Bodily injury to third parties

- Property damage caused by your operations

- Personal and advertising injury (libel, slander, copyright claims)

Umbrella extends limits across multiple policy types at once. If a single accident involves both a GL claim and a commercial auto claim, umbrella can apply to both — rather than requiring separate excess policies for each line.

Difference 3 — Limits and Cost Efficiency

GL is structured around fixed per-occurrence and aggregate limits. Umbrella adds coverage in large increments — typically $1M at a time.

The cost math is straightforward: GL for a contractor averages around $82/month for a $1M/$2M policy. Adding $1M in umbrella coverage runs approximately $40/month. That's meaningful additional protection for roughly half the per-million rate of the primary policy — making umbrella one of the more cost-efficient ways to increase total liability coverage.

Difference 4 — Purchase Requirements

That cost efficiency comes with one structural requirement: GL can be purchased as a standalone policy, but umbrella cannot. It requires at least one active underlying policy before it can be written.

This also means umbrella is inherently an integrated risk management tool. Rather than buying separate excess liability policies for each coverage line — one stacked above GL, another above commercial auto — a single umbrella policy covers the entire tower simultaneously.

Do You Need Both General Liability and Umbrella Insurance?

Most small businesses need GL as a starting point. Whether you need umbrella depends on your risk profile.

You likely need umbrella if:

- Your industry carries high-severity liability exposure (construction, trucking, healthcare, hospitality)

- You have significant business assets that a large judgment could threaten

- Clients, landlords, or contracts require limits above standard GL

- Employees drive as part of their job

- You regularly interact with large volumes of the public

A scenario worth considering: A construction subcontractor with a $1.5M GL policy has an employee who causes a multi-vehicle accident resulting in $3M in total damages. GL pays the first $1.5M. Without umbrella, the remaining $1.5M falls to the business — which can mean asset liquidation or bankruptcy.

With a $2M umbrella policy in place, the claim is fully covered. The business survives.

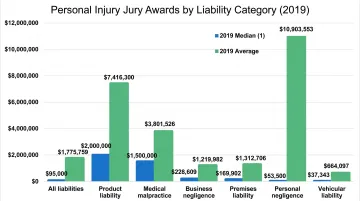

That scenario plays out more often than most owners expect. Personal injury jury awards averaged nearly $2.5 million across all liability categories in 2020, with product liability averaging over $7 million — figures that standard GL limits can't always absorb on their own.

Determining the right combination of GL and umbrella coverage requires understanding both your exposure and your contracts. Soma's specialists work across these industries daily and can assess your risk profile, placing both policies through a single application with carrier partners including Chubb, Markel, and Liberty Mutual.

Conclusion

GL and umbrella aren't competing options. They're complementary layers in a coverage stack — one handles everyday claims, the other handles catastrophic ones.

The right question isn't "which one do I need?" It's "how much total liability protection does my business actually require?"

Start by reviewing your current GL limits against three factors:

- Your business assets — what's actually at risk if a large judgment lands against you

- Your industry's claim severity — some sectors see routine seven-figure suits; others rarely do

- Contractual requirements — clients and landlords often mandate specific limits you may not currently carry

If any of those reveal a gap your GL can't close, umbrella coverage deserves a serious look. A commercial insurance broker who works with both policy types can run that comparison and structure the two layers so they work together — not against each other.

Frequently Asked Questions

Is forming an LLC better protection than buying an umbrella policy for my business?

An LLC shields your personal assets from business liabilities — it doesn't create insurance proceeds for the business itself. If your business owes a $2M judgment and only has $1M in GL coverage, the LLC doesn't cover the gap. Umbrella insurance does. Use both together.

Can you buy umbrella insurance without general liability insurance?

No. Insurers require at least one active underlying policy — typically GL, commercial auto, or employer's liability — before they'll write umbrella coverage. It's a secondary policy by definition and cannot stand alone.

How much does commercial umbrella insurance cost?

Insureon benchmarks umbrella at roughly $40/month per $1M of additional coverage, or about $480/year per $1M. Most small businesses purchase $1M–$5M in umbrella limits. Final pricing varies by industry, business size, underlying limits, and claims history — so quotes differ significantly.

What does general liability insurance NOT cover?

Key GL exclusions include: professional errors or negligence (requires E&O), employee injuries (workers' compensation), intentional acts, commercial vehicle accidents (commercial auto policy), and cyber incidents. Each of these requires its own dedicated coverage.

Does umbrella insurance cover professional liability claims?

Standard commercial umbrella policies do not cover professional liability or E&O claims — umbrella extends GL, commercial auto, and employer's liability only. Businesses providing professional advice or services need a separate E&O policy.

How much umbrella insurance does a small business typically need?

A common starting guideline is to carry umbrella limits at least equal to the total value of your business assets. In practice, industry risk level and contract requirements often drive the number higher — construction and government contracts can require $5M–$10M.