Introduction

The US Tech E&O insurance market in 2026 presents a clear tension: incident frequency is climbing sharply while pricing remains soft. That combination rarely lasts.

Aon's March 2026 market report documented a 38% increase in reported US cyber and Tech E&O incidents in 2025 versus 2024 — yet average pricing stayed essentially flat, with all-layer rates declining 4–5% across the year. More than 90 insurers competed for placements, keeping capacity abundant and buyers firmly in control.

Most tech companies aren't taking advantage of it. Many are underinsured — operating under general liability policies that don't cover professional failures, or holding cyber policies that leave third-party service claims exposed.

The coverage gaps are often invisible until a claim surfaces. AI tools, SaaS products, and managed services each carry distinct Tech E&O exposures that standard policies don't address.

This article covers what Tech E&O insurance actually protects, what the US market looks like heading into 2026, the risk forces driving long-term growth, current pricing conditions, and how tech companies should structure coverage while soft-market conditions still hold.

TLDR

- Reported US cyber and Tech E&O incidents rose 38% in 2025, even as pricing declined 4–5%

- Average global ransomware claims jumped from $374,400 to $713,200 — a 90% increase in a single year

- Over 90 insurers participated in 2025 placements, sustaining strong capacity and keeping rates favorable for buyers heading into 2026

- AI development and deployment is creating a distinct liability category that most standard Tech E&O policies weren't written to cover

- SaaS, fintech, healthtech, and MSP companies have a narrow window to lock in favorable terms before rising claims push pricing back up

What Is Tech E&O Insurance and What Does It Cover?

Technology Errors & Omissions insurance is a specialty professional liability product. It protects tech companies when their products or services fail to perform as intended and a client suffers financial harm — covering legal defense costs and any resulting damages.

General liability covers bodily injury and property damage. Cyber liability covers breach response costs and privacy events. Tech E&O fills a different gap: the professional and contractual failures that happen when software breaks, deadlines are missed, or services don't deliver what was promised.

Risks and Claim Types Typically Covered

Core covered scenarios include:

- Product malfunction or coding errors that cause measurable financial loss for a client

- Failure to deliver on contractual obligations or project timelines

- IP infringement — copyright or patent disputes tied to your product or codebase

- Negligent professional services — consulting, implementation, or integration failures

- Vicarious liability from subcontractors working on your behalf

Consider how quickly a claim can materialize: a software integration vendor deploys a data migration tool that corrupts a pharmaceutical client's production database. The client faces regulatory fines and lost revenue. The vendor is sued. Without Tech E&O, that lawsuit and any resulting judgment lands entirely on the vendor. With coverage, legal defense and damages fall within policy limits.

What Tech E&O Does NOT Cover

- Bodily injury or physical property damage (general liability territory)

- Intentional wrongdoing or fraud

- First-party breach response costs — notification, forensics, credit monitoring — which require a separate cyber policy

A single incident — a vendor breach that exposes client data and disrupts a software service — can trigger both cyber and Tech E&O claims at the same time. Carriers including Chubb, Hiscox, and others in Soma's carrier network offer bundled Tech E&O + cyber products that cover both under one policy, removing the gap between coverage lines.

US Tech E&O Insurance Market Size in 2026

No authoritative public source separately reports US Tech E&O-only premiums. The closest regulatory benchmark is the broader US cyber insurance market, which NAIC measured at $9.14 billion in direct written premiums in 2024 — though that figure covers cyber insurance broadly and does not isolate Tech E&O as a distinct line.

For global context, Congruence Market Insights estimated the global Technology E&O market at $574 million in 2025, projecting growth to $928.8 million by 2033 at a 6.2% CAGR. That's a global figure, not US-specific — but at that growth rate, the US market (historically accounting for roughly 40–50% of global specialty insurance premiums) is on pace to represent a meaningfully larger slice of Tech E&O spend by 2026.

What Market Behavior Actually Tells Us

The strongest current evidence comes from Aon's 2026 report:

- 38% increase in reported US cyber and Tech E&O incidents in 2025 vs. 2024

- More than 90 insurers participated in cyber and Tech E&O risk placements in 2025

- Approximately 19% of US cyber liability buyers expanded their coverage limits in 2025

Those participation and limit-expansion numbers reflect a market responding to real claims pressure. Behind that pressure: a growing tech sector. CompTIA's 2025 State of the Tech Workforce report shows the US tech workforce grew 1.2% in 2024, with SaaS, AI, cloud, and managed services firms making up a rising share of the insured market. More tech companies means more professional liability exposure — and more demand for coverage.

Who's Driving Demand

The fastest-growing buyer segments include:

- SaaS and cloud platforms with enterprise client contracts requiring minimum coverage limits

- AI/ML developers facing a new category of professional liability claims

- Fintech firms operating under heightened regulatory scrutiny

- Managed service providers (MSPs) with deep client-system access

- Healthtech companies handling sensitive data under HIPAA-adjacent risk

Key Risk Drivers Fueling Market Growth in 2026

Ransomware Severity

Global ransomware incidents dropped 31% year-over-year in Q4 2025 — but claim costs nearly doubled. The average global ransomware claim rose from $374,400 in 2024 to $713,200 in 2025, according to Aon. Underwriters are watching severity, not frequency.

For context, Sophos reported average recovery costs of $1.5 million per incident in its 2025 State of Ransomware survey. That kind of loss development is why underwriters remain selective about controls even while pricing stays soft.

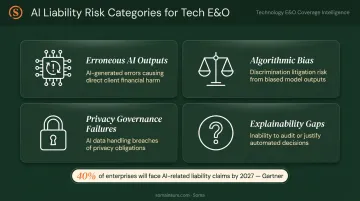

AI Liability

AI is creating a liability category that most standard Tech E&O policies weren't written to address. Companies deploying AI tools face claims tied to:

- Erroneous AI outputs that cause client financial harm

- Algorithmic bias — Workday has been in active litigation since 2024 over claims that its AI hiring tools facilitated discrimination at customer companies

- Privacy governance failures in AI data handling

- Lack of explainability in high-stakes automated decisions

Gartner forecast in February 2025 that by 2027, more than 40% of AI-related data breaches will arise from improper cross-border use of generative AI. Regulatory pressure is building alongside litigation risk — Colorado's SB24-205 requires developers and deployers of high-risk AI systems to use reasonable care against algorithmic discrimination, effective in 2026.

Privacy Regulation Expansion

The US state privacy landscape has transformed in three years. Indiana, Kentucky, and Rhode Island laws took effect January 1, 2026, joining 14+ other states that have enacted comprehensive privacy statutes since Virginia's CDPA in 2023. Each new law creates another liability vector for technology providers handling consumer data.

The financial exposure is concrete. Blackbaud settled a multistate data breach investigation for $49.5 million across 49 states and DC in October 2023. Motorola Solutions settled BIPA-related facial recognition claims for a reported $47.5 million.

Supply Chain Cyber Risk

Aon's 2026 report found that two-thirds of large organizations name third-party and supplier vulnerabilities as their most significant cyber exposure. Nearly the same share experienced an actual third-party breach in the past year. Verizon's 2026 DBIR reported third-party involvement in 30% of breaches, up from 15% the prior year.

For software vendors and MSPs, that's a direct Tech E&O exposure. A client breach that traces back to your code or access credentials puts your professional liability coverage in play immediately.

Supporting Sub-Drivers

Three additional factors are shaping demand:

- Geopolitical risk — state-sponsored attacks targeting US tech infrastructure continue to escalate, with CrowdStrike's 2025 Global Threat Report documenting the trend

- SEC and CISA disclosure obligations — public companies must now disclose material cyber incidents within four business days on Form 8-K, raising governance expectations for technology vendors

- Enterprise contract requirements — the University of Nevada's public technology contract standards, for example, require a minimum $5M per-occurrence Tech E&O limit for contracts under $1M, a clear sign that procurement requirements are pushing coverage minimums higher

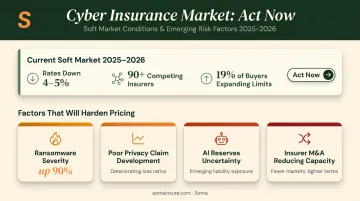

2026 Pricing and Market Conditions: A Buyer's Window

Current pricing data tells a consistent story across multiple sources:

| Source | 2025 Tech E&O / Cyber Pricing |

|---|---|

| Aon | Flat to -4% quarterly; all-layer down 4–5% |

| WTW 2026 Outlook | -5% to +5% range |

| Marsh Global Index | Cyber rates down ~5% |

| Gallagher | Flexible pricing, stabilizing after volatility |

All four major brokers are signaling the same thing: soft conditions. More than 90 insurers competed for placements in 2025, keeping capacity abundant and putting buyers in control of terms.

Why This Won't Last Indefinitely

Several factors are building that will eventually firm pricing:

- Ransomware severity nearly doubled year-over-year — rising losses will eventually push rates up

- Poor prior-year development on privacy claims is emerging

- Insurers are pricing AI-driven exposures without meaningful claims history to guide reserves — a gap that tends to correct sharply

- Insurer M&A activity could reduce the number of competing carriers

Buyers who act now can lock in favorable terms, broader coverage definitions, and competitive pricing before the market corrects. Approximately 19% of US cyber liability buyers expanded their limits in 2025, according to Aon — a clear signal that informed buyers are using the soft market strategically rather than simply reducing premium spend.

The window is open. The next section breaks down what coverage structure actually makes sense in this environment.

What Underwriters Look for When Pricing Tech E&O

Underwriters evaluate Tech E&O submissions across several dimensions:

Primary pricing factors:

- Company revenue and employee count

- Type of technology offered — proven SaaS products vs. emerging AI tools

- Client contract sizes and contractual liability caps

- Claims and litigation history

- Geographic footprint (multi-state or international operations increase legal complexity)

Growing emphasis areas:

- Incident response plan documentation

- Vendor and subcontractor management practices

- Software testing and QA protocols

- For AI companies specifically: governance frameworks, bias testing procedures, and compliance documentation

That last category has shifted from optional to expected. Colorado's AI law and FTC enforcement actions have moved AI governance from a theoretical concern to something underwriters now ask about directly. A company that can show structured oversight — documented policies, testing protocols, and clear accountability — typically qualifies for broader coverage at better rates than one that can't.

Companies with strong internal controls and contractual risk management practices (limiting liability exposure in client agreements, for example) consistently secure better pricing and broader coverage terms than comparable businesses without them.

How to Get the Right Tech E&O Coverage for Your Business

A straightforward process for approaching coverage in 2026:

- Inventory your products and services — identify every technology offering, including AI tools, APIs, and third-party integrations, that could generate a professional liability claim

- Review your contracts — check for minimum insurance requirements in enterprise agreements; $5M per-occurrence limits are common in public-sector and large-enterprise contracts

- Determine appropriate limits — base limits on your largest client contract value, not on what seems affordable

- Consider bundling — a combined Tech E&O + cyber policy eliminates coverage gaps and simplifies claims handling when a single incident triggers both policies

- Work with a specialized broker — Tech E&O policy wording varies significantly across carriers; AI exclusions, retroactive dates, and claims-made structures require expertise to evaluate

Soma places Tech E&O coverage for SaaS companies, software developers, IT consultants, and technology product firms through carriers including Chubb, Markel, Kinsale, and Liberty Mutual. Submitting one application across multiple carriers means faster quotes and side-by-side comparisons — without the back-and-forth of managing each carrier separately.

Frequently Asked Questions

How big is the US Tech E&O insurance market?

No authoritative public source separately reports US Tech E&O-only premiums. The NAIC's broader US cyber insurance market hit $9.14 billion in direct written premiums for 2024 — the closest available benchmark. Globally, the Technology E&O market is estimated at $574 million in 2025, growing at a 6.2% CAGR through 2033, though that figure is not US-specific.

What is Tech E&O insurance coverage?

Tech E&O is a professional liability policy covering third-party claims arising from technology product failures, professional service errors, breach of contract, and related negligence. It's distinct from general liability (which covers physical harm) and cyber insurance (which covers breach response costs).

Who needs Technology Errors & Omissions insurance?

Any company that develops, sells, or services technology products — including SaaS companies, AI developers, IT consultants, managed service providers, fintech firms, and cloud platforms. If a client could suffer financial harm from your product or service failing, Tech E&O coverage applies.

Is the Tech E&O market growing in 2026?

Yes. Reported US cyber and Tech E&O incidents rose 38% in 2025, driven by ransomware severity, AI-related claims, and expanding privacy regulation. Current buyer-favorable pricing makes 2026 a strategic time to purchase or increase coverage before conditions tighten.

How does Tech E&O insurance differ from cyber liability insurance?

Tech E&O covers third-party claims from product or service failure — a client suing you because your software caused them financial harm. Cyber liability primarily addresses first-party breach response costs and third-party privacy claims. Many carriers now offer bundled policies covering both to eliminate gaps between the two.

What factors affect Tech E&O insurance premiums in 2026?

Premiums are shaped by company revenue, the type of technology offered (AI tools face more scrutiny than established SaaS), client contract exposure, claims history, and cybersecurity controls. For companies building or deploying AI, governance documentation has become an increasingly relevant underwriting factor.