Cost?](https://file-host.link/website/somainsure-hpf9ow/assets/blog-images/b47adec1-e78f-4302-830d-7ee913ce8594/1781006975738458_ab208b0a196f459e8a8b3da661e675fb/360.webp)

Premiums vary widely. A low-risk solopreneur might pay under $50/month, while a technology company or engineering firm could pay $150–$240+. There's no single price because your industry, business size, coverage limits, and claims history all pull the number in different directions.

This guide breaks down typical cost ranges, the factors that move premiums up or down, industry-by-industry benchmarks, and how to find the right coverage without overpaying — or underinsuring.

Key Takeaways

- Typical range: $19–$88/month for most small businesses; $140–$240+ for higher-risk professions like architects, engineers, and tech companies

- Biggest pricing drivers: Industry risk, business size, coverage limits, deductible, and claims history

- Who pays less: Low-risk solopreneurs, newer/smaller service businesses with limited client exposure

- Who pays more: Businesses with prior claims or contracts requiring higher limits

- Don't just buy cheap: Low-limit policies often won't cover a real claim — match limits to your actual exposure

How Much Does E&O Insurance Cost?

E&O insurance doesn't have a set price. Benchmarks from major insurers and brokers cluster around a wide range depending on methodology and customer base:

- Progressive Commercial reports a 2025 median of $50/month and an average of $69/month for new professional liability customers

- The Hartford puts the typical small business at $76/month for a standalone policy

- Insureon's small-business customer data shows $88/month (or $1,051/year), with annual premiums ranging from roughly $400 to over $7,000

None of these figures are universal — they reflect different customer bases and methodologies, so your actual premium could fall well above or below any of them.

Focusing only on the monthly number is the real trap. Businesses that shop on price alone often end up with limits too low to cover a real claim, or a policy structure they don't fully understand when it matters most.

Entry-Level / Low-Risk Coverage

Typical range: $19–$45/month

NEXT Insurance reports that 73% of its E&O customers pay $45/month or less, with coverage available from as little as $19/month for the lowest-risk profiles.

Most policies at this tier include basic per-claim and aggregate limits (often $250K–$500K), defense cost coverage, and a claims-made structure. This range works well for solo practitioners, notaries, tax preparers, and bookkeepers — anyone with limited client exposure and a straightforward service scope.

Mid-Range Coverage

Typical range: $50–$100/month

This is where most consultants, real estate agents, insurance agents, accountants, and marketing agencies land.

Policies here typically carry $1M per-claim limits, broader covered services, and sometimes cyber add-ons. Expect to land in this tier if you run an established service business with multiple clients, face contractual coverage requirements, or operate in a moderately regulated industry.

High-End / Complex Coverage

Typical range: $140–$240+/month

Technology companies, architects, engineers, property managers, and healthcare professionals typically fall into this tier.

Coverage at this level includes:

- Higher aggregate limits and tailored endorsements for industry-specific risks

- Broader retroactive date coverage to protect against claims from prior work

- Designed for higher-risk professions, businesses with large contract values, or industries that face frequent or expensive litigation

Key Factors That Affect E&O Insurance Cost

Insurers calculate E&O premiums by assessing the overall risk your business presents. These are the variables that move the number most.

Industry and Profession

Profession type is the single biggest pricing driver. A notary faces far fewer high-stakes errors than a software developer or civil engineer. Insurers price based on two things: how likely a claim is, and how large that claim could get.

Regulated professions — real estate agents, insurance agents — may also face state-mandated minimum coverage requirements that affect how policies are structured and priced.

Business Size and Revenue

More employees involved in client work means more opportunities for mistakes or miscommunication. Higher revenue often signals larger contract values at stake. Both factors scale up risk exposure and, consequently, premiums.

Coverage Limits and Deductibles

- Higher per-claim and aggregate limits = higher premium

- Higher deductible = lower monthly premium, but more out-of-pocket when a claim occurs

- Most E&O policies are written on a claims-made basis — meaning the policy must be active both when the error occurs and when the claim is filed

One structural detail many buyers miss: some policies include defense costs within the policy limit. This means legal fees reduce the amount available for a settlement. A $500K policy with defense-within-limits can leave very little for the actual judgment if litigation is prolonged.

Claims History and Years in Business

Businesses with prior E&O claims are considered higher risk and typically face higher premiums at renewal. The same logic applies to newer businesses — without a track record, insurers have less data to work with and typically price that uncertainty into the premium.

Location

State regulations, litigation frequency, and local market conditions all influence pricing. Insureon data shows meaningful variation by state for professional liability coverage:

| State | Avg. Monthly Premium |

|---|---|

| New York | $97 |

| California | $94 |

| Texas | $91 |

| Georgia | $83 |

| Pennsylvania | $79 |

E&O Insurance Cost by Industry

The table below reflects starting baselines from insurer data — not final quotes. Individual premiums vary by services, revenue, limits, deductible, and claims history.

| Profession | Approx. Monthly Premium | Annual Equivalent |

|---|---|---|

| Notary | ~$20 | ~$240 |

| Tax preparer | ~$20 | ~$240 |

| Insurance agent | ~$35 | ~$420 |

| Accountant / bookkeeper | $40–$73 | $480–$876 |

| Business / management consultant | ~$60 | ~$720 |

| Civil engineer (solo) | ~$65 | ~$780 |

| IT consultant | ~$65 | ~$785 |

| Real estate agent | ~$70 | ~$840 |

| Architect | ~$141 | ~$1,695 |

| Engineer (broad category) | ~$168 | ~$2,010 |

| Property manager | ~$140 | ~$1,680 |

| Technology company | ~$146 avg. minimum | ~$1,752 |

The gap between a $20/month notary premium and a $168/month engineering premium isn't arbitrary. Ames & Gough's 2025 A&E professional liability survey found that 82% of surveyed A&E insurers paid multimillion-dollar claims, including 44% that paid between $1M and $4.9M. When a single error can trigger that kind of loss, insurers price accordingly.

At the lower end, the stakes of a notarial error or a tax preparation mistake are contained — these claims rarely escalate to seven-figure litigation.

That changes for complex or niche operations. Fintech firms, healthcare technology companies, and specialized consultancies often struggle to get competitive quotes from standard markets — or get declined outright. Soma works with carriers including Chubb, Hiscox, Kinsale, Markel, and CRC Group to place these professional liability risks that standard markets price high or won't touch.

How to Lower Your E&O Insurance Premium

Compare Quotes Across Multiple Carriers

Premiums for identical coverage can vary significantly between insurers. A broker with access to a broad carrier network — rather than a handful of preferred markets — can compare options with a single submission. Soma routes businesses through carriers like Chubb, Hiscox, Liberty Mutual, Markel, and Kinsale without requiring multiple separate applications.

Adjust Deductibles and Limits Strategically

Two levers directly affect your premium:

- Deductible: A higher deductible lowers your monthly cost, but you pay more out-of-pocket when a claim hits

- Coverage limit: Don't choose the cheapest option — choose based on realistic financial exposure in your contracts

A $250K limit might look attractive at $30/month. But if your largest client contract is worth $500K, that gap is your problem, not the insurer's.

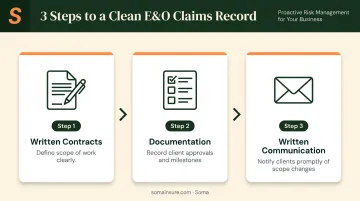

Maintain a Clean Claims Record and Continuous Coverage

Even one E&O claim can trigger a premium increase at renewal. Proactive steps that reduce exposure:

- Clear written contracts with defined scope of work

- Documentation of client approvals and project milestones

- Prompt written communication when scope changes

Don't let a claims-made policy lapse. A gap in coverage leaves prior work unprotected. If you cancel your E&O policy after completing a project and a client files a claim six months later, there's no coverage — regardless of whether your work was actually at fault.

What Most Business Owners Get Wrong About E&O Insurance Cost

Most buyers fixate on the monthly premium and miss the three mistakes that actually cost them money.

Choosing coverage limits based on price. A $25K coverage limit costs less per month — until a $50K lawsuit hits that policy. Your business covers the gap out of pocket. The cheaper policy isn't a deal; it's a deferred expense.

Missing the claims-made structure. E&O coverage must be active when the claim is filed, not just when the work was performed. Canceling a policy after a project wraps feels like saving money. It eliminates coverage for everything you've already done.

Underestimating industry-specific exposure. Tech firms, financial consultants, and healthcare-adjacent businesses consistently underestimate risk relative to revenue. A single dispute over a software bug or a flawed financial recommendation can exceed a full year's income — and the annual premium for adequate coverage rarely comes close.

Conclusion

E&O insurance costs vary significantly based on profession, business size, coverage limits, location, and claims history. A solo tax preparer and a SaaS company both need E&O coverage — but they're buying very different policies at very different price points.

This guide gives you a framework for identifying where your business falls in that range. From there, the most effective next step is working with a broker who has access to multiple carriers — so your specific risk profile gets matched to the right market, not just the first available quote.

That's what Soma does. As an independent commercial brokerage, Soma places E&O coverage across a broad network of carriers for businesses in tech, finance, healthcare, construction, and more — including complex or hard-to-insure operations that standard markets often decline.

Frequently Asked Questions

How much does professional liability insurance typically cost?

Most small businesses pay between $50 and $88/month, based on current data from Progressive Commercial and Insureon. Professional liability and E&O insurance are often used interchangeably. Actual cost depends on your profession, business size, coverage limits, and claims history.

What does errors and omissions insurance actually cover?

E&O covers legal defense costs, settlements, and judgments when a client claims your professional advice or services caused them financial harm. Coverage applies even if the claim lacks merit — the insurer pays to defend you up to the policy limit.

Is E&O insurance required by law?

Some states require it for licensed professions — Colorado, Louisiana, Tennessee, Kentucky, Alaska, South Dakota, and Oregon among them. Even where it's not mandated, clients or contracts often require it.

What is the difference between E&O insurance and general liability insurance?

General liability covers bodily injury and property damage. E&O covers financial losses arising from professional mistakes, omissions, or failure to deliver services as promised. A client tripping in your office is a GL claim; a client losing money because of your advice is an E&O claim.

How do coverage limits affect E&O insurance premiums?

Higher per-claim and aggregate limits increase the premium. Lower limits reduce it — but any costs above the cap come out of your pocket. Set limits based on realistic contract values and risk exposure, not on what produces the lowest monthly payment.

Can a business with prior E&O claims still get coverage?

Yes. Prior claims don't disqualify a business, but they typically result in higher premiums. A broker with access to specialty market carriers can often find competitive options even with a claims history on file.