Introduction

Financial advisors operate in one of the most legally exposed professions in the country. A single disputed recommendation can trigger an arbitration filing or lawsuit costing tens of thousands of dollars to defend — even if you did nothing wrong. A client who suffered losses, a missed disclosure on a complex product, a misunderstood risk tolerance conversation: any of these can be enough.

FINRA reported 906 new arbitration filings through April 2026, including 629 customer cases. That's not a hypothetical risk. It's the operating environment for anyone providing paid financial advice.

E&O insurance exists specifically to protect advisors from that exposure. This guide covers what it is, what it covers and excludes, whether it's required, what it costs, and how to choose the right policy — intended for RIAs, independent financial advisors, financial planners, and advisory firm owners evaluating or updating their professional liability coverage.

TL;DR

- Legal defense costs, settlements, and judgments from negligent advice claims fall under E&O insurance — not general liability, which covers bodily injury and property damage

- The SEC doesn't require E&O federally, but Oregon and Oklahoma mandate it, and Schwab requires a $1M minimum for all RIAs using its custodial platform

- Claims-made policies tie coverage to your retroactive date and reporting deadlines — both become critical if you switch carriers

- Fraud, cyber incidents, employment claims, and bodily injury are standard exclusions; advisors typically need separate policies for each

- $1M per occurrence is the standard starting point; your AUM, client profile, and custodian requirements determine the right limit

What Is E&O Insurance for Financial Advisors?

E&O insurance — also called professional liability insurance, professional indemnity insurance, or malpractice insurance depending on the carrier and context — protects financial advisors and their firms from lawsuits alleging negligence or failure to meet professional duties.

It is not the same as general liability (GL) insurance. GL covers physical harm: a client slips in your office, or property gets damaged. E&O covers financial harm — the losses a client claims resulted from your advice, analysis, or services. Advisors typically need both, because they address different risks.

What Scenarios Does E&O Actually Cover?

Two examples make this concrete:

Scenario 1: A client invests in an alternative fund you recommended. The fund underperforms sharply, and the client claims you failed to explain the liquidity risks. They file a FINRA arbitration claim. Your E&O policy covers your legal defense and any resulting settlement or award.

Scenario 2: An administrative error results in a trade being placed in the wrong account, creating a tax event the client didn't authorize. The client sues for damages. E&O responds to the claim — even though it was a mistake, not intentional conduct.

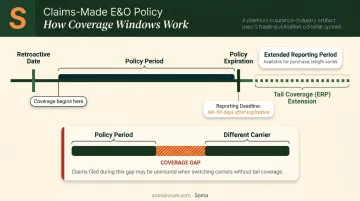

The Claims-Made Structure: Why Timing Matters

E&O policies are "claims-made" policies, not occurrence-based ones. IRMI explains that a claims-made policy is triggered when the claim is first made, and the underlying event must have occurred after the policy's retroactive date.

Two things advisors frequently overlook:

- Retroactive date gaps: Switching carriers to a policy with a later retroactive date leaves prior events uncovered — even when the claim is filed while the new policy is active

- Reporting windows: Claims-made-and-reported policies typically require reporting within the policy period or within 60–90 days of expiration — miss that deadline and coverage may be forfeited

When switching carriers, verify that your new policy's retroactive date aligns with — or predates — your prior policy's inception date. Extended Reporting Period (ERP) endorsements, sometimes called "tail coverage," let you report claims after a policy expires for events that occurred before expiration.

What Does E&O Insurance Cover — and What Doesn't It Cover?

Standard Coverages

A well-structured financial advisor E&O policy typically covers:

- Legal defense costs — attorney fees, court filing fees, and expert witness costs

- Settlements — amounts agreed to outside of court

- Judgments — court-ordered damages

- Covered claim types — negligence, errors in financial analysis, omissions in advice, misrepresentation, and failure to render services as promised

Some policy structures also provide coverage for costs related to regulatory investigations by the SEC or FINRA — but this varies widely by carrier and policy form. Review this specifically with your broker; don't assume it's included.

The specific trigger language in your actual policy governs — not marketing descriptions. For reference, Markel's investment advisors coverage operates on a "right and duty to defend" basis and pays on behalf of the insured; Chubb's Asset Management Protector covers investment advisers and affiliated service providers. Policy forms differ, so always read your actual contract.

Common Exclusions

Most financial advisor E&O policies exclude:

- Intentional misconduct or fraud — deliberate wrongdoing isn't covered

- Criminal acts — no coverage for criminal convictions or indictments

- Bodily injury and property damage — covered under a separate general liability (GL) policy

- Cyber incidents and data breaches — these require a separate cyber liability policy

- Employment practices claims — harassment, discrimination, and wrongful termination need an EPLI policy

- Incidents predating the retroactive date — no coverage for historical acts outside the covered window

Coverage Limits: Occurrence vs. Aggregate

Two numbers define how much protection you actually have:

| Limit Type | What It Means |

|---|---|

| Per-occurrence limit | Maximum payout for a single claim |

| Aggregate limit | Maximum total payout across all claims in the policy period |

A $1M/$3M structure means the insurer pays up to $1M on any one claim, and up to $3M total across all claims in that policy year.

One important note on group/master policies: Some association programs pool multiple firms under a single aggregate limit. If other firms in the pool exhaust the aggregate before you file a claim, coverage may not be available. Individual policies avoid this risk entirely.

How Much Does E&O Insurance Cost for Financial Advisors?

No current authoritative market-wide median premium has been independently verified for financial advisor E&O coverage. Figures circulate widely online, but sourcing is often unclear.

What is verified: one published RIA program quote showed $1M per claim / $1M aggregate coverage at $1,625 paid in full (approximately $128/month), including association membership fees, through the NAPA Benefits RIA program. That's a program quote, not a market average. Your actual premium will vary based on your specific profile.

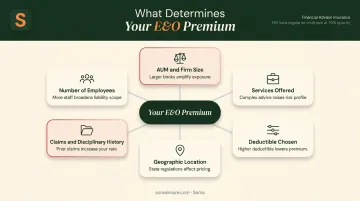

What Drives Your Premium

Underwriters price E&O based on several factors:

- AUM and firm size — higher AUM means higher potential claim severity

- Services offered — advisors managing alternative investments, options strategies, or complex structured products pay more than those running standard equity/fixed income portfolios

- Number of employees — more staff means more exposure points

- Claims and disciplinary history — prior E&O claims or ADV disclosures raise premiums

- Geographic location — states with more litigation activity affect pricing

- Deductible chosen — higher deductibles lower premiums but increase out-of-pocket costs per claim

InvestmentNews reported in June 2024 that E&O premiums had fallen sharply for one risk asset category, citing a Golsan Scruggs analysis — evidence that asset mix directly affects pricing trends.

Deductibles

Standard deductibles for financial advisor E&O policies typically range from $2,500 to $5,000. Choosing a higher deductible reduces your annual premium but increases what you pay out of pocket before coverage kicks in.

For a solo practice, a $5,000 deductible is often workable. For a firm with multiple advisors, higher claim frequency risk means a lower deductible may save money overall — even if annual premiums run higher.

Is E&O Insurance Required for Financial Advisors?

Federal Requirements

The SEC does not require registered investment advisers to carry E&O insurance. That said, most compliance professionals treat it as essential rather than optional — the SEC's enforcement activity ($8.2 billion in ordered financial remedies in FY2024) underscores the broader regulatory climate advisors operate in.

State Requirements

Two states have verified mandatory E&O requirements:

- Oregon: Under ORS 59.175(5) and OAR 441-175-0185, Oregon-based state investment adviser firms must maintain $1M in E&O coverage as a condition of licensure and annual renewal. Oregon's DFR Bulletin 2022-7 confirms that proof of continuous coverage is an examination subject and failure to maintain it can result in license cancellation

- Oklahoma: OAC 660:11-7-21 requires investment advisers registering in Oklahoma to maintain professional liability/E&O coverage, with a $1M per claim minimum and requirements around proof via declaration page, acceptable insurers, and notice of cancellation

Kansas has surfaced in secondary discussions as requiring advisors to disclose whether they carry professional liability insurance, but that is not a confirmed mandate from primary regulatory sources.

If you're registered in multiple states, check each state securities regulator directly — requirements can change.

Custodian Requirements

Schwab Advisor Services requires all RIA firms working with it to maintain an aggregate minimum of $1M in insurance covering E&O, social engineering, theft by hackers, and employee theft where applicable.

Schwab also notes that securing coverage can take up to 90 days: if you're transitioning to Schwab as a custodian, start the insurance process well before your go-live date.

No equivalent public minimum requirement was verified for Fidelity Institutional, Pershing/BNY, or Altruist. If you custody elsewhere, contact your custodian directly to confirm their current insurance requirements before binding coverage.

How to Choose the Right E&O Policy for Your Firm

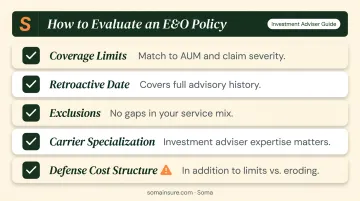

Key Variables to Evaluate

When comparing policies, assess:

- Coverage limits: confirm they match your AUM and the realistic severity of client claims

- Retroactive date: verify it covers your full history of advisory work, not just recent engagements

- Exclusions: look for carve-outs that could create gaps specific to your service mix

- Carrier specialization: a carrier that regularly underwrites investment adviser E&O reads your risk differently than a generalist

- Defense cost structure: determine whether defense costs are paid in addition to your policy limits or erode them

Why Online Quote Forms Fall Short

Quick-quote platforms and one-size-fits-all association programs are convenient, but they often include restrictive exclusions and sublimits that only surface at claim time. The policy that looks adequate at $1,600/year may exclude the specific service type that generated the claim.

Working with a specialist broker who can canvas multiple carriers — one who understands how financial advisor E&O policies are actually structured and priced — is the better approach.

Soma places coverage for investment advisors, RIAs, lenders, and fintech firms through specialty carriers including Chubb, Markel, and Hiscox. That includes E&O, cyber liability, fiduciary liability, D&O, and crime coverage — coordinated as a single program rather than separate applications. Advisors work through Soma's Risk Management Team to compare options across carriers with one intake process.

How to Reduce Your Risk of an E&O Claim

The best E&O policy is one you never need to use. Understanding what actually drives claims is the first step to avoiding them. Most trace back to a small set of triggers:

- Unsuitable investment recommendations relative to the client's documented risk tolerance

- Failure to document client conversations, instructions, and investment rationale

- Miscommunication about product terms, fees, or risks

- Administrative errors in trade execution or account management

Documentation as Your Primary Defense

If a claim is filed, documentation is often the deciding factor — not the merits of the advice itself. Advisors who can produce:

- Written records of client conversations and meeting notes

- Signed acknowledgments of risk disclosures provided

- Clear documentation of why a recommendation was suitable

- Trade confirmations and account change authorization trails

...are better positioned to defend a claim quickly and successfully — often resolving disputes before they reach litigation.

Ongoing Policy and Compliance Review

E&O coverage should grow with your firm. A policy that was adequate at $50M AUM may be dangerously thin at $300M AUM. Revisit your coverage annually alongside your compliance calendar — when AUM grows, when you add services, when you bring on employees, or when state or custodian requirements change.

Frequently Asked Questions

Frequently Asked Questions

How much does E&O insurance cost for financial advisors?

Costs vary based on firm size, AUM, services offered, location, and claims history. One published RIA program showed $1M/$1M coverage available for approximately $1,625/year through an association program (a program rate, not a market average). Request carrier quotes through a specialist broker to get pricing specific to your practice.

Is E&O insurance required for financial advisors?

There is no federal SEC requirement. Oregon and Oklahoma explicitly mandate E&O coverage for state-registered investment advisers, both requiring at least $1M per claim. Charles Schwab requires all RIAs on its platform to carry a $1M aggregate minimum covering E&O, social engineering, and related risks.

What is the difference between E&O insurance and general liability for financial advisors?

General liability covers physical harm — bodily injury and property damage. E&O covers professional harm — financial losses clients attribute to errors, omissions, or negligence in your advisory work. Advisors need both; neither policy substitutes for the other.

What does E&O insurance not cover for financial advisors?

Standard exclusions include intentional fraud or criminal acts, cyber incidents and data breaches, bodily injury, employment practices claims, and any incidents that predate the policy's retroactive date. Separate policies (cyber liability, EPLI) are needed for those exposures.

How much E&O coverage does a financial advisor need?

$1M per occurrence is the common floor, and it's the minimum Schwab and Oregon/Oklahoma require. The right limit depends on your AUM, service complexity, client concentration, and any custodian or state minimums that apply.

Is E&O insurance worth it for financial advisors?

Yes. Legal defense alone for a single arbitration or lawsuit can reach $50,000–$100,000+ before any settlement or judgment is reached. For any advisor providing paid professional advice, E&O coverage is a basic cost of operating responsibly — the premium is modest relative to the exposure it covers.