Introduction

Securities professionals operate in one of the most litigation-prone sectors of the U.S. economy. In 2024 alone, FINRA recorded 2,469 arbitration filings — 65% of them customer disputes — while the SEC's enforcement division produced $8.2 billion in financial remedies across 583 actions.

For broker-dealers and registered investment advisors (RIAs), that exposure doesn't pause. Client claims, regulatory investigations, data breaches, and employee fraud are recurring realities — and standard commercial insurance policies routinely fail to cover any of them.

This guide covers the essential insurance coverages for broker-dealers and RIAs: which are legally required, where BD and RIA needs diverge, and what to prioritize when evaluating policies.

TL;DR

- E&O insurance is the most critical coverage — it protects against client claims of bad advice, unsuitable recommendations, and failure to follow instructions

- Fidelity bonds are mandatory for FINRA-member broker-dealers under Rule 4360, with minimums tied to net capital

- D&O and cyber liability are increasingly necessary — enforcement actions are rising and data breach costs average $6.08M for financial firms

- RIAs and broker-dealers carry different risk profiles: RIAs face ongoing fiduciary duty claims while broker-dealers face transaction-specific disputes, so coverage structures differ significantly

- A specialist broker familiar with securities industry risks prevents the coverage gaps that general commercial brokers routinely miss

Broker-Dealers vs. Investment Advisors: Key Differences That Shape Insurance Needs

Understanding the regulatory distinction between these two firm types isn't just legal background — it directly determines which insurance exposures are highest and which coverages are non-negotiable.

What Is a Broker-Dealer?

A broker-dealer is a person or firm that buys and sells securities on behalf of clients (broker function) and/or its own account (dealer function). Broker-dealers register with the SEC, must join a self-regulatory organization (FINRA for most), and follow Regulation Best Interest (Reg BI).

Reg BI is a conduct standard that applies at the point of a recommendation to a retail customer — it took effect June 30, 2020.

Their risk is transactional. Each recommendation, trade execution, or account opening is a separate exposure event — and each one can generate a claim.

What Is a Registered Investment Advisor?

An RIA provides ongoing, personalized investment advice for a fee and is held to a continuous fiduciary standard under Section 206 of the Investment Advisers Act of 1940. Registration threshold matters here:

- Under $100M AUM → typically state-registered

- $100M–$110M AUM → may register with the SEC

- Above $110M AUM → must be SEC-registered

Unlike broker-dealers, RIAs are compensated through fees rather than commissions, and their duty of care doesn't end after a transaction — it continues for the life of the client relationship.

Why This Matters for Insurance

| Factor | Broker-Dealer | RIA |

|---|---|---|

| Standard of conduct | Best interest at point of recommendation (Reg BI) | Continuous fiduciary duty |

| Compensation model | Commission-based | Fee-based |

| Primary regulator | FINRA / SEC | SEC or state regulators |

| Primary liability trigger | Transaction-specific disputes | Ongoing advice and relationship management |

| Fidelity bond requirement | Mandatory (FINRA Rule 4360) | Varies by state and custody status |

These structural differences flow directly into how underwriters assess risk — and why E&O policy language, fidelity bond requirements, and coverage limits vary so sharply between the two firm types.

Why These Firms Face Unique and Elevated Insurance Risks

Client Litigation Is Frequent and Expensive

FINRA's 2024 dispute resolution statistics reveal the most common allegations driving customer arbitration cases:

- Breach of fiduciary duty — 1,518 instances

- Negligence — 1,126

- Suitability — 1,022

- Misrepresentation — 923

- Breach of Reg BI — 652

Average arbitration case duration: 12.5 months. Defense costs alone can reach six figures before any settlement or award.

Regulatory Enforcement Adds Another Layer

FINRA's 2024 enforcement statistics paint a clear picture of firm-level exposure:

- 730 disciplinary actions filed

- $75.6M in fines and disgorgement collected

- 182 broker bars issued

- 354 individual suspensions handed down

- 124 officer-and-director bars brought separately by the SEC in FY2024

These aren't just firm-level consequences. Individual executives face personal sanctions, which is precisely why D&O insurance exists for securities firms. Regulatory risk doesn't stop at the company level — it follows people.

Cyber Incidents Are Targeting Financial Data

According to IBM's 2024 Cost of a Data Breach report, the average data breach cost in financial services reached $6.08M, well above the global average of $4.88M. Broker-dealers and RIAs hold dense concentrations of sensitive client data: Social Security numbers, account balances, tax information, and transaction histories.

FINRA has specifically documented coordinated attacks targeting member firms. Standard business policies exclude most breach events, making standalone cyber liability coverage a practical necessity for firms holding this volume of sensitive data.

Essential Insurance Coverages: A Complete Breakdown

Errors & Omissions (E&O) / Professional Liability Insurance

E&O is the foundational coverage for any securities firm. It protects the firm and its representatives against client claims that professional advice, recommendations, or services caused financial harm — whether or not actual negligence occurred.

What a typical E&O policy covers:

- Defense costs for client arbitration or litigation

- Settlements and judgments from unsuitable recommendation claims

- Failure to follow client instructions

- Misrepresentation in investment advice

- Errors in account management

What it typically excludes:

- Intentional fraud or criminal acts

- Bodily injury or property damage

- Claims arising from services outside the policy's defined scope

For RIAs, continuous fiduciary exposure makes E&O a permanent necessity. For broker-dealers, the volume of transactions — each one a potential dispute trigger — makes it equally critical.

Fidelity Bond / Crime Insurance

A fidelity bond covers losses from employee dishonesty, theft, forgery, computer fraud, and securities fraud against the firm's own assets.

Here's a distinction that often gets confused: SIPC and a fidelity bond are not the same thing. SIPC protects customer assets if a brokerage firm fails financially. A fidelity bond protects the firm itself from crime losses. They serve entirely different purposes and neither substitutes for the other.

Directors & Officers (D&O) Insurance

D&O insurance protects executives and board members from personal liability arising from decisions made in their leadership capacity. For securities firms, this covers regulatory investigations, investor claims directed at management, and shareholder suits.

D&O policies are typically structured in three parts:

- Side A — Protects individual directors and officers when the firm cannot indemnify them directly

- Side B — Covers the firm's costs when it steps in to indemnify an executive

- Side C — Extends protection to the entity itself for securities claims

Side C coverage is particularly relevant for registered broker-dealers and RIAs — entity-level securities claims are a recurring enforcement pattern. The SEC's 2024 sweep against nine RIAs for Marketing Rule violations is a clear example of exactly this exposure.

Cyber Liability Insurance

For financial services firms, cyber liability covers:

- Data breach notification costs

- Regulatory defense under SEC Regulation S-P (which now requires breach notification within 30 days of awareness)

- Client credit monitoring and identity restoration

- Ransomware response and recovery

- Business interruption losses from cyberattacks

The 2024 amendments to Reg S-P — adopted May 16, 2024 — impose written incident response requirements on broker-dealers and RIAs alike. Non-compliance is an enforcement risk on top of the breach cost itself.

For RIAs and broker-dealers, cyber liability works best as part of a coordinated multi-policy program — paired with E&O, D&O, and crime coverage to close the gaps that standalone policies leave open.

Employment Practices Liability (EPLI) and General Liability

Any firm with employees needs EPLI coverage for claims of discrimination, harassment, and wrongful termination. General liability covers third-party bodily injury or property damage at office premises.

Neither coverage is securities-specific, but both are standard components of a complete program — and gaps in either can expose the firm to costly claims that core financial lines won't touch.

What's Legally Required: Regulatory Insurance Mandates

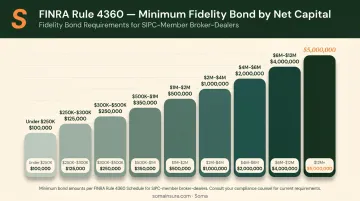

FINRA Fidelity Bond Requirement (Rule 4360)

FINRA Rule 4360 requires every SIPC-member broker-dealer to maintain a blanket fidelity bond. Required insuring agreements include fidelity, on premises, in transit, forgery and alteration, securities, and counterfeit currency. Minimum coverage is scaled to the firm's net capital requirement:

| Net Capital Requirement | Minimum Fidelity Bond |

|---|---|

| Less than $250,000 | Greater of $100,000 or 120% of net capital |

| $250,000 – $300,000 | $600,000 |

| $300,001 – $500,000 | $600,000 |

| $500,001 – $1,000,000 | $800,000 |

| $1,000,001 – $2,000,000 | $1,000,000 |

| $2,000,001 – $3,000,000 | $1,500,000 |

| $3,000,001 – $6,000,000 | $2,000,000 |

| $6,000,001 – $12,000,000 | $4,000,000 |

| $12,000,001 or more | $5,000,000 |

FINRA reviews fidelity bond compliance during routine examinations. If a bond is cancelled, terminated, or substantially modified, the firm must notify FINRA promptly in writing. Violations are included in FINRA's Minor Rule Violation Plan schedule.

SEC and State Requirements for Investment Advisors

The Investment Advisers Act of 1940 does not universally mandate E&O insurance at the federal level. However, state requirements vary considerably:

- Oregon requires proof of at least $1M in E&O coverage for state-regulated investment adviser firms

- Alaska requires a $35,000 surety bond for advisers with custody and a $10,000 bond for advisers with discretionary authority

- Virginia imposes net worth and surety bond requirements under 21VAC5-80-180

The NASAA Model Rule on bonding further requires bonds for advisers with custody or discretion who don't meet minimum net worth standards. Before quoting coverage, confirm the specific state registration requirements for each jurisdiction where the firm operates.

Advisers subject to NASAA's model custody rule also face surprise audits, qualified custodian requirements, and quarterly statement obligations. Together, these obligations increase liability exposure enough that crime and E&O coverage becomes practically necessary even where not strictly mandated.

SIPC Membership: What It Covers (and What It Doesn't)

Most broker-dealers are required to become SIPC members before conducting business. SIPC provides up to $500,000 per customer (including $250,000 for cash) if a brokerage firm fails financially.

What SIPC does not cover:

- Declines in investment value

- Bad investment advice or unsuitable recommendations

- Fraud against the firm itself

- D&O claims, cyber incidents, or regulatory defense costs

SIPC protects customers if a firm fails financially. It does not replace professional liability, crime, or D&O insurance.

How to Get the Right Coverage for Your Firm

Broker-dealer and RIA insurance is a specialty class. Many standard commercial insurers lack either the appetite or the underwriting expertise to structure policies that reflect actual securities industry risks.

What Underwriters Look At

When quoting coverage for a securities firm, underwriters evaluate:

- AUM (for RIAs) — a primary scale and exposure indicator

- Number of registered representatives — affects E&O premium and fidelity bond sizing

- FINRA disciplinary history — reviewed through BrokerCheck; prior actions materially affect pricing and availability

- Products offered — variable annuities, complex structured products, and alternatives carry higher E&O risk than plain-vanilla equity management

- Custody arrangements — advisers with direct custody face heightened underwriting scrutiny

- Prior claims history — the single largest pricing variable for most underwriters

Preparing Your Submission

Before approaching any carrier or broker, pull together:

- Form ADV (RIAs) or Form BD (broker-dealers), the primary disclosure documents underwriters use to assess your business

- BrokerCheck / IAPD history, with clear explanations ready for any disclosed events

- Supervisory procedures and compliance policies that demonstrate your firm's risk management practices

- Client demographics and investment strategy overview so underwriters can gauge concentration and complexity risk

Having this documentation ready before your first conversation with a broker speeds up the quoting process and signals to underwriters that your firm takes compliance seriously.

Soma works with broker-dealers, RIAs, lenders, and fintech firms to place coordinated insurance programs through carriers including Chubb, Markel, and Hiscox — each with dedicated financial services underwriting desks. Bundling E&O, cyber, D&O, fidelity/crime, and fiduciary liability into a single program eliminates the coverage gaps that typically appear when these policies are placed separately with different carriers.

Frequently Asked Questions

What types of insurance do small securities firms, broker-dealers, and investment advisors need?

The core program includes E&O/professional liability, a fidelity bond (mandatory for FINRA-registered BDs), D&O, cyber liability, and EPLI. The specific mix depends on firm size, structure, whether the firm has custody of client assets, and which states it operates in.

What is the difference between an investment advisor and a broker-dealer?

Broker-dealers execute securities transactions under a best interest standard (Reg BI) at the point of a recommendation and are regulated by FINRA. Investment advisors provide ongoing advice under a continuous fiduciary standard and are regulated by the SEC or state regulators depending on AUM.

Is E&O insurance required for broker-dealers and investment advisors?

No federal law universally mandates E&O. Some states do require it for investment advisor registration — Oregon mandates at least $1M in coverage. Given the litigation frequency in this sector, most firms carry it regardless of whether their state requires it.

What is a fidelity bond and is it required for broker-dealers?

A fidelity bond covers losses from employee theft, fraud, forgery, and securities-related crime. FINRA Rule 4360 mandates it for all SIPC-member broker-dealers, with minimum amounts ranging from $100,000 to $5M based on the firm's net capital requirement.

Does SIPC protection replace the need for insurance for broker-dealers?

No. SIPC protects customer assets when a brokerage firm fails financially — it does not cover professional liability claims, bad advice lawsuits, D&O disputes, cyber incidents, or employee fraud against the firm. Private insurance remains essential regardless of SIPC membership.

How much does insurance for broker-dealers and investment advisors typically cost?

Premiums vary based on AUM, number of registered representatives, claims history, products offered, and custody arrangements. Submit a complete application with your Form ADV or Form BD for an accurate quote — underwriters price based on your firm's actual risk profile, not a flat benchmark.