A single incident — a wet floor near the entrance, a broken floor mat, a refrigeration leak in the aisle — can produce a lawsuit that threatens your entire operation. Without the right coverage in place before that happens, the store absorbs every dollar.

This guide is written for retail store owners and operators. It covers the coverage you need, what it costs, how claims work, and what you can do to reduce both incidents and premiums.

TL;DR — Key Takeaways

- General liability (CGL) insurance is the foundation of slip and fall protection for retail stores

- Standard limits start at $1M per occurrence / $2M aggregate — high-traffic stores should carry more

- Claim costs average $45,000 for small businesses, with serious injuries regularly exceeding $500,000

- Documented safety programs and a clean claims history lower your premiums at renewal

- Working with a multi-carrier brokerage means better rates and broader coverage than any single carrier can offer

Why Slip and Fall Liability Is a Major Risk for Retail Stores

Your Legal Obligation as a Store Owner

Under U.S. premises liability law, customers are classified as invitees — the category owed the highest duty of care. Cornell Law's Legal Information Institute defines this as a duty to keep premises reasonably safe and to warn visitors of known dangerous conditions.

That means regular inspections, prompt hazard response, and adequate warnings. Failing any one of those duties is what courts look at when determining whether your store bears responsibility for a customer's injury.

The Financial Scale of the Risk

The numbers have been moving in the wrong direction for store owners:

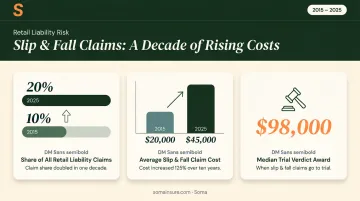

- Slip, fall, and customer injury claims now represent 20% of small-business claims, double the rate from 2015

- The average claim cost has grown from $20,000 to $45,000 in ten years

- Verisk's 2025 GL Loss Trends report shows premises/operations bodily injury severities are still rising — with some state-level increases above 35%

- Older Bureau of Justice Statistics data puts the median premises liability trial award at $98,000 for plaintiff winners

For small and mid-sized retailers, a single judgment at that level — or the legal defense costs alone — can be financially disabling.

Why Retail Is Particularly Exposed

Retail environments generate hazardous conditions constantly and quickly:

- Constant foot traffic means more opportunity for incidents, regardless of how well-managed the store is

- Product spills, refrigeration leaks, and liquid tracked in from weather all create slip hazards

- Plaintiff attorneys actively target retail defendants, knowing stores typically carry insurance

- Even a well-documented, well-run store can face a claim — and defending one costs money whether you win or lose

That last point matters: legal defense alone can run $50,000–$100,000 before a verdict is even reached. Coverage isn't just about losing — it's about staying in business while the case plays out.

What Insurance Coverage Retail Stores Need for Slip and Fall Protection

No policy is labeled "slip and fall insurance." Protection comes from layering several coverage types together.

Commercial General Liability (CGL) Insurance

CGL is the primary policy that handles slip and fall claims. It covers:

- Bodily injury — covers medical costs and damages when a customer is injured on your premises

- Medical payments — reimburses injured parties without requiring a liability finding, which can resolve minor claims quickly

- Legal defense costs — attorney fees and court costs if you're sued

- Settlements and judgments — up to your policy limits

CGL is non-negotiable for any retail operation. Most stores should carry at minimum $1 million per occurrence and $2 million aggregate, as Hartford and Next Insurance both document as standard starting limits. High-traffic stores — grocery, hardware, big-format retail — should evaluate whether those limits are sufficient.

Business Owner's Policy (BOP)

A BOP bundles general liability with commercial property insurance at a lower combined rate than buying each separately. For small to mid-sized retail stores, a BOP is usually the more efficient starting point.

It delivers the same slip and fall liability protection as standalone CGL, plus property coverage for your physical location and inventory. Many BOP policies also include medical payments coverage, letting you resolve minor injury costs before they become formal claims.

Commercial Umbrella / Excess Liability Insurance

When a claim exceeds your base policy limits — such as spinal injuries, permanent disability, or traumatic brain injuries — umbrella coverage kicks in. Hartford notes that commercial umbrella policies can provide additional aggregate limits from $1M to $15M above underlying policies.

For high-traffic retail operations, umbrella coverage is what stands between a manageable claim and a judgment that exceeds your base policy entirely.

Finding the Right Coverage Combination

Soma places retail coverage for storefronts, e-commerce operators, and multi-location businesses through carriers including The Hartford, Hiscox, and Progressive — covering slip-and-fall liability, product liability, business interruption, and storefront property. Soma also works with retail risks that standard markets decline, including high-inventory environments and multi-location operators.

How Much Does Retail Slip and Fall Insurance Cost?

Most retail stores pay between $42 and $95/month for core liability coverage — but your actual premium depends on several factors specific to your operation.

Retail Premium Benchmarks

Insureon's retail insurance cost data provides useful starting points:

| Coverage Type | Median Monthly Cost | Annual Estimate |

|---|---|---|

| General Liability (retail) | $42/month | ~$500/year |

| Business Owner's Policy (retail) | $95/month | ~$1,136/year |

| Commercial Umbrella (retail) | $59/month | ~$708/year |

By store type, the differences matter:

- Clothing stores: ~$42/month GL, ~$88/month BOP

- Grocery stores: ~$43/month GL, ~$87/month BOP

- Liquor/wine stores: ~$48/month GL, ~$161/month BOP

Key Underwriting Factors

Insurers weigh several variables when setting your premium:

- Larger stores and higher revenue translate directly to greater exposure — and higher premiums

- More foot traffic means more opportunity for incidents, so high-volume stores pay more

- Grocery and hardware stores carry higher base rates than boutique apparel due to inherent hazards (wet floors, heavy shelving, power tools)

- A single prior slip and fall claim can trigger higher renewal rates or coverage restrictions

- Documented safety programs — inspection logs, staff training records — can offset some of that cost

How to Reduce What You Pay

- Bundle coverage through a BOP rather than buying standalone GL

- Maintain a clean claims history — even one incident affects renewal pricing

- Implement and document a formal safety program (more on this below)

- Work with a broker who can compare quotes across multiple carriers rather than locking you into one carrier's pricing

What Happens When a Slip and Fall Claim Is Filed Against Your Store

The Claims Process

When a customer reports an injury, the process moves quickly:

- Report immediately — notify your insurer as soon as the incident occurs. Delays complicate coverage.

- Insurer assigns an adjuster — the adjuster evaluates liability and damages based on available evidence.

- Investigation begins — the adjuster may request photos of the incident scene, witness statements, and medical records.

- Defense is managed by your insurer — your carrier handles all communications with the plaintiff's legal team.

- Resolution — through settlement, dismissal, or trial verdict. BJS data shows roughly three-quarters of tort cases resolve by settlement, with half disposed within 14 months.

What Your Insurer Covers

Your CGL policy pays for:

- Attorney fees and legal defense throughout the process

- Settlement negotiations and payments

- Court costs if the case proceeds to trial

- Any judgment up to your policy limits

Adequate limits need to be in place before a claim is filed. Once an incident occurs, adjusting your coverage doesn't change what your policy will pay.

Why Your Own Documentation Is Critical

Your insurer can only work with what you've documented. Even the best coverage has limits when evidence is thin — stores with thorough records are in a measurably stronger position:

- Incident reports — completed immediately at the time of the event

- Surveillance footage — preserved before it's overwritten

- Witness statements — collected while memories are fresh

- Floor inspection logs — dated, signed records showing the area was monitored

Stores without documentation are far more vulnerable when disputing exaggerated or fraudulent claims.

Common Retail Hazards That Trigger Slip and Fall Claims

Insurers specifically evaluate these hazard categories during underwriting. Addressing them before a claim occurs also prevents underwriters from using them to justify a higher premium.

The most common hazard sources in retail environments:

- Wet or freshly mopped floors without adequate posted signage

- Liquid spills from products, refrigeration leaks, or beverage stations

- Rain and snow tracked in near store entrances, especially during seasonal weather

- Uneven flooring, raised thresholds, or worn/curled entrance mats

- Merchandise, pallets, or boxes left in customer aisles

- Poor lighting in storage areas, parking lots, or back-of-store zones

NIOSH's wholesale and retail trade safety guidance identifies spilled liquid as a primary slip cause and recommends flooring with a static coefficient of friction above 0.5 for high-risk areas.

Grocery stores, hardware stores, and large-format retailers face more scrutiny from underwriters due to refrigeration units, outdoor garden centers, heavy merchandise, and high customer volume. Insurers may conduct site inspections or ask about specific hazard management protocols. Stores that document their hazard controls consistently earn better terms and lower premiums.

How to Reduce Slip and Fall Risk and Lower Your Insurance Premiums

Core Elements of an Effective Prevention Program

A documented prevention program serves two purposes: it reduces actual incidents and it gives insurers evidence that your operation is managed responsibly.

The essentials:

- Conduct floor inspections every 30–60 minutes in high-risk areas, with signed logs as proof

- Post wet floor signage immediately and keep it visible until the surface is completely dry

- Assign spill response responsibilities to specific staff so cleanup is fast and consistent every time

- Replace worn or damaged entrance mats regularly, particularly heading into rain and snow seasons

- Build seasonal procedures for rain and snow tracking near entrances into your standard operating routine

Documentation Practices That Matter to Insurers

The paper trail you build before a claim is the same paper trail used to defend one:

- Written inspection logs with date, time, and employee signature

- Incident report templates that staff know how to complete

- Employee training records showing safety procedures were communicated

- Maintenance logs for flooring, lighting, and entrance conditions

Stores without documentation have no objective basis to dispute a claim. Courts don't give credit for safety practices that can't be proven.

That documentation also has direct financial value — which connects directly to what you pay for coverage.

Premium Credits for Safety Programs

Some insurers offer premium discounts or credits for retail stores with formal safety programs, staff training certifications, or documented loss control measures. A clean claims history combined with verifiable safety practices can meaningfully reduce what you pay each year. Ask your broker specifically about available credits — carriers don't always apply them without a conversation.

Frequently Asked Questions

How much is a slip and fall claim in a retail store?

Costs vary based on injury severity. The Hartford's 2025 data puts the average small-business slip and fall claim at $45,000, while BJS data shows median premises liability trial awards of $98,000 for plaintiff winners in tried cases. Severe injuries — spinal damage, fractures, traumatic brain injuries — can push claims into the hundreds of thousands, which is why adequate coverage limits matter.

What kind of insurance does a retail store need?

Commercial general liability (CGL) is the essential coverage. A Business Owner's Policy (BOP) is the efficient option for most smaller stores since it bundles GL with property coverage at a lower combined cost. High-traffic stores should add a commercial umbrella policy to protect against claims that exceed base policy limits.

Does general liability insurance cover slip and fall claims?

Yes. CGL is the primary policy that responds to customer slip and fall claims. It covers legal defense costs, medical payments, settlements, and judgments resulting from third-party bodily injury on your premises — up to your policy limits.

How much does slip and fall insurance cost for a retail store?

A typical small retail store pays around $42/month ($500/year) for standalone general liability, or approximately $95/month ($1,136/year) for a BOP, based on Insureon's retail benchmarks. Actual premiums depend on store size, type of retail operation, foot traffic, and claims history.

Can a retail store be sued even if wet floor signs were posted?

Yes. A wet floor sign reduces but does not eliminate liability. If the hazardous condition was excessive, the warning inadequate, or other negligence present, a claim can still succeed. Cases like Helms v. Wal-Mart confirm that courts evaluate warning adequacy on the specific facts, not the presence of a sign alone. Coverage remains necessary regardless of the precautions taken.

What happens to my insurance after a slip and fall claim is filed?

A filed claim typically affects premiums at renewal — Hartford lists claims history as a direct cost factor, and stores with multiple claims may face higher rates or reduced carrier options. Working with a broker like Soma, who accesses multiple carriers, helps since different insurers weigh loss history differently.