Most businesses discover this the hard way — after weeks of waiting on quotes, chasing brokers for updates, or finding out mid-renewal that their broker can't place a key coverage line because the risk is too complex for standard markets.

This guide cuts through that noise. Below are five leading retail insurance brokers in the USA, evaluated on market reach, specialty capability, carrier access, and ability to handle both standard and hard-to-place commercial risks.

TL;DR

- Retail insurance brokers work directly with businesses to find and place coverage; they represent the client, not any single carrier

- The US market has over 435,000 brokerage businesses, but only a small number have the carrier depth and E&S access to handle complex commercial placements

- Surplus lines premiums hit $131 billion in 2024, representing 12% of the total US P&C market

- Key selection criteria: carrier network depth, industry specialization, E&S market access, and quote turnaround speed

- This list covers five brokers, from global giants to specialist firms, evaluated on industry fit, specialization, and carrier access

What Is a Retail Insurance Broker?

A retail insurance broker is a licensed professional who works directly on behalf of businesses or individuals to identify, compare, and place the most appropriate insurance coverage. Their legal and professional duty runs to the client — not to any carrier. That means their incentive is finding the right fit for your business, not pushing a preferred product.

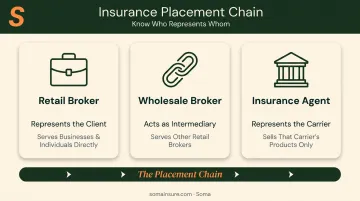

Retail vs. Wholesale vs. Agent

These three roles get conflated constantly, but they serve very different functions:

| Role | Who They Represent | Who They Serve |

|---|---|---|

| Retail Broker | The client | Businesses and individuals directly |

| Wholesale Broker | Acts as intermediary | Other retail brokers (not end clients) |

| Insurance Agent | The carrier | Sells that carrier's products only |

Retail brokers sit at the client-facing end of the placement chain. When a risk is too complex or unusual for standard admitted markets, a retail broker may route it through a wholesale intermediary to access surplus lines carriers — but the client relationship always stays with the retail broker.

The brokers profiled below are all retail operations, selected based on:

- US market presence and geographic reach

- Carrier access across standard and surplus lines markets

- Demonstrated ability to handle complex or non-standard commercial risks

Top Retail Insurance Brokers in the USA

The five brokers below were chosen based on market scale, carrier network depth, industry expertise, and ability to serve diverse commercial risks — from straightforward BOP policies to complex, hard-to-place operations.

Marsh McLennan

Marsh McLennan is the largest insurance broker in the US by a wide margin. Its brokerage arm, Marsh, generated $12.67 billion in 2024 US brokerage revenue and serves multinational corporations, mid-market companies, and virtually every industry sector operating in the country.

What separates Marsh from other large brokers is the depth of its industry verticals. The firm maintains dedicated practice groups for energy, healthcare, financial institutions, construction, and real estate — each with specialized underwriting relationships and risk analytics capabilities that allow large clients to model exposure before a loss occurs, rather than scrambling to respond after one.

| Category | Details |

|---|---|

| Specialty / Focus Areas | Commercial property, casualty, cyber, professional liability, and specialty lines across energy, healthcare, and financial services |

| Carrier Access / Market Reach | Hundreds of global and domestic admitted and non-admitted carriers; operations in 130+ countries |

| Best For | Large enterprises and multinationals with complex, multi-line coverage needs |

Aon

Aon ranks second among US brokers and brings a distinctly analytics-led approach to commercial insurance. Headquartered in Dublin, Ireland, Aon generated $15.7 billion in total 2024 revenue, with $7.7 billion coming from US operations.

The firm's biggest differentiator is its Risk Analyzer suite, launched in 2024, which gives risk managers quantified, board-ready modeling for cyber, D&O, property, and health risks. For organizations where insurance decisions are driven by data rather than gut feel — and where the CFO wants numbers, not narratives — Aon's analytics infrastructure is a meaningful operational advantage.

| Category | Details |

|---|---|

| Specialty / Focus Areas | Management liability, cyber, workers' compensation, employee benefits, and global specialty programs |

| Carrier Access / Market Reach | Broad access to global markets including Lloyd's of London; clients in 120+ countries |

| Best For | Mid-to-large corporations seeking data-backed risk strategy alongside traditional brokerage services |

Arthur J. Gallagher & Co.

Gallagher is the third-largest US broker by revenue — $7.09 billion in 2024 US brokerage revenue — and has built much of that position through acquisitions. The firm closed 10 acquisitions in Q1 2025 alone, a strategy that continuously expands its regional footprint and niche industry access.

The practical benefit for buyers: Gallagher's acquisition model means the firm often has a local office with deep industry expertise in education, agribusiness, non-profits, and hospitality — staffed by specialists, not generalists applying national templates. Its decentralized structure lets specialty knowledge be deployed regionally, which is a real advantage for mid-market businesses that don't fit the multinational mold.

| Category | Details |

|---|---|

| Specialty / Focus Areas | Construction, healthcare, real estate, hospitality, education, social services, and non-profit programs |

| Carrier Access / Market Reach | All 50 US states; 900+ offices globally; strong admitted and E&S market relationships |

| Best For | Small to mid-sized businesses needing industry-specific programs and local broker relationships |

Hub International

Hub International operates 500+ offices across the US and Canada, making it one of the largest broker networks on the continent. The firm has grown aggressively through acquisitions and now serves both personal lines clients and a wide range of commercial accounts.

Hub's commercial offering is broad, covering transportation, construction, environmental liability, and professional liability. The firm has invested in specialty practices that give it real placement depth in areas where many mid-market brokers fall short — particularly transportation risks and environmental exposures, which can be difficult to place cleanly through generalist channels.

| Category | Details |

|---|---|

| Specialty / Focus Areas | Transportation, construction, environmental liability, professional liability, and high-net-worth personal lines |

| Carrier Access / Market Reach | 500+ offices across North America; major US markets covered |

| Best For | Mid-market businesses seeking broad commercial coverage with strong regional service teams |

Soma

Soma is built for a specific problem: businesses with complex, non-standard, or hard-to-insure operations that generalist brokers either decline or handle poorly.

Where large brokers excel at multinational programs and data analytics, Soma's focus is narrower and more operational — getting complex commercial risks quoted and bound fast, without the weeks of delays that plague businesses with unusual exposures.

The firm's team has processed thousands of businesses across trucking, construction, healthcare, technology, hospitality, security agencies, and manufacturing. One application generates industry-specific coverage options across their entire carrier network, which includes Chubb, Markel, Liberty Mutual, Kinsale, Nationwide, and hundreds of additional partners.

Soma's core specialty areas include:

- Security guard agencies (armed and unarmed, including firms with prior claims)

- Trucking operations (new ventures, drivers with violations, hazmat haulers)

- Construction programs (GCs, subcontractors, wrap-up insurance)

- Hospitality and liquor liability (late-night venues, high-occupancy spaces standard brokers turn away)

These are the risk profiles most standard brokers decline to place — and the ones Soma is specifically built to handle.

| Category | Details |

|---|---|

| Specialty / Focus Areas | Complex and hard-to-insure businesses across tech, retail, finance, trucking, manufacturing, healthcare, construction, and hospitality |

| Carrier Access / Market Reach | Hundreds of carrier partners including Chubb, Markel, Liberty Mutual, Kinsale, and Nationwide; US-focused |

| Best For | Complex or hard-to-place risks requiring fast turnaround, industry-specific customization, and expert placement |

How We Chose the Best Retail Insurance Brokers

The brokers on this list weren't selected by brand recognition or advertising spend. Each was evaluated against criteria that actually predict outcomes for commercial buyers:

- Carrier network depth: Access to both admitted and non-admitted (E&S) markets matters. With surplus lines premiums at $131 billion — now 12% of the US P&C market — a broker without credible E&S access can't compete for anything beyond straightforward accounts.

- Industry specialization: Generic brokerage produces generic coverage. Brokers with dedicated industry practices negotiate better terms, know which exclusions to push back on, and understand the operational nuances underwriters actually care about.

- Complex risk capability: The most common mistake buyers make is choosing a broker by name, then discovering mid-placement that the firm can't handle their actual risk profile. For construction, trucking, healthcare, and manufacturing, non-standard market relationships matter more than revenue ranking.

- Operational speed: Slow quote turnarounds cause real problems — delayed project starts, coverage gaps at renewal, lost revenue. Speed is a legitimate differentiator, not a convenience feature.

The right broker for a Fortune 500 multinational differs entirely from the right broker for a 40-truck regional fleet or a security agency with armed guards. The brokers below were chosen because their capabilities match specific buyer profiles — not because of name recognition.

Conclusion

Choosing a retail insurance broker shapes what gets covered, what gets excluded, and how fast your business can respond when something goes wrong.

The brokers on this list cover a genuine range of needs:

- Marsh and Aon — large, complex, data-driven programs

- Gallagher and Hub — mid-market businesses that value regional expertise and broad coverage

- Soma — operations with hard-to-place risks where speed and specialist market access matter

Ask any broker you evaluate whether they can grow with you. As your operations expand, revenue increases, or risk profile shifts, your broker needs to keep pace — with the carrier relationships, industry knowledge, and capacity to handle what comes next.

For businesses with complex or non-standard operations that have been declined elsewhere — or simply want coverage placed fast without weeks of chasing — Soma's industry-specific approach delivers. One application reaches hundreds of carrier partners, and Soma's team has placed thousands of businesses across exactly these kinds of risks. Get a quote now or reach out to Soma's Risk Management Team directly.

Frequently Asked Questions

What is a retail insurance broker?

A retail insurance broker is a licensed professional who works directly with businesses or individuals to identify and place the most appropriate insurance coverage. Unlike agents, brokers represent the client's interests rather than any single carrier — meaning they can shop across multiple insurers to find the best fit.

What is the difference between a retail and wholesale insurance broker?

Retail brokers work face-to-face with end clients (businesses and individuals) to place coverage. Wholesale brokers act as intermediaries between retail brokers and specialty or surplus lines carriers. End clients typically only interact with retail brokers — the wholesale layer operates behind the scenes when a risk needs non-standard placement.

How do retail insurance brokers get paid?

Retail brokers are primarily compensated through commissions paid by the insurance carrier upon policy placement. Some brokers also charge advisory or broker fees for complex placements. Both compensation types are disclosed to the client before binding.

Do I need a retail broker if I already work with an insurance agent?

Agents represent specific carriers and can only offer that carrier's products. Brokers work independently across multiple carriers. For complex, multi-line, or hard-to-place risks, a broker's wider market access usually means better coverage terms and more competitive pricing.

What types of businesses benefit most from working with a retail insurance broker?

Businesses with complex operations, regulated industries, or hard-to-place risks — construction, trucking, healthcare, technology, security, and manufacturing — benefit most. Brokers access specialty and non-admitted markets that standard agents cannot reach — often the only path to getting coverage placed at all.

How do I evaluate the quality of a retail insurance broker?

Key factors to assess:

- Carrier network breadth (admitted and E&S markets)

- Industry-specific expertise in your sector

- Quote turnaround speed and responsiveness

- Claims support track record

- Direct experience with businesses similar to yours in size and risk complexity

Brand name alone is not a reliable quality indicator.