According to BLS data, manufacturing recorded 332,600 nonfatal workplace injuries in 2024 alone — a rate of 2.7 cases per 100 full-time workers. And that's just one exposure. Add product liability, equipment failure, supply chain disruption, and a growing cyber threat, and the stakes of getting insurance wrong become very clear.

Choosing the wrong carrier doesn't just mean paying too much. It means finding coverage gaps at the worst possible moment — when a machine fails mid-run, a product is recalled, or a worker is injured on the floor.

This article covers the top insurance companies for manufacturers in 2026, the coverage types every operation needs, and how to evaluate the right carrier fit for your specific manufacturing profile.

TL;DR

- Manufacturers face layered risks — equipment failure, product defects, worker injuries, and goods in transit — that standard business policies don't fully address

- The top carriers for manufacturers in 2026 are Chubb, The Hartford, Liberty Mutual, Markel, and Nationwide, each suited to different manufacturing profiles

- Financial strength (AM Best ratings), manufacturing-specific coverage depth, and claims experience matter more than brand name or premium price

- Core coverage needs include general liability with product liability, workers' comp, commercial property, equipment breakdown, and inland marine

- A broker with access to multiple specialized carriers, like Soma, lets manufacturers compare competing quotes through a single application

Why Manufacturers Need Specialized Insurance Coverage

Standard commercial policies are built around common business risks. Manufacturing is not a common business environment.

A typical production operation combines several risk categories simultaneously:

- High-value machinery that can fail without warning, halting production and triggering significant replacement or repair costs

- Large physical workforces in environments with real injury exposure — OSHA compliance obligations, workers' comp claims, and return-to-work programs

- Goods in transit between suppliers, facilities, and customers — often uninsured under standard property forms

- Product liability exposure that extends years beyond the sale date, covering defects in completed operations

- Contractual obligations to buyers, distributors, and retailers that often require specific coverage types and minimum limits

Those risks are only part of the picture. OSHA standards, EPA requirements, and product safety laws add a compliance layer that standard commercial policies aren't built to address — manufacturers need programs structured around those obligations, not ones that treat them as an afterthought.

Few carriers underwrite manufacturing well. The ones that do are profiled below.

Top Insurance Companies for Manufacturers in 2026

Each carrier below was selected based on manufacturing-specific coverage availability, AM Best financial strength ratings, claims handling reputation for industrial accounts, and the ability to cover complex or specialty manufacturing operations across the U.S.

Chubb

Chubb is the go-to carrier for large-scale or specialty manufacturing operations that need high limits and genuinely customized policy forms. It serves manufacturers across industrial equipment, chemicals, food processing, and consumer goods — with underwriting teams dedicated to complex, high-value industrial accounts. Its distinguishing edge is a willingness to take on large-limit risks that standard markets decline, backed by one of the strongest financial ratings in commercial insurance.

| Detail | Info |

|---|---|

| Best For | Large-scale, complex, or specialty manufacturers needing high-limit coverage and refined policy forms |

| Key Coverages | Product liability, commercial property, equipment breakdown, workers' comp, commercial umbrella, cyber liability |

| AM Best Rating | A++ (Superior) |

The Hartford

Founded in 1810, The Hartford brings over two centuries of commercial insurance experience — and one of the strongest workers' compensation programs in the industry. For manufacturers prioritizing workers' comp quality and bundled coverage, it's a natural starting point.

The Hartford differentiates through dedicated risk engineering resources: workplace safety tools and loss-control services specifically designed for production environments. These resources help reduce workers' comp claims frequency, which translates directly to lower long-term premiums.

| Detail | Info |

|---|---|

| Best For | Small-to-mid-sized manufacturers prioritizing workers' comp and bundled coverage with strong service support |

| Key Coverages | Workers' compensation, BOP, general liability, product liability, commercial property, business interruption |

| AM Best Rating | A+ (Superior) |

Liberty Mutual

Liberty Mutual is built for mid-market manufacturers operating across multiple facilities, running commercial fleets, and managing sizable workforces. Its commercial lines coverage is broad and scalable — practical for operations that are actively growing production capacity.

Its SafetyNet platform provides risk control tools and training resources across safety research, self-assessment, regulatory guidance, and return-to-work programs. For manufacturers managing OSHA compliance alongside claims costs, that's a meaningful operational advantage.

| Detail | Info |

|---|---|

| Best For | Mid-market manufacturers with multi-location operations, fleet vehicles, or production growth plans |

| Key Coverages | General liability, commercial property, workers' comp, commercial auto, product liability, umbrella |

| AM Best Rating | A (Excellent) |

Markel

Markel writes manufacturing risks that standard markets won't touch. For niche or high-risk operations — specialty chemical manufacturers, highly automated facilities, life sciences production — it builds coverage structures from the ground up rather than forcing unusual risks into generic forms.

That flexibility makes Markel one of the few realistic options for emerging or unconventional manufacturing businesses that standard carriers routinely decline.

| Detail | Info |

|---|---|

| Best For | Specialty, niche, or hard-to-insure manufacturers that standard markets decline or under-price |

| Key Coverages | Specialty product liability, professional liability, inland marine, commercial property, excess liability |

| AM Best Rating | A (Excellent) |

Nationwide

Nationwide is a practical choice for small-to-mid-sized manufacturers that want solid, accessible coverage without navigating large-market underwriting complexity. Its BOP offerings bundle core coverages cleanly, and its independent agent network makes it easy to manage across multiple states.

Its agent network spans all 50 states, so manufacturers operating across state lines can manage most of their core coverage through a single relationship without coordinating multiple regional carriers.

| Detail | Info |

|---|---|

| Best For | Small-to-mid manufacturers seeking accessible bundled coverage with competitive pricing |

| Key Coverages | BOP, workers' compensation, general liability, commercial auto, cyber liability |

| AM Best Rating | A (Excellent) |

Key Coverage Types Every Manufacturer Should Have

The Baseline Stack

Three coverage types are non-negotiable for any manufacturing operation, regardless of size or product type:

- General liability with product liability — covers bodily injury and property damage claims, including completed operations (defects that cause harm after the product leaves your facility)

- Commercial property — covers buildings, machinery, inventory, and equipment against fire, theft, and physical damage

- Workers' compensation — required by law in most states; covers medical expenses and lost wages for employees injured on the job

These three form the floor. The gaps start above them.

Manufacturing-Specific Coverages That Are Often Missed

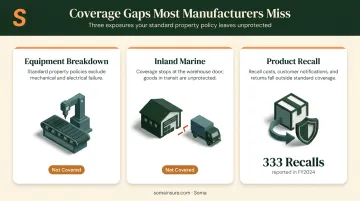

Standard property and liability policies leave significant gaps for manufacturing operations. Three coverage types consistently fall through:

- Equipment breakdown — standard commercial property policies explicitly exclude sudden mechanical or electrical failure. If a conveyor system or CNC machine fails mid-production run, this coverage responds when your property policy won't.

- Inland marine — covers raw materials and finished goods in transit between facilities or to customers. Most manufacturers don't realize their standard property policy stops at the warehouse door.

- Product recall — covers the direct costs of withdrawing a defective product from market. The CPSC completed 333 voluntary recalls covering 153 million consumer product units in FY2024 alone — an exposure that's especially critical for food, pharmaceutical, and consumer goods manufacturers.

The Cyber Threat Manufacturers Can't Ignore

According to IBM's 2026 X-Force Threat Intelligence Index, manufacturing was the most targeted industry for cyberattacks in 2025, accounting for 27.7% of all incidents — holding the top spot for the fifth consecutive year.

As production systems become increasingly connected — IoT-enabled equipment, automated supply chains, ERP integrations — ransomware attacks can shut down physical production, not just IT systems. Cyber liability coverage is no longer optional for manufacturers with networked operations.

How We Chose the Best Insurance Companies for Manufacturers

Brand recognition doesn't equal manufacturing expertise. Several of the largest insurers by market share have limited appetite or coverage depth for manufacturing-specific risks. The evaluation for this list focused on three factors:

- AM Best financial strength — all five carriers are rated A or above, providing confidence in their ability to pay complex claims

- Demonstrated underwriting capacity for manufacturing — specifically across product liability, equipment breakdown, inland marine, and workers' comp for production environments

- Manufacturing-specific policy forms — carriers needed to offer endorsements and coverage structures that match actual manufacturing exposures, not generic commercial adaptations

One mistake manufacturers make consistently: choosing the cheapest quote without verifying the policy covers all three critical areas:

- Completed operations coverage

- Product liability with adequate limits

- Equipment breakdown

These are where stripped-down policies create serious gaps at claim time. Avoiding those gaps starts with working with a broker that maintains active relationships with specialized carriers. Soma partners with Chubb, Markel, and Nationwide for manufacturing accounts specifically — carriers with policy forms designed for production operations. Manufacturers can receive competing quotes from multiple carriers through a single application.

Soma's brokers work across SIC codes and regularly place manufacturing risks that standard markets decline — a practical advantage for operations in niche categories or with difficult risk profiles.

Conclusion

The best insurance company for a manufacturer isn't the largest or the cheapest. It's the one that understands the specific production environment, offers coverage forms designed for manufacturing exposures, and has the financial strength to pay when things go wrong — whether that's a product defect claim, a machinery failure, or a worker injury on the production floor.

When evaluating carriers at renewal, look beyond premium. The right questions to ask:

- Does the policy cover your specific product liability and machinery exposures?

- How does the carrier handle claims for industrial accounts?

- Is risk engineering support included?

- Can the policy scale as you add facilities or product lines?

Manufacturers with complex risks or hard-to-insure operations can work with a broker who already has relationships with the carriers built for those accounts. Soma places coverage for manufacturing businesses across all risk profiles — with direct access to Chubb, Markel, Nationwide, and a broader carrier network. Get a quote and see what the right coverage looks like for your operation.

Frequently Asked Questions

What are the big 5 insurance companies?

According to III data on 2024 direct premiums written, the top five U.S. property/casualty groups are State Farm, Progressive, Berkshire Hathaway, Allstate, and Liberty Mutual. For manufacturers, overall market size matters less than financial strength ratings and demonstrated expertise in underwriting production operations.

What is the 80% rule for insurance?

The 80% rule (coinsurance) requires a commercial property policy to cover at least 80% of the property's full replacement value to receive full claim reimbursement. Manufacturers face particular risk here — production equipment and facilities are frequently undervalued at inception, which can result in significantly reduced payouts at claim time.

What types of insurance do manufacturers typically need?

The core stack includes general liability (with product liability and completed operations), workers' compensation, commercial property, equipment breakdown, and inland marine for goods in transit. The exact mix depends on manufacturing type, workforce size, and whether products are sold to consumers or commercial buyers.

How much does manufacturing insurance cost?

Costs vary by sub-sector, revenue, workforce size, and claims history. Insureon's 2025 platform data reports average general liability costs around $600/year for small manufacturers, BOP coverage averaging $1,517/year, and workers' compensation averaging $1,852/year — though mid-sized or complex operations will differ substantially.

Is product liability insurance mandatory for manufacturers?

No federal law mandates it, but retailers, distributors, and large commercial buyers routinely require product liability coverage as a supplier condition. Without it, a single defect claim can expose a manufacturer to uninsured losses that threaten the business entirely.

Can small manufacturers get the same quality coverage as large ones?

Yes — small manufacturers can access the same carrier quality and coverage types, but may need a specialized broker to reach admitted and surplus lines markets with appetite for smaller or niche operations. Carriers like Markel are specifically designed for small-batch and mid-size manufacturers that standard markets underserve.