That scenario plays out across manufacturing facilities constantly. According to Siemens' 2024 True Cost of Downtime report, plants average 326 hours of unplanned downtime annually — and in automotive manufacturing, a single idle production line costs $2.3 million per hour.

This guide covers what equipment breakdown insurance is, what it covers for manufacturers, where commercial property insurance falls short, what drives costs, and how to get the right policy.

TL;DR

- Equipment breakdown insurance covers sudden mechanical and electrical failures that standard commercial property policies exclude

- Covered equipment includes CNC machines, industrial robots, boilers, compressors, conveyors, and process control systems

- Payouts cover repair or replacement costs, lost production income, extra expenses, and spoilage of perishable goods

- Premiums depend on total equipment value, equipment types, facility size, and claims history

- You can add coverage as a standalone policy or as an endorsement to an existing commercial property policy or BOP

What Is Equipment Breakdown Insurance for Manufacturers?

Equipment breakdown insurance pays for losses caused by sudden, accidental failures of machinery and equipment — specifically damage originating from internal forces: a blown motor, a cracked pressure valve, an electrical short, a mechanical failure under load.

What it doesn't cover is damage from external events like fire, windstorm, or flooding. Those belong to commercial property insurance. The distinction between internal and external cause is the entire basis for why these two policies exist alongside each other.

From "Boiler and Machinery" to Modern Coverage

The policy has roots in the 1860s. Hartford Steam Boiler Inspection and Insurance Company was founded on June 30, 1866, after boiler explosions were occurring at nearly one every four days across industrial America. The original model paired mandatory inspections with insurance — the inspection incentivized safety; the policy covered the losses that slipped through.

That original "Boiler and Machinery" (BM) coverage gradually expanded over a century and a half. Today's equipment breakdown policies, as IRMI defines them, cover "mechanical or electrical breakdown of nearly any type of equipment" — a significantly broader scope than the pressure-vessel focus of traditional BM coverage. Modern manufacturing facilities rely on far more than boilers. Today's covered equipment now includes:

- Programmable logic controllers (PLCs) and SCADA systems

- Industrial robotics and CNC machinery

- Precision electrical infrastructure and motor control centers

- Refrigeration, HVAC, and compressed air systems

That expanded scope is why the policy name changed — and why manufacturers can't afford to evaluate it only through the lens of traditional boiler coverage.

What Does Equipment Breakdown Insurance Cover for Manufacturers?

The Five Categories of Covered Equipment

Equipment breakdown policies organize coverage around five equipment types. All five are directly relevant to manufacturing operations:

- Mechanical — motors, engines, hydraulic presses, conveyor systems, production line machinery

- Electrical — transformers, electrical panels, control systems, power distribution equipment

- Computers and communications — PLCs, SCADA systems, CNC machine controllers, industrial automation systems

- Boilers and pressure equipment — steam boilers, pressure vessels, autoclaves

- HVAC and refrigeration — industrial chillers, cooling systems, cold storage for food or pharmaceutical manufacturers

Chubb's equipment breakdown coverage specifically lists manufacturing examples including CNC turret lathes, robotically controlled welding lines, and 400-ton stamping presses — coverage that spans the full range of production environments, from light fabrication to heavy industrial.

Financial Coverages Beyond Repair Costs

Repair or replacement is only one part of the payout. A well-structured policy also covers:

- Business interruption — lost production income during the shutdown period

- Extra expense — costs to rent replacement equipment, outsource production, or expedite repairs to minimize downtime

- Spoilage — perishable raw materials or finished goods destroyed due to refrigeration failure (critical for food processors and pharmaceutical manufacturers)

- Consequential property damage — if a boiler explosion damages an adjacent wall or production area, the policy covers both the boiler and the structural repair

Some policies also extend to utility interruption: if a breakdown at your local power utility disrupts your facility, coverage can apply to income loss and spoilage caused by that third-party failure — not just failures of equipment you own.

Compliance Benefit: Required Inspections

In many states, insurers offering equipment breakdown coverage also perform required annual inspections of boilers and pressure vessels. HSB, for example, schedules and performs certificate inspections per state and municipal jurisdictional requirements. For manufacturers running high-pressure steam systems, that means fewer compliance headaches — the insurer handles the inspection scheduling, documentation, and certificate filing that regulators require.

Covered Manufacturing Equipment: A Practical List

| Equipment Type | Examples |

|---|---|

| Machining centers | CNC mills, lathes, turret centers |

| Forming equipment | Hydraulic presses, injection molding machines, stamping presses |

| Industrial robots | Robotic arms, automated welding lines |

| Material handling | Conveyors, automated storage/retrieval systems |

| Compressed air systems | Industrial air compressors, pneumatic equipment |

| Power systems | Electrical switchgear, transformers, distribution panels |

| Boilers and pressure equipment | Steam boilers, pressure vessels, autoclaves |

| Refrigeration and cooling | Industrial chillers, cold storage systems |

| Process control | PLCs, SCADA systems, DCS controllers |

| Packaging and labeling | Automated packaging lines, labeling machinery |

What Equipment Breakdown Insurance Does NOT Cover

What the Policy Excludes

Understanding exclusions matters as much as understanding coverage. Equipment breakdown policies are not maintenance coverage. Per IRMI's expert commentary on the policy form, standard exclusions include:

- Gradual wear and tear, rust, and corrosion — conditions insurers expect you to prevent through regular upkeep

- Deferred or faulty maintenance that leads to a breakdown

- Fire, flood, windstorm, and hail — these belong on your property policy, not here

- Software failures and cyber incidents, which require a separate cyber liability policy (Nationwide explicitly excludes software from equipment breakdown coverage)

- Scheduled overhauls, filter replacements, and other routine maintenance costs — these are operational expenses, not insurable losses

The policy responds to sudden, unplanned failures. If the condition was developing for weeks before it caused a breakdown, that's a maintenance problem — not a covered loss.

The Pre-Existing and Gradual Deterioration Problem

If a machine was already failing before your policy started — or its failure resulted from a condition that had been deteriorating for months — coverage is unlikely to apply. Insurers treat gradual deterioration as a maintenance obligation you were expected to address.

This is also why carriers ask about equipment age and maintenance records at underwriting. A machine with a spotty service history raises questions about whether a future failure will qualify as sudden and accidental or get denied as a foreseeable result of neglect.

Why Manufacturers Can't Rely on Commercial Property Insurance Alone

The Coverage Gap That Catches Manufacturers Off Guard

Commercial property insurance covers damage caused by external perils — fire, hail, theft, vandalism. The ISO Causes of Loss – Special Form (CP 10 30 09 17) explicitly excludes:

- Mechanical breakdown, including rupture or bursting caused by centrifugal force

- Artificially generated electrical or electromagnetic energy that damages electrical equipment or systems

- Explosion of steam boilers, steam pipes, or steam turbines owned or controlled by the insured

This means a fire that destroys your production line is a property claim. A power surge that burns out the electrical panel controlling that same line is not — that's an equipment breakdown claim. Without the right policy, the second loss comes entirely out of pocket.

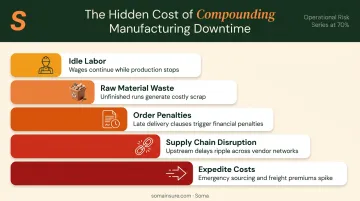

The Compounding Costs of Manufacturing Downtime

Repair costs can be the smallest line item in a major equipment loss. When a machine goes down in a manufacturing environment, the financial damage compounds quickly:

- Idle labor — workers continue drawing wages while production stops

- Raw material waste — work-in-process may be scrapped

- Order penalties — customer contracts often include late-delivery penalties

- Supply chain disruption — downstream customers and relationships take hits that don't show up on a repair invoice

- Expedite costs — rushing parts, outsourcing production, or paying overtime to catch up

The business interruption component of an equipment breakdown policy is specifically designed to address these cascading costs.

Equipment Warranties Don't Fill the Gap

Some manufacturers assume their equipment warranties cover the gap. That assumption gets expensive fast. Haas Automation's CNC limited warranty, for example, explicitly excludes "loss of profits, lost data, loss of revenue, loss of use, and cost of down time" and caps the manufacturer's liability at repair or replacement only. It also voids coverage for mishandling, improper maintenance, or operator error.

Warranties expire, and they cover defects — not power events, operational failures, or the cascading business losses that follow. Equipment breakdown insurance picks up precisely where warranties stop.

How Much Does Equipment Breakdown Insurance Cost for Manufacturers?

Key Pricing Factors

Premium pricing for manufacturing operations depends on several variables underwriters evaluate together:

- Total equipment replacement value — the primary driver; higher-value equipment inventories mean higher premiums

- Equipment types — high-pressure boilers and complex robotics carry more risk than standard HVAC or conveyors

- Facility size and operational complexity — larger facilities with more interconnected systems have broader exposure

- Claims history — prior breakdown losses influence pricing directly

Standalone Policy vs. Endorsement

Manufacturers can structure equipment breakdown coverage two ways:

- Standalone policy — a separate monoline policy, typically used when equipment values are large or the operation's complexity warrants dedicated coverage

- Endorsement to a commercial property policy or BOP — adding equipment breakdown coverage to an existing policy is generally more cost-effective and simplifies claims coordination

For most small-to-mid-size manufacturers, the endorsement route is more economical. For operations with specialized or high-value equipment, a standalone policy may offer higher limits and more flexibility.

Deductibles and the Coinsurance Requirement

Higher deductibles reduce premiums, but manufacturers should weigh that trade-off against their ability to absorb out-of-pocket repair costs on expensive machinery. A $50,000 compressor repair hits very differently with a $1,000 deductible versus a $10,000 one.

The coinsurance requirement matters just as much. Many commercial policies require manufacturers to carry coverage equal to at least 80% of equipment replacement value. Underinsure your equipment, and the insurer applies a proportional penalty at claims time — you absorb the shortfall.

Per IRMI's analysis of coinsurance in commercial property policies, the recovery ratio is calculated by dividing the carried limit by the minimum required limit, and claims payments are reduced accordingly.

Accurate equipment valuation before binding coverage is what separates a full recovery from a partial one.

How to Get the Right Equipment Breakdown Coverage for Your Manufacturing Operation

What to Bring to the Quoting Process

Manufacturers with complex equipment benefit most from working with a broker who understands industrial risks. Before requesting quotes, gather:

- A current equipment inventory with estimated replacement values (replacement cost, not book value)

- Equipment age and maintenance records

- Existing policy information (commercial property, BOP, or package policy)

- Any history of prior breakdowns or insurance claims

Generic, off-the-shelf policies rarely account for the specific mix of equipment, production dependencies, and operational risks in a manufacturing environment. A broker who understands SIC codes, process equipment, and manufacturing exposures can match your coverage to how your facility actually operates, rather than defaulting to a standard class code that may not reflect your actual risk.

Working with Soma

Soma works with leading carriers — including Chubb, Liberty Mutual, Markel, and Nationwide — and places equipment breakdown coverage as part of comprehensive manufacturing insurance programs. Soma's brokers have experience across manufacturing segments, including complex operations that standard markets decline.

Through a single application, manufacturers can receive industry-specific quotes without waiting weeks for responses. The team analyzes your specific exposures and matches coverage to your production environment — filling gaps that generic policies typically miss.

Frequently Asked Questions

What is covered by equipment breakdown insurance?

Equipment breakdown insurance covers the repair or replacement cost of machinery that suffers a sudden mechanical or electrical failure. Beyond direct equipment damage, the policy also covers business interruption losses, spoilage of perishable goods, and extra expenses incurred to restore operations during the repair period.

Is equipment breakdown insurance worth it for manufacturers?

For manufacturers, it's essential. Production equipment is expensive to replace, downtime carries significant financial consequences, and commercial property insurance specifically excludes the internal failures that cause most equipment losses.

What are the most common causes of equipment breakdowns?

Rough Notes reports that over 50% of equipment breakdown claims stem from power surges affecting circuit boards, drive boards, and sensitive electronic components. Mechanical failures and operator-induced failures make up most of the remainder.

What is the 80% rule in insurance?

The 80% coinsurance rule requires that you carry coverage equal to at least 80% of your equipment's replacement value. If you insure for less than that threshold, the insurer will only pay a proportional share of any claim — you absorb the rest out of pocket. Accurate equipment valuation before binding coverage is critical to avoid this penalty.

Does equipment breakdown insurance cover operator error?

Most equipment breakdown policies cover accidental damage from operator error — such as a worker mis-operating a hydraulic press. The damage must be accidental and sudden, not the result of intentional misuse or deliberate abuse.

Can equipment breakdown insurance be added to a Business Owners Policy?

Yes. Equipment breakdown coverage is commonly available as an endorsement to a BOP or commercial property policy. Adding it this way is typically more cost-effective than purchasing a standalone policy, and it simplifies claims handling since both coverages sit under the same program.