These questions come up constantly, especially for businesses in construction, trucking, hospitality, and manufacturing — industries where claims are a real possibility, not a theoretical one.

This article explains exactly what a CGL deductible is, how it works when a claim hits, how it affects your premium, and how to choose the right amount for your operation.

TL;DR

- A CGL deductible is the fixed dollar amount you pay per covered claim before your insurer pays the remainder

- Many CGL policies offer a $0 deductible ; taking one is optional, and doing so lowers your premium

- Higher deductible = lower premium, but only worthwhile if your cash reserves can absorb it

- The deductible applies per occurrence, not annually so three claims in a year means three separate deductible payments

- A self-insured retention (SIR) differs from a deductible: with an SIR, you fund defense costs yourself before the insurer gets involved

What Is a Deductible in Commercial General Liability Insurance?

As defined by IRMI, a deductible is the amount the insurer deducts from a covered loss before paying out up to policy limits. In the CGL context, it's the fixed dollar amount your business agrees to absorb on each covered claim.

A simple example: A slip-and-fall at your facility results in a $50,000 covered claim. With a $1,000 deductible, your insurer pays $49,000. You pay $1,000.

That mechanic is straightforward. What trips people up is what the deductible doesn't do:

- It does not increase your policy limits

- It does not guarantee coverage — the insurer's adjuster still determines whether the claim qualifies

- It does not apply annually — it triggers per covered claim event

- It does not activate on claims that aren't covered under your policy

The ISO deductible endorsement (form CG 03 00) applies specifically to bodily injury and property damage claims under the CGL coverage part. The deductible only comes into play once coverage is confirmed.

Do All CGL Policies Have a Deductible?

No. Many standard CGL policies are available with a $0 deductible. Insureon notes that deductibles can be set as low as zero for general liability, though the business pays a higher premium as a result.

Taking a deductible is a choice — typically $500, $1,000, or $2,000 — that trades a lower premium for more out-of-pocket exposure per claim.

Businesses in higher-risk categories — construction, hospitality, trucking, security — frequently land in surplus lines or non-standard markets, where this calculation shifts. In those markets:

- Deductible structures vary more widely by carrier and risk class

- Standard $500–$2,000 tiers may not apply

- Your policy declarations page is the only reliable source for what your specific deductible is

If your business operates in one of these categories, verify your declarations page before assuming standard market terms apply.

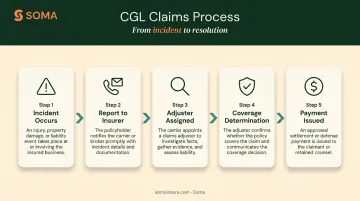

How Does a CGL Deductible Work When a Claim Is Filed?

Here's the sequence, based on how standard CGL claims processing works under ISO CG 00 01 and carrier practice:

- Incident occurs — bodily injury, property damage, or a covered offense takes place

- Report to insurer — you notify your carrier as soon as practicable of an occurrence that may result in a claim

- Adjuster assigned — a claims adjuster investigates what happened, reviews documents, and verifies coverage

- Coverage determination — if the claim qualifies under your policy, the deductible is triggered

- Payment issued — the insurer pays the covered amount minus your deductible; under ISO CG 03 00, the insurer may pay the full loss upfront and bill you for the deductible portion

Under a standard deductible structure, the insurer manages the claim from the start — this is different from a self-insured retention, which is covered in the next section.

That sequence also shapes where judgment calls come into play.

The Small-Claims Decision

When a covered loss is close to your deductible — say a $1,200 claim with a $1,000 deductible — filing may not be the right call. Your insurer only pays $200, but the claim appears in your loss run history.

According to Insureon, loss runs (periodic claim reports maintained by insurers) can influence future premiums and your ability to switch carriers. A claim that generates almost no insurer payout isn't necessarily worth the long-term impact on your record.

Deductibles and Policy Limits

The deductible does not add to your coverage. With a $1,000,000 per-occurrence limit and a $1,000 deductible, the maximum insurer payout is still $1,000,000. Your deductible comes off the top of what they pay — it doesn't extend the ceiling.

IRMI confirms that CGL declarations fix the most the insurer will pay regardless of the number of claims, insureds, or parties involved.

How CGL Deductibles Affect Your Premium

Higher deductible = lower premium. By taking on more of each loss yourself, you reduce the insurer's financial exposure — and they price that reduction into your rate.

A few concrete data points on this:

- Hiscox notes that a policy with a $5,000 deductible will generally cost less than the same policy with a $500 deductible

- Insureon's data shows a $1M general liability policy can range from roughly $260 to over $3,000 annually, with industry and deductible selection among the key variables

- For context: contractors average around $82/month, general contractors around $142/month, and restaurants around $141/month — all figures that shift based on deductible chosen

The practical caveat: No published actuarial study provides a universal savings figure for moving between deductible tiers, so use carrier-specific quotes as estimates, not guarantees. More importantly, premium savings only matter if your business can absorb the higher deductible out of cash reserves. A lower monthly premium means little if one claim drains your operating funds.

CGL Deductible vs. Self-Insured Retention (SIR)

These two terms get used interchangeably, but they work very differently in practice.

| Feature | Standard Deductible | Self-Insured Retention (SIR) |

|---|---|---|

| Who manages the claim first | Insurer | Insured |

| Who funds the first layer | Insurer pays, then bills insured | Insured pays directly until retention is met |

| Defense costs included | Generally not included in deductible | Often included in SIR amount |

| When insurer gets involved | From day one | Only after SIR is exhausted |

| Common policy types | Standard CGL | Professional liability, cyber, higher-limit CGL |

IRMI draws the distinction clearly: under a deductible, the insurer pays every loss and is reimbursed by the insured up to the deductible amount. Under a SIR, the insured funds and manages all expenses — including defense — until the retention is exceeded. Only then does the insurer step in.

For most small-to-mid-size businesses, this distinction surfaces most often on professional liability, cyber liability, and higher-limit umbrella policies — though it can appear on complex CGL programs as well.

If you're unsure which structure your policy uses, check with your broker before a claim arrives — under a SIR, you may owe tens of thousands in upfront defense costs before your insurer gets involved.

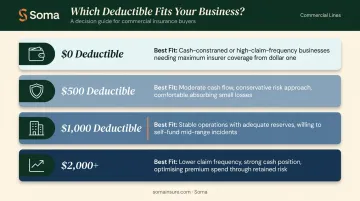

How to Choose the Right CGL Deductible for Your Business

Start with one question: how much can your business pay out of pocket without disrupting operations?

That number is your ceiling. Your deductible should never exceed what your cash reserves can comfortably absorb. From there, two factors shape the decision.

Claims frequency matters more than most business owners expect. Construction sites, restaurants, and facilities with heavy foot traffic face more frequent covered claims — a lower deductible keeps each event manageable. Businesses with lower claim frequency and stronger cash flow may find a higher deductible worthwhile for the premium savings.

Here's how different deductible levels typically align with business profile:

| Deductible | Best Fit |

|---|---|

| $0 | Cash-constrained businesses; high-frequency-risk operations; newer businesses building reserves |

| $500 | Moderate cash flow; some exposure; conservative approach to out-of-pocket risk |

| $1,000 | Stable operations with adequate reserves; willing to absorb small claims to reduce premium |

| $2,000+ | Lower claim frequency; strong cash position; prioritizing premium reduction |

One practical step: run the same deductible options across multiple carriers before deciding. Because premiums respond differently to deductible changes depending on the carrier and your risk profile, comparing quotes side by side shows you where the savings are actually meaningful. Soma's access to hundreds of carrier partners — including Kinsale, Markel, and Chubb — means you can see those comparisons across standard and surplus lines markets, not just whatever a single carrier offers.

Frequently Asked Questions

Is there a deductible on commercial general liability insurance policies?

Not always. Many CGL policies offer a $0 deductible, though the premium will be higher. Businesses can elect a deductible (commonly $500 to $2,000) to reduce their premium. In some surplus lines or higher-risk markets, carriers may require a minimum deductible.

How do I choose the right deductible for commercial general liability insurance?

Base your decision on available cash reserves, your industry's claims frequency, and how much premium savings each tier generates. A licensed broker can model different scenarios and show you the actual trade-off for your specific operation and risk profile.

How much does $1,000,000 commercial general liability insurance cost?

According to Insureon's marketplace data, a $1M general liability policy ranges from roughly $260 to over $3,000 annually for small businesses, averaging around $45/month. Costs vary by industry: contractors average $82/month, restaurants $141/month. A higher deductible generally reduces these figures.

What is the difference between a deductible and a self-insured retention (SIR)?

With a deductible, the insurer manages the claim from day one and bills you for your share. With a SIR, you fund and manage all costs, including defense, until the retention is exhausted. SIRs are more common on professional liability, cyber, and higher-limit policies.

Does a higher deductible lower my CGL insurance premium?

Yes. A higher deductible shifts more financial risk to you, which reduces the insurer's exposure and lowers your premium. The savings are only valuable if your business can actually afford the higher out-of-pocket amount when a claim occurs.

What happens if a claim is less than my CGL deductible?

You pay the full amount yourself and the insurer pays nothing. Filing may still hurt you: the claim appears in your loss run history and can affect future premiums or your ability to switch carriers, with no offsetting payout to show for it.