Introduction

Many business owners use "professional liability" and "malpractice insurance" interchangeably. That's understandable — both policies protect professionals against claims tied to their work. But assuming they're the same thing, or that one policy covers everything, can leave serious gaps when a claim actually lands.

The type of harm alleged determines which policy responds. A claim centered on financial loss from bad advice triggers professional liability. A claim involving patient injury triggers malpractice. Pick the wrong coverage — or rely on general liability alone — and your legal defense costs and any settlement land directly out of pocket.

According to the AMA's 2026 Policy Research Perspectives, 28.7% of U.S. physicians have been sued at least once during their career, and 1.8% faced a new claim in the prior year alone. For non-clinical professionals, the exposure is just as real: Hiscox reports that 77% of U.S. small businesses are underinsured.

This guide breaks down both policies clearly: what each covers, who needs it, and how to choose the right one for your business.

TL;DR

- Malpractice insurance is a specialized subset of professional liability — not a separate category

- Professional liability (E&O) covers consultants, accountants, architects, technology firms, and similar service businesses

- Malpractice covers healthcare and legal professionals where errors cause direct physical or legal harm

- Both are typically written on a claims-made basis — policy structure matters as much as coverage type

- Your industry and the type of harm your errors cause clients determines which you need

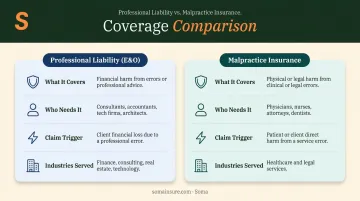

Professional Liability vs. Malpractice Insurance: At a Glance

| Dimension | Professional Liability (E&O) | Malpractice Insurance |

|---|---|---|

| What it covers | Financial harm from errors, omissions, negligent advice, or failure to deliver services | Physical, psychological, or legal harm from clinical or legal professional errors |

| Who needs it | Consultants, tech firms, accountants, architects, engineers, financial advisors, real estate agents | Physicians, surgeons, nurses, dentists, mental health professionals, attorneys |

| Claim trigger | Client suffers financial loss tied to professional's work or advice | Patient/client suffers direct harm from clinical or legal negligence |

| Policy structure | Primarily claims-made; some occurrence-based policies exist | Claims-made (most common) or occurrence-based |

| Common industries | Technology, finance, consulting, construction, real estate, marketing | Healthcare, legal |

| Other names | E&O insurance, errors and omissions insurance | Medical malpractice, legal malpractice |

One important note: these policies aren't mutually exclusive. A healthcare provider who also runs an administrative consulting practice, for example, may need both — malpractice for the clinical side, professional liability for the consulting work.

What Is Professional Liability Insurance?

Professional liability insurance — also called errors and omissions (E&O) insurance — protects professionals against claims that their service, advice, or work product caused a client financial harm. Coverage applies whether or not the professional was actually at fault — a frivolous claim still generates real legal defense costs.

What It Covers

Core coverage areas include:

- Alleged negligence in delivering a professional service

- Errors or omissions in a work product or deliverable

- Failure to meet professional standards or contractual commitments

- Misrepresentation of services or expected outcomes

- Inaccurate advice that causes a client financial loss

Who Needs It

Any profession where a client's financial or business outcome depends on the professional's judgment. That includes consultants, IT firms, accountants, architects, engineers, financial advisors, real estate agents, and marketing agencies. Many are also contractually required to carry E&O coverage before working with certain clients or government entities.

Beyond contract requirements, some states mandate coverage outright:

- Real estate agents in Louisiana, Colorado, Kentucky, Tennessee, and Alaska must carry E&O insurance by law

- Oregon attorneys are required to hold primary malpractice coverage through the state bar's Professional Liability Fund — an example of legal malpractice functioning as a required E&O equivalent

How Claims-Made Coverage Works

Most professional liability policies are written on a claims-made basis, meaning coverage is triggered when the claim is filed — not when the underlying incident occurred. If your policy lapses or is canceled, claims filed afterward aren't covered, even if the work happened while you were insured.

That's why tail coverage (also called an extended reporting period) matters. It allows claims to be reported after a policy ends for incidents that occurred during the policy period. Any professional switching carriers or retiring should understand this mechanic before canceling a claims-made policy.

Professional Liability in Practice

Three scenarios that would trigger professional liability — not malpractice:

- An IT consultant recommends a software platform that fails, resulting in a client's data loss and operational disruption. The client sues for the cost of recovery and lost business.

- An accounting firm makes a tax calculation error that results in an IRS penalty. The client holds the firm responsible for the penalty and associated costs.

- A marketing agency is hired to deliver a lead-generation campaign. The campaign underperforms, and the client claims the agency misrepresented its capabilities.

In each case, the alleged harm is financial — not physical. That's the line that separates professional liability from malpractice.

What Is Malpractice Insurance?

Malpractice insurance is a specialized form of professional liability designed for healthcare providers and attorneys — professions where errors don't just cost clients money, they cause direct physical, psychological, or legal harm. A standard E&O policy won't cover these risks.

What It Covers

Malpractice policies address risks specific to clinical and legal practice:

- Clinical errors, misdiagnosis, and surgical mistakes

- Medication dosage errors or prescribing failures

- Failure to treat or failure to obtain timely consultation

- HIPAA-related claims and medical board proceedings

- Legal malpractice (missed deadlines, procedural errors, conflict of interest)

These claim types don't appear in a standard professional liability form — which is why healthcare and legal professionals need a purpose-built policy.

Who Needs It — and What the Law Requires

Licensed clinical practitioners need malpractice insurance: physicians, surgeons, nurses, nurse practitioners, dentists, physical therapists, and mental health professionals. Several states mandate minimum coverage levels:

- Connecticut: $500,000 per occurrence / $1,500,000 aggregate for physicians providing direct patient care

- Florida: $250,000 per claim / $750,000 aggregate for physicians with hospital privileges or who perform surgery in an ASC

- Massachusetts: Requires doctors to have malpractice coverage; licensed insurers must make it available

Claims-Made vs. Occurrence in Malpractice

Two policy structures exist in the malpractice market:

- Claims-made: The claim must be filed while the policy is active. Tail coverage is required when the policy ends to protect against future claims from that period.

- Occurrence-based: Covers any incident during the policy period, regardless of when the claim is filed later. Rarer and typically more expensive.

Claims-made is the dominant structure in the malpractice market. Physicians changing jobs, retiring, or switching carriers need to arrange tail coverage; without it, incidents from their policy period remain uninsured for any future claims.

Malpractice in Practice

Policy structure matters most when a real claim surfaces. Here are three scenarios that fall squarely under malpractice:

- A surgeon performs a procedure that results in an avoidable complication. The patient files a claim for medical costs and ongoing disability.

- A physician misses a cancer diagnosis, delaying treatment by eight months. The delayed treatment worsens the patient's prognosis.

- A nurse practitioner administers the wrong medication dosage, causing an adverse reaction requiring hospitalization.

The financial scale is significant. A peer-reviewed JAMA Internal Medicine study analyzing NPDB data from 1992–2014 found a mean paid malpractice claim of $329,565, with inflation-adjusted payments rising over time. For high-severity diagnosis-related claims exceeding $1 million, 91% involved patient death or severe injury.

Which Coverage Do You Need?

The answer comes down to one question: what type of harm does your work create?

- Financial harm from advice, errors, or deliverables → Professional liability (E&O)

- Physical, psychological, or legal harm from clinical or legal practice → Malpractice

Coverage by Industry Segment

| Professional Type | Coverage Needed |

|---|---|

| Physicians, surgeons, nurses, dentists | Medical malpractice |

| Attorneys | Legal malpractice |

| Healthcare providers who also consult or run admin practices | Malpractice + professional liability |

| IT consultants, SaaS companies, tech firms | Tech E&O / professional liability |

| Accountants, financial advisors, investment advisors | Professional liability (E&O) |

| Architects, engineers, construction consultants | Professional liability (E&O) |

| Marketing agencies, management consultants | Professional liability (E&O) |

The Coverage Gap That Catches Businesses Off Guard

Many business owners assume their general liability policy handles professional mistakes. It doesn't. General liability covers bodily injury and property damage from everyday operations — a slip-and-fall, accidental property damage, equipment damage to a client's space.

Professional errors, negligent advice, and substandard work are explicitly excluded through the professional services exclusion, a standard carveout in general liability forms.

Without a separate professional liability or malpractice policy, those claims land entirely on the business: legal defense, expert witnesses, settlements.

In healthcare specifically, relying on an employer's group policy without reviewing your individual coverage scope creates real exposure. Common gaps include:

- Group policies that don't transfer after a job change

- Limits that don't match your specialty or practice volume

- Exclusions tied to specific procedures or patient populations

For businesses that sit at industry crossroads — a healthcare tech company, a financial services consultant with clinical advisory clients, or a telehealth platform — determining the right coverage combination requires a closer look at every exposure. Soma works across healthcare, technology, finance, and consulting, placing both professional liability and malpractice coverage through carrier partners including Chubb, Kinsale, Hiscox, Markel, and CRC Group. Soma's Risk Management Team analyzes your specific exposures and matches you to the right policy structure — one application, one conversation, no chasing multiple brokers.

Frequently Asked Questions

Is malpractice insurance the same as professional liability insurance?

No : malpractice is a specific type of professional liability insurance, not a synonym for it. It's purpose-built for healthcare and legal professionals where errors cause direct physical or legal harm, rather than financial harm to a business client.

How much does professional liability insurance cost?

Costs vary by industry, revenue, limits, and claims history. Insureon reports small businesses pay an average of $88/month ($1,051/year), with annual premiums ranging from roughly $400 to $1,800. Higher-risk professions and larger firms pay more.

What are the two types of professional liability insurance?

Claims-made and occurrence-based. Claims-made is far more common: coverage applies when the claim is filed during the active policy period, and tail coverage extends protection after the policy ends. Occurrence-based policies cover any incident that happens during the policy period, regardless of when the claim is filed.

Do I need both professional liability and malpractice insurance?

Most non-clinical businesses only need professional liability (E&O). Healthcare providers who also perform consulting or administrative functions may need both : one policy for the clinical exposure, another for the non-clinical work.

Does general liability insurance cover professional mistakes?

No. General liability covers bodily injury and property damage from business operations, not professional errors or negligent advice.

Is professional liability insurance required by law?

It depends on your state and profession. Real estate agents in several states (Louisiana, Colorado, Kentucky, Tennessee, Alaska) are legally required to carry E&O. Oregon mandates malpractice coverage for all licensed attorneys. Many client contracts also require it regardless of state law.