Introduction

A single client dispute can cost a freelancer thousands in legal fees — with no employer to absorb the hit. A missed deliverable, a campaign that underperformed, code that crashed a production site: any of these can trigger a claim that lands entirely on you.

Professional liability insurance — also called errors and omissions (E&O) insurance — covers you when a client claims your work caused them financial harm, whether through a mistake, an oversight, or failure to meet professional standards.

It's also increasingly a contract requirement. Some corporate clients, including institutions like Cornell University, require independent consultants to carry $1M per claim and $2M aggregate in E&O coverage before work begins.

That context shapes everything about how to shop for this coverage. This guide covers what professional liability insurance is, what it costs, and which providers offer the best options for freelancers in the US.

TL;DR

- E&O insurance covers client claims of negligence, errors, or faulty deliverables — physical injury and property damage fall under separate policies

- Top providers include Hiscox, The Hartford, NEXT Insurance, Thimble, and biBerk — each suited to different needs and budgets

- Independent contractors pay an average of $88/month for professional liability, though costs vary by profession

- Corporate clients increasingly require proof of E&O coverage before signing contracts with freelancers

- A multi-carrier brokerage saves time by running your quote across multiple providers through one application

What Is Professional Liability Insurance for Freelancers?

E&O vs. General Liability

Professional liability insurance (E&O) protects you if a client claims your professional services caused them financial harm — through a mistake, an omission, a missed deadline, or failure to meet a professional standard.

That's a different animal from general liability insurance. General liability covers physical risks: someone gets hurt at your workspace, or property gets damaged. E&O covers abstract, financial risks: the kind that arise when a deliverable goes wrong.

For freelancers who provide consulting, creative work, or any service-based deliverable, general liability alone leaves a real gap. A web designer, for instance, faces almost no bodily injury risk — but faces genuine exposure if a client argues the design led to lost revenue.

What E&O Actually Covers

According to NEXT Insurance, professional liability can help defend against:

- Business errors and professional negligence

- Missed deadlines

- Breach of contract claims

- Professional oversights in delivered work

Real-World Claim Scenarios

Three situations where freelancers typically need E&O coverage:

- Developer error — A freelance developer builds an e-commerce site that crashes during a major sale, and the client sues for lost revenue

- Marketing underperformance — A marketing consultant's campaign produces weak results, and the client demands a refund plus compensation for the budget spent

- Copyright dispute — A freelance designer uses stock elements that turn out to be improperly licensed, triggering an infringement claim against the client who then names the designer

In each case, the exposure is financial, not physical — and general liability wouldn't touch any of it.

Best Professional Liability Insurance Providers for Freelancers

Providers below were evaluated based on financial strength ratings, breadth of coverage, ease of purchase, and suitability for solo and small freelance operations.

Hiscox

Hiscox specializes in small business insurance, with a dedicated professional liability product for freelancers across consulting, IT, marketing, and design. The company carries an AM Best A (Excellent) financial strength rating.

A key differentiator: Hiscox's worldwide coverage clause covers work performed anywhere, as long as legal action is filed in the US, US territories, or Canada. This matters for freelancers with international clients. Policies are available online with a 14-day money-back option.

Note: Hiscox's standard professional liability excludes medical, nursing, legal, and actuarial services unless specifically added via endorsement.

| Category | Details |

|---|---|

| Best For | Freelancers needing global project coverage and fast online purchase |

| Key Policies | Professional liability, general liability, BOP, cyber |

| Notable Limitation | No coverage in Alaska; some professions require endorsement for E&O |

The Hartford

With an AM Best A+ (Superior) rating, The Hartford ranks among the most financially stable providers in this comparison. It offers professional liability alongside a full suite of business coverage, including data breach riders and home-based business policies.

Freelancers operating as LLCs or sole proprietors can bundle E&O with a BOP through The Hartford, which simplifies coverage management. The carrier also maintains a dedicated page for 1099 independent contractors.

| Category | Details |

|---|---|

| Best For | Freelancers prioritizing financial stability and bundled coverage |

| Key Policies | Professional liability, GL, BOP, workers' comp, data breach, commercial umbrella |

| Notable Limitation | Not all business types can quote fully online; no coverage in Alaska or Hawaii |

NEXT Insurance

NEXT Insurance is a digital-first platform backed by Munich Re (ERGO Group), rated AM Best A+ (Superior). The entire process — quote, purchase, and Certificate of Insurance — happens online in minutes.

The unlimited digital COI sharing feature is useful for freelancers who need proof of coverage before a project starts. Certificates are available instantly after purchase, with no back-and-forth required.

| Category | Details |

|---|---|

| Best For | Freelancers who need instant digital coverage with same-day COI access |

| Key Policies | Professional liability, GL, BOP, cyber, workers' comp, commercial auto |

| Notable Limitation | Claims filed online only (no phone option); not available in all states |

Thimble

Thimble's standout feature is flexible policy duration — freelancers can buy coverage by the job, month, or year, making it a practical option for project-based or seasonal work. It operates as a broker rather than a direct insurer.

The underwriting entity, National Specialty Insurance Company, carries an AM Best A (Excellent) rating. Built-in certificate management tools are included at no extra step.

| Category | Details |

|---|---|

| Best For | Freelancers with irregular workloads who need flexible coverage periods |

| Key Policies | Professional liability, GL, BOP, workers' comp, inland marine, cyber, event insurance |

| Notable Limitation | Professional liability not available in Washington or New York; customer support is online-only |

biBerk

Backed by Berkshire Hathaway, biBerk's underwriting entity holds an AM Best A++ (Superior) rating — the highest available. Its direct-to-consumer model removes broker markup, which keeps pricing lean.

Coverage can activate as soon as the next business day, and a COI is available immediately after purchase. Policies typically start around $300/year, making it one of the more accessible entry points for budget-conscious freelancers.

| Category | Details |

|---|---|

| Best For | Solo freelancers seeking affordable, no-frills E&O with fast activation |

| Key Policies | Professional liability, GL, BOP, workers' comp, cyber, umbrella, commercial auto |

| Notable Limitation | Single-carrier platform; less suited for complex or specialized coverage needs |

How We Chose the Best Professional Liability Insurance Providers

Evaluation Criteria

Each provider was assessed across five factors:

- Financial strength — AM Best ratings confirm an insurer's ability to pay claims. Ratings ranged from A (Excellent) for Hiscox and Thimble to A++ (Superior) for biBerk

- Ease of purchase and COI access — Solo freelancers need speed — providers that offer instant online purchase score higher

- Breadth of policy options — Freelancers with multiple exposure types benefit from providers who bundle E&O with cyber or GL

- State and profession availability — Coverage gaps matter; Thimble excludes New York and Washington for professional liability

- Customer experience — General complaint history with state regulators, while full NAIC complaint index scores require a live pull from NAIC's Consumer Insurance Search tool

Common Freelancer Mistakes When Choosing Coverage

Avoid these when shopping:

- Buying GL instead of E&O — General liability doesn't cover professional service errors; many freelancers carry one and think they're fully covered

- Choosing on price alone — A lower premium from a carrier with a weak financial rating is a poor trade-off if a claim gets disputed

- Not checking profession exclusions — Some providers exclude certain professions at the standard policy level; always verify your work type is covered

- Going direct when your situation is complex — Single-insurer platforms like biBerk work well for straightforward coverage needs, but freelancers working across multiple industries, handling sensitive client data, or serving large institutional clients benefit from comparing quotes across carriers

That last point matters more than most freelancers expect. Soma, for example, provides access to hundreds of carriers — including Chubb, Markel, and Liberty Mutual — and lets freelancers receive quotes across multiple providers through a single application. This is especially relevant when a client's contract requires specific limits or when standard markets decline coverage outright.

How Much Does Professional Liability Insurance Cost for Freelancers?

Premium Benchmarks by Profession

According to Insureon customer data, independent contractors pay an average of $88/month for professional liability coverage. Costs vary meaningfully by profession:

| Profession | Average Monthly Premium |

|---|---|

| Marketing consultants | ~$55/month |

| Software developers | ~$83/month (median) |

| Building design professionals | ~$142/month (median) |

| Independent contractors (all types) | ~$88/month (average) |

Source: Insureon and TechInsurance customer data

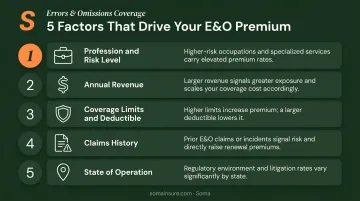

What Drives Your Premium

Five factors affect what you'll pay:

- Profession and risk level — IT, tech, and legal consulting carry higher premiums than content writing or general marketing

- Annual revenue — Higher revenue typically means higher exposure and higher premiums

- Coverage limits and deductible — A $1M/$2M limit with a $2,500 deductible is common; adjusting either affects cost

- Claims history — Prior E&O claims will increase your rate

- State of operation — Some states have higher baseline costs due to litigation environment

Claims-Made vs. Occurrence Policies

Most professional liability policies for freelancers are claims-made, meaning the policy must be active both when the work was done and when the claim is filed. For project-based freelancers, this matters more than most realize.

If you switch providers between engagements, a coverage gap could leave you exposed for work done under a prior policy. The fix: purchase tail coverage (also called an extended reporting period) when canceling — it extends the window for claims to be filed under the old policy.

Occurrence-based policies cover events that happen during the policy period regardless of when the claim is filed, but they're less common and generally more expensive for professional liability.

Tax Deductibility

Professional liability premiums are generally deductible as an ordinary and necessary business expense under IRS Publication 535. This covers insurance premiums tied to your trade or business, including professional negligence coverage.

Consult a tax professional to confirm how this applies to your situation.

Frequently Asked Questions

How much is liability insurance for a freelancer?

Independent contractors pay an average of $88/month (about $1,056/year) for professional liability, based on Insureon customer data. Costs vary by profession — marketing consultants average closer to $55/month, while software developers run around $83/month.

Do freelancers need liability insurance?

Yes — especially professional liability (E&O) if you provide advice, deliverables, or any professional service. Many corporate clients require proof of E&O coverage before signing a contract, and a single dispute can cost far more than the annual premium.

What insurance do I need as a freelancer?

Most freelancers need at least two to three policies depending on their work:

- Professional liability (E&O) — essential for any service-based freelancer

- General liability — recommended if you meet clients in person or work on-site

- Cyber liability — worth adding if you store or transmit sensitive client data

What does professional liability insurance not cover for freelancers?

E&O does not cover bodily injury, property damage, intentional wrongdoing, illegal acts, or employment disputes. Freelancers need general liability to cover physical risks and may need separate cyber or employment practices policies for other gaps.

Can I deduct professional liability insurance as a business expense?

Yes. IRS Publication 535 allows deductions for insurance premiums that are ordinary and necessary for your trade or business, which includes professional liability and malpractice coverage. A tax advisor can help you document and apply the deduction correctly for your situation.

Conclusion

Professional liability insurance isn't just about protecting against worst-case scenarios — it's increasingly a prerequisite for working with serious clients. Larger companies routinely require proof of E&O coverage before contract signing, and many enterprise clients won't move forward without it.

When evaluating providers, look beyond the monthly premium. Check AM Best ratings, verify your profession is explicitly covered, understand the claims-made structure, and consider whether a single carrier gives you everything you need.

If your work is specialized, your clients are institutional, or you want coverage that reflects what you actually do, get a professional liability quote through Soma. With access to hundreds of carriers — including Chubb, Markel, and Liberty Mutual — Soma matches freelancers to the right policy with one application, no broker chasing required.