Introduction

Running a small clinic means carrying liability risk that large hospital systems spread across entire legal departments and institutional policies. Independent practices don't have that safety net — when a patient files a malpractice claim, the financial and legal exposure lands directly on the clinic.

According to the AMA's 2025 Policy Research Perspective, medical professional liability premiums have risen for six consecutive years (2019–2024), with 49.8% of reported premiums increasing in 2024 alone. Sixteen states saw at least one increase of 10% or more.

For small clinics covering multiple providers — physicians, NPs, PAs, part-time specialists — the exposure compounds quickly. A single uncovered claim can threaten not just the practice's finances, but the personal assets of its owners.

This guide breaks down the best medical malpractice carriers for small clinics in 2026 — what separates a solid policy from an inadequate one, and how premiums vary by specialty and state.

TL;DR

- Medical malpractice insurance covers legal defense, settlements, and judgments when patients allege negligence — a must-have for any small clinic without hospital backing

- Claims-made policies cost less upfront but require tail coverage when a provider exits; occurrence policies cost more annually but eliminate that obligation

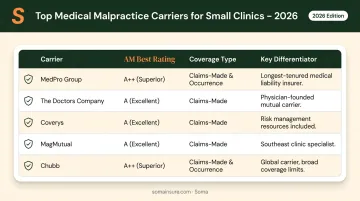

- Top carriers for small clinics in 2026: MedPro Group, The Doctors Company, Coverys, MagMutual, and Chubb — each with distinct strengths

- Filter carriers by AM Best rating (A- or higher), consent-to-settle terms, and tail coverage options before comparing price

- A multi-carrier broker lets small clinics compare custom quotes through one application, with no separate submissions required

Why Small Clinics Need Dedicated Medical Malpractice Coverage

Physicians employed by large health systems are typically covered under their employer's institutional policy. Independent clinic owners are not — they must source their own coverage, and that policy needs to protect both individual providers and the clinic entity itself.

This distinction matters because patients often sue the practice, not just the individual physician. Without facility-level coverage, a vicarious liability claim against the clinic as an employer can result in uninsured exposure for clinic owners personally.

The Financial Stakes

Washington State's 2025 medical malpractice report found an average indemnity payment of $956,032 per paid claim in 2024 — and claims over $1 million accounted for 77.4% of total paid indemnity over the prior five years. Even when no liability is found, defense costs run high: Washington's 2024 data showed an average of $89,691 per claim.

For a small clinic operating without adequate limits, a single claim can exceed a full year of revenue — before any judgment is entered.

2026-Specific Risk Factors

Several trends are pushing small clinics to reassess their coverage structures:

- Telemedicine expansion — Clinics offering remote services need to verify their policy covers services rendered across state lines; many standard policies are state-specific by default

- Mixed provider models — Practices employing NPs, PAs, or contracted specialists face vicarious liability exposure that not all individual physician policies address

- Premium hardening — With 46 states and Washington D.C. reporting at least one premium increase in 2024, small clinics shopping for first-time coverage or renewals are entering a tighter market

Best Medical Malpractice Insurance for Small Clinics in 2026

The carriers below were selected based on AM Best financial strength, suitability for small-to-mid-sized practice groups, policy structure flexibility, and claims defense quality — not simply market size.

MedPro Group (Berkshire Hathaway)

MedPro Group is the largest medical professional liability insurer in the U.S. by market share, backed by Berkshire Hathaway's financial strength. AM Best affirmed its A++ (Superior) rating in July 2025, with a stable outlook.

Member companies include The Medical Protective Company, Princeton Insurance Company, PLICO, and Wellfleet — giving MedPro broad specialty and geographic coverage for outpatient clinics.

What makes it a strong fit for small clinics:

- Offers occurrence, claims-made, and convertible claims-made forms to match coverage structure to your staffing model

- Pure consent-to-settle provision keeps settlement decisions with the clinic, not the insurer

- Free tail coverage at retirement under qualifying conditions reduces long-term financial exposure for founding physicians

| Feature | Detail |

|---|---|

| Coverage Type | Occurrence, claims-made, and convertible claims-made |

| Best Suited For | Small clinics in high-litigation states or high-risk specialties needing strong financial backing |

| Key Feature | Free tail coverage at retirement; A++ AM Best rating |

The Doctors Company

The Doctors Company is the largest physician-owned malpractice insurer in the U.S., covering over 100,000 members with an A (Excellent) AM Best rating — with AM Best revising its outlook to positive in October 2025. Its 2025 agreement to acquire ProAssurance expanded its specialty and geographic reach, creating a combined entity with approximately $12 billion in assets.

Strong fit for independent clinics: Physician ownership aligns governance and claims defense philosophy with the insured's interests. The company also invests heavily in risk management education and patient safety resources — tools that reduce claim frequency rather than simply responding after the fact.

| Feature | Detail |

|---|---|

| Coverage Type | Occurrence and claims-made policies |

| Best Suited For | Independent primary care and specialty clinics prioritizing claims defense quality and risk management support |

| Key Feature | Physician-owned mutual; expanded reach post-ProAssurance acquisition |

Coverys

Coverys is a specialized medical professional liability carrier covering physicians, surgeons, outpatient facilities, and allied health providers. It holds an A-rated financial strength designation through Medical Professional Mutual Insurance Company and its subsidiaries, and uses data-driven underwriting and analytics-based risk management.

A practical fit for clinics managing provider turnover: Coverys offers a modified claims-made policy that includes a prepaid tail with an indefinite extended-reporting endorsement at no additional premium.

For small practices, this eliminates the large lump-sum tail payment that typically comes due when a provider leaves or retires — one of the most overlooked financial risks in a growing clinic.

| Feature | Detail |

|---|---|

| Coverage Type | Modified claims-made with prepaid tail; traditional occurrence also available |

| Best Suited For | Small clinics with provider turnover concerns or those seeking to eliminate tail cost exposure |

| Key Feature | Prepaid unlimited tail included at no additional premium in modified claims-made form |

MagMutual

MagMutual is a physician-owned mutual insurer covering over 40,000 clinicians and healthcare organizations, with $3.2 billion in total assets and $1.214 billion in capital and surplus as of its 2024 annual report. AM Best rates it A (Excellent). While regionally strong in the Southeast, it has a growing national footprint.

Best for clinics wanting consolidated coverage: MagMutual's coordinated coverage model bundles medical professional liability with cyber, regulatory, and workers' compensation lines — reducing the complexity of managing multiple policies across different carriers. Its policyholder dividend and rewards program also returns value to clinics with strong claims histories.

| Feature | Detail |

|---|---|

| Coverage Type | Claims-made and occurrence options |

| Best Suited For | Small multi-provider clinics seeking bundled coverage (MPL + cyber + regulatory) in a single program |

| Key Feature | Bundled healthcare coverage programs; policyholder dividend and rewards program |

Chubb

Chubb is a globally rated insurer with AM Best affirming its A++ (Superior) financial strength rating for its grouped subsidiaries in January 2026. In the U.S., Chubb provides medical liability insurance for healthcare organizations and outpatient facilities, with financial capacity suited to complex or multi-location clinical environments.

Purpose-built for mixed-provider teams: Chubb's medical liability product covers civil liability from professional acts and errors, vicarious liability for contracted clinicians, and Good Samaritan acts. This is particularly relevant for small clinics employing NPs, PAs, or part-time specialists whose coverage status under standard physician policies is often ambiguous. Soma works with Chubb as a carrier partner for healthcare insurance placements, alongside specialty markets CRC Group and Kinsale.

| Feature | Detail |

|---|---|

| Coverage Type | Professional liability/malpractice on a claims-made basis with supplementary protections |

| Best Suited For | Small clinics with mixed provider types (MDs, NPs, PAs) or those needing vicarious liability coverage for contracted staff |

| Key Feature | Vicarious liability for contracted clinicians; Good Samaritan coverage included |

Key Coverage Features Small Clinics Should Look For

Claims-Made vs. Occurrence

Claims-made is the more common structure and carries lower initial premiums. The catch: it only covers incidents reported while the policy is active. When a provider leaves or the clinic switches carriers, claims-made coverage requires a tail policy — typically costing 150% to 200% of the final annual premium as a lump sum, according to Gallagher Healthcare.

Occurrence policies cover any incident that happened during the policy period, regardless of when the claim is filed. No tail obligation on exit — but annual premiums run higher. For small clinics with high provider turnover, the math on tail costs can tip the decision toward occurrence.

Facility vs. Individual Coverage

Some policies only cover the named physician. That leaves the clinic entity itself exposed when a patient sues the practice rather than the individual. Small clinics need to confirm their policy either includes separate facility coverage or addresses vicarious liability claims against the practice as an employer.

Consent-to-Settle Provisions

Consent-to-settle clauses determine who controls settlement decisions. A policy requiring insurer consent before settling can prevent the clinic from resolving claims on its own terms — and a settled claim, even without admission of liability, can affect the clinic's NPDB record. Look for policies that give the insured meaningful input or veto power.

Financial Strength Ratings

Require an AM Best rating of A- or better — this is a hard floor, not a preference. Defense costs alone can run into six figures even when no liability is found, and a carrier's reserves need to hold through prolonged litigation in high-severity cases.

Telemedicine and Multi-State Coverage

Standard policies are often state-specific. Clinics offering telehealth services or operating across multiple locations need to verify that their policy explicitly covers services rendered remotely and extends to all practice states. Ask your broker to confirm this in writing before binding — gaps here are common and costly to discover mid-claim.

Before committing to any policy, verify these five features are addressed:

- Policy structure: Claims-made or occurrence, and what tail coverage costs if you switch

- Entity coverage: Whether the clinic itself — not just individual providers — is named

- Settlement control: Whether the insured has consent or veto rights on settlements

- Carrier rating: AM Best A- or better, confirmed at binding

- Telehealth scope: Remote services and all active practice states explicitly covered

How Much Does Medical Malpractice Insurance Cost for Small Clinics?

Premium is driven by five variables: specialty, number of providers, state, policy type, and claims history. Geography creates some of the widest spread.

AMA's 2025 Medical Liability Monitor data shows the range clearly for $1M/$3M limits:

| Specialty | Location | Annual Premium |

|---|---|---|

| Internal medicine | Miami-Dade, FL | $59,736 |

| Internal medicine | Philadelphia, PA | $24,647 |

| Internal medicine | Connecticut | $21,770 |

| Internal medicine | New Jersey | $18,410 |

| OB-GYN | Miami-Dade, FL | $243,988 |

| OB-GYN | Nassau/Suffolk, NY | $171,672 |

| OB-GYN | Connecticut | $154,591 |

| OB-GYN | New Jersey | $94,640 |

A few practical notes:

- Group policies can sometimes yield lower per-provider costs than individual policies, depending on how a carrier prices the clinic's specialty mix — worth exploring, but verify through actual quotes rather than assuming savings

- New-provider discounts exist at several carriers, with The Doctors Company offering claims-free credits of up to 25% for eligible Florida members plus additional society discounts

- Clean claims history is one of the strongest levers for premium reduction; clinics with no prior claims should ask about loyalty or dividend programs when negotiating renewals

In high-premium states like Florida and New York, carrier pricing and willingness to write certain specialties varies widely. Getting quotes from multiple carriers side-by-side — through a single application with a multi-carrier broker — is the most practical way to benchmark what you should actually be paying.

Conclusion

No single carrier is the right fit for every small clinic. The decision depends on specialty mix, provider turnover frequency, state litigation environment, and long-term growth plans. A clinic adding telehealth has different coverage needs than one with a stable three-physician panel in a low-litigation state.

What doesn't change: financial strength, policy structure, and claims defense quality should drive the selection process — not price alone. A carrier rated below A- or a policy missing facility-level vicarious liability coverage creates exposure that a lower premium won't offset.

Applying those criteria across multiple carriers is where a broker with deep healthcare market access makes a practical difference. Soma works with hundreds of carrier partners — including Chubb, Markel, Liberty Mutual, and Nationwide — as well as specialty healthcare markets like CRC Group and Kinsale. Small clinics can submit one application and receive quotes from carriers that match their specialty, state, and structure. Get a no-obligation quote through Soma to find out what coverage aligned to your clinic's actual risk profile costs.

Frequently Asked Questions

Frequently Asked Questions

How much does a $1,000,000 medical malpractice liability policy cost?

It varies by specialty and state. Internal medicine can run $18,000–$60,000 annually at $1M/$3M limits, while high-risk specialties like OB-GYN range from $95,000 to over $240,000 in high-litigation states. Claims history and policy type (claims-made vs. occurrence) also affect final pricing.

What is the difference between claims-made and occurrence malpractice insurance for a small clinic?

Claims-made covers incidents reported while the policy is active — when the policy ends, you need tail coverage to protect prior acts. Occurrence covers any incident that happened during the policy period regardless of when the claim is filed, eliminating the tail obligation but carrying higher annual premiums.

Do small clinics need separate coverage for nurse practitioners and physician assistants?

It depends on the policy. Some group clinic policies extend vicarious liability coverage to employed NPs and PAs, while others require individual policies for each mid-level provider. Clinics should confirm with their carrier or broker whether mid-level providers are explicitly named or covered under the facility's policy — don't assume they are.

What is tail coverage and when does a small clinic need it?

Tail coverage (extended reporting endorsement) protects against claims filed after a claims-made policy ends for incidents that occurred during the active policy period. Small clinics need it when a provider leaves, retires, or the clinic switches carriers. The cost is typically 150%–200% of the final annual premium, paid as a lump sum.

Can a small clinic be sued for malpractice even if an individual physician is at fault?

Yes — patients can sue the clinic entity directly under vicarious liability theory. Small clinics need facility-level coverage in addition to individual physician policies; a claim against an uninsured practice entity can expose owners' personal assets.

How do I compare medical malpractice insurance carriers for my small clinic?

Start by filtering for AM Best financial ratings of A- or better, then compare policy structure — claims-made vs. occurrence, tail options, and consent-to-settle terms. Use a multi-carrier broker to receive competing quotes from specialty-focused insurers through a single process, rather than approaching each carrier separately.